15 September 2025

Key Insights: Fed at the Crossroads

Fed Cuts on the Table

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

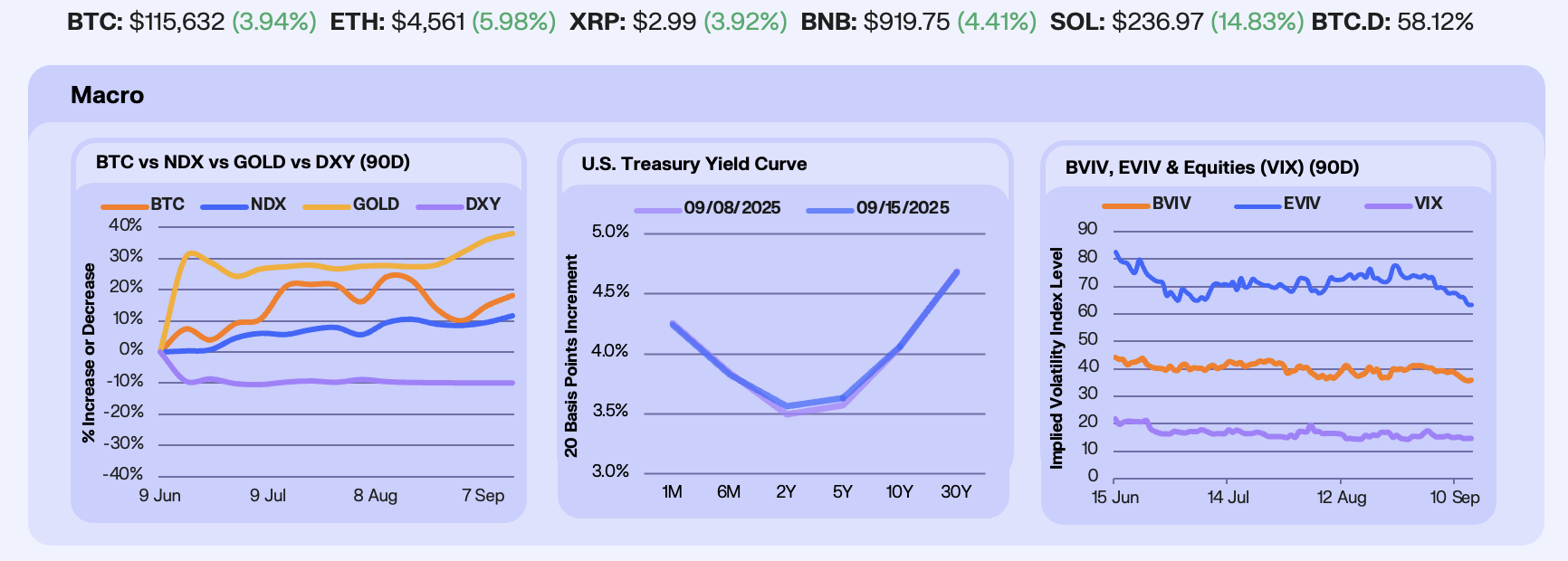

Last week, markets digested a historic -911k downward revision to U.S. payrolls through March 2025, the largest in history and concentrated in consumer-facing sectors. Inflation data was mixed, with PPI turning negative MoM for just the second time since March 2024 (and July revised lower), while CPI came in slightly hotter, driven by housing rather than tariffs. The combination fueled bets on easing policy, with a 25 bp cut this week all but cemented and 50 bps in play. Bitcoin (+2.8%) climbed, NDX (+1.9%) hit fresh all-time highs, and inflation-adjusted Gold (+1.5%) set a new record for the first time since the 1980s.

