20 April 2026

Key Insights: False Dawn

Strait Reversal

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

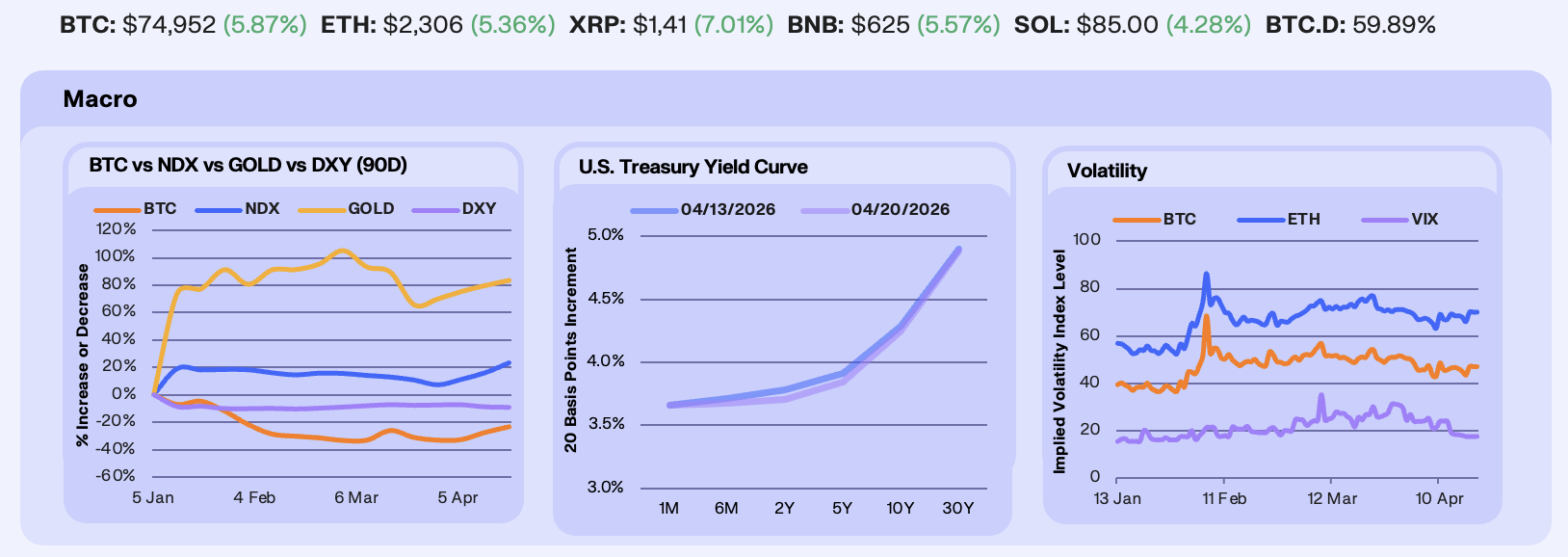

The Strait of Hormuz dominated the markets for a second consecutive week last week. Iran’s foreign minister declared the Strait “completely open” on Thursday, crashing Brent 11% in a single session to $87 and lifting equities to their strongest weekly performance of the year. The euphoria lasted less than 24 hours, until Tehran reversed course on Friday, reinstating control of the Strait after the U.S. refused to lift its naval blockade of Iranian ports, sending Brent back toward $96. NDX rose 6.34% to $26,672, extending a daily winning streak to 13 sessions by Friday, the longest since 1992. BTC rose 5.54% to $75,480 on strong spot ETF inflows, while Gold gained 2.06%, and DXY dipped marginally at -0.32% for the week.

Treasury yields declined across the curve for the second straight week as the Strait reopening, even temporary, softened near-term inflation pricing. The 2Y fell 7 bps to 3.71%, dropping below the FFR upper bound of 3.75% for the first time since the war began, a meaningful shift from the hike pricing that has dominated since March. The 5Y declined 6 bps to 3.85% and the 10Y eased 4 bps to 4.25%, while the 30Y barely moved at -1 bp, still anchored near 5%. The pattern mirrors last week, where we’re seeing front-end and belly declining while the long end holds, but the 2Y crossing below the FFR upper bound is new. Initial claims fell to 207k against an expected 215k, extending the streak of resilient labor data, while industrial production contracted -0.5% in March after a +0.7% expansion in February. The next FOMC is April 28-29th, with CME pricing an 86% probability of a hold.

We saw equity and crypto volatility diverge sharply on the Strait reversal, but only