Markets are now pricing in 75bps of rate cuts by year-end. As a result, the 10Y Note Yield dipped below 4.00% for the first time since April 4th. The curve dynamics were more nuanced. The front end slipped (1M -2 bps, 6M -1 bps), the 2Y and 5Y firmed (+7 bps and +6 bps), while the long end stayed anchored (10Y +1 bp, 30Y -1 bp). Rather than a clean steepener, the move reflects markets leaning heavily into front-loaded cuts while questioning how much policy relief can extend further out the curve. The Treasury market is endorsing near-term easing but remains unconvinced about the durability of growth and inflation trends into 2026.

Implied vol continues to drift lower across the board as spot holds steady. Bitcoin IV fell from 38.6 to 35.7 (-7.4%), Ethereum IV eased from 67.5 to 63.2 (-6.4%), and the VIX slipped from 15.6 to 14.6 (-6.2%). Options positioning shows caution, with put demand rising ahead of this week’s Fed decision. Traders are bracing for Powell’s decision and the steady bleed in implieds highlights how macro risk is being hedged selectively.

Our Take: The record payroll revision marks a turning point where policy easing is no longer optional. With 75 bps of cuts now priced in 2025, the market is effectively daring the Fed to overdeliver, and Bitcoin is the clearest expression of that bet. While equities grind higher, Bitcoin’s consolidation near all-time highs signals it is positioning as the high-beta proxy for U.S. monetary easing. Retail is still stuck on “Red September,” but in this regime, every incremental dovish shift amplifies its upside.

Altcoins Join Rally

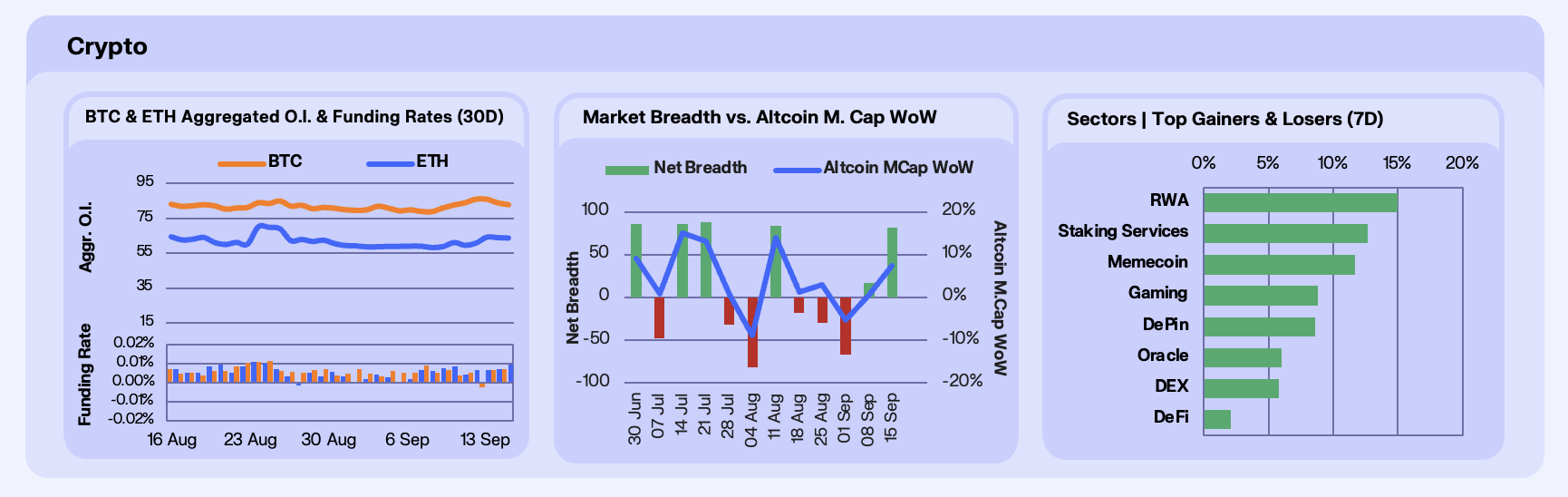

Majors posted a strong rebound this week, led by Solana’s outperformance. The orange coin posted most gains of around 4.9%, supported by $2.3b in weekly spot ETF inflows, including $315m into Fidelity’s FBTC, reversing August’s outflow trend and lifting September inflows to $2.57b. Digital Asset Treasury (DAT) adoption also remains a structural tailwind, with public firms having crossed the 1m BTC held threshold. ETH, up 8.5% WoW, outpaced BTC, driven by $405m in ETF inflows on September 12th, reversing a six-day outflow streak, bringing cumulative inflows above $11b. SOL stood out this week, up 17% WoW, propelled by Galaxy’s $700m purchase, believed to be tied to Galaxy’s backing of Forward Industries, poised to be the largest Solana treasury firm. We also saw a $40m DeFi Development Corp. buy, bringing total corporate holdings above 2m SOL. Momentum was further supported by the Alpenglow upgrade. Looking ahead, anticipation of Solana spot ETF approvals and capital inflows into Solana DATs, with Kyle Samani slated to head one up in the near-future, add speculative fuel to the rally.

Derivatives positioning reflects this ETH sentiment shift relative to BTC. BTC OI edged up 2.2% WoW to $82.8b, while ETH surged 8.6% to $63.6b. Funding rates remained contained, reflecting stronger long bias tied to ETF and DAT demand. Positioning suggests BTC leverage remains measured, while ETH leverage is accelerating, with traders more willing to extend risk into ETH.

Interestingly, altcoins bounced even harder than ETH, showing one of the first clear-cut scenarios of capital being pushed down the risk continuum in a general risk-on environment we’ve seen in weeks. Altcoin market cap climbed 6.2% WoW to $1.72t. Breadth was positive at net 76, with 88 advancers vs. 12 decliners, marking the first broad rebound in weeks, further highlighting this broad-based risk on sentiment. Pump.fun’s token was a standout, rallying 65.8% on aggressive buybacks, of which there have been over $90m to date, as well as supply contraction, and revenue momentum of $20m weekly, underscoring how token-specific catalysts are driving outsized returns.

Sectors showed broad strength, led by RWAs, up 15%, Staking, up 12.7%, and Memecoins, up 11.7%. Memecoins were particularly strong, with DOGE and BONK up 20.8% and 14.9% WoW respectively.Sector performance highlights rotation into narrative-driven assets, with RWAs and staking capturing structural capital while memecoins continue to benefit from speculative momentum.

Our Take: ETH’s surge in OI points towards traders moving into a risk on environment with elevated demand for leverage. This is further supported by Solana’s treasury buys, and the broad altcoin breadth, signalling capital is moving down the risk continuum, a rare sign of sustained risk-on sentiment. This rebound appears far more durable than recent bounces.

Stablecoin Leverage Builds

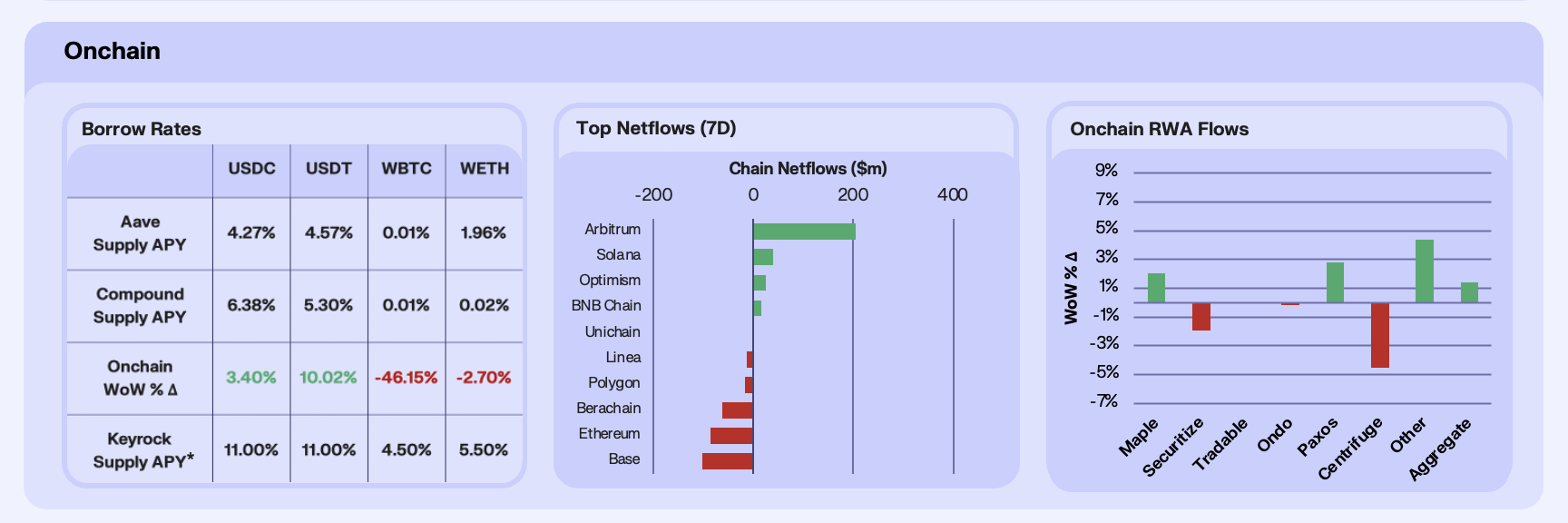

Onchain supply rates were mixed this week, with stablecoin yields climbing, signalling leverage demand onchain. USDC yields climbed 7.4% WoW, while USDT was flat. WBTC yields remained negligible and WETH fell 7.9% amid a 54.8% jump in Aave supply. The dynamic underscores how even with steady inflows, borrow demand continues to soften, particularly in ETH markets.

Chain netflows pointed to a clear rotation from Ethereum and Base toward Arbitrum. Arbitrum posted $205m in inflows, amid extreme demand for yield on the L2. Base saw outflows of $104m despite strong fundamentals, as liquidity shifted to Arbitrum. Ethereum recorded $87m in outflows, coinciding with a 2.6m ETH validator exit queue and heavy bridge activity.

RWAs were once again a bright spot, with aggregate AUM up 0.69% WoW as sector market cap expanded to $17b. Maple led with a 6.0% gain, driven by syrupUSDC deposits crossing $100m on Solana. Ondo rose 4.1% to $1.5b TVL, supported by tokenised equity momentum, while Paxos and Centrifuge saw inflows from gold tokenisation and Solana launches respectively.

Our Take: Yields reflect the trend of a risk-on sentiment, with leverage appetite increasing both on and offchain. RWAs continue to prove resilient, positioning tokenisation as DeFi’s most consistent growth engine heading into Q4.

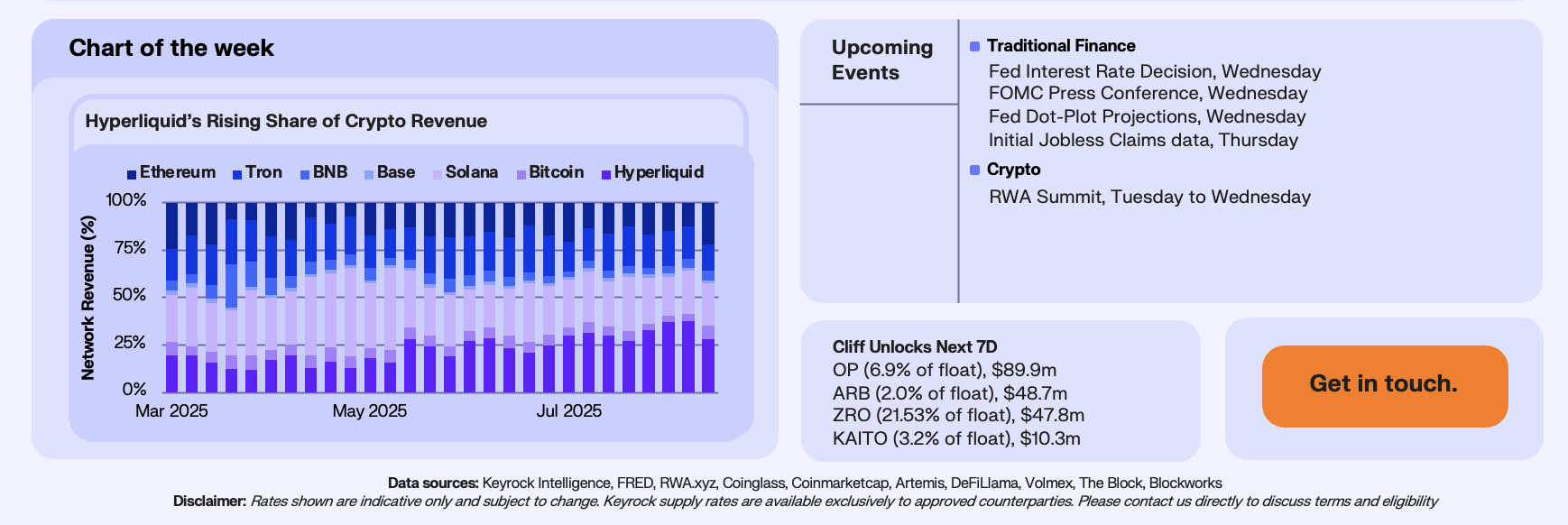

Hyperliquid’s Rising Share

Hyperliquid’s share of total network revenues among chains has climbed sharply in recent months, rising to over 35% by late August before settling at 28% last week. That puts it alongside Solana, Tron, and Ethereum as the top revenue-generating networks, underscoring how quickly Hyperliquid has captured flow in a market historically dominated by entrenched L1s and how steadily it is carving out a bigger slice of the pie.

This growth highlights a paradox. Despite commanding a rising share of trading revenue, Hyperliquid still relies heavily on external stablecoins for settlement. More than $5.5b in USDC sits on the platform today, and at current rates, over $200m of annual stablecoin revenue flows to Circle. To address this, the protocol opened up the USDH ticker to prospective issuers, drawing proposals from players like Paxos, Frax, Agora, Sky, Ethena, and OpenEden, each offering different mixes of compliance, value capture, and liquidity design.

Among the proposals, Native Markets emerged as the frontrunner with a Hyperliquid-first design. Under the Native Markets proposal, USDH will be natively issued, backed by cash and U.S. Treasuries through Bridge, with custody split between BlackRock offchain and Superstate onchain. Yield distribution follows a 50/50 split with half directed to the Assistance Fund via HYPE buybacks, and the other half reinvested into ecosystem growth through HIP-3 markets, builder code interfaces, and HyperEVM apps. On compliance, Bridge already holds MSB/MTL licenses and provides a flexible regulatory pathway. With founder Max Fiege advising both leading HyperEVM apps and HYPE DatCo, Native’s team is positioned to keep USDH aligned with Hyperliquid’s long-term growth.

Our Take: The real story isn’t the outcome of the USDH vote as leading issuers have already committed to building on Hyperliquid regardless of a failed proposal. Runner ups are likely to pursue alternative stablecoin tickers and compete to establish the most aligned stablecoin on HL. This dynamic has accelerated partnerships across stablecoins, payments, and DeFi, reinforcing HL’s push into the three largest markets in crypto: exchanges, smart contract platforms, and stablecoins. Despite rivaling Ethereum, Tron, and Solana in revenue share, HYPE still trades at a steep discount. We see that gap closing as USDH redirects reserve yield to buybacks and revenues compound across its current product offering, putting Hyperliquid on track toward a $100B FDV over the next year.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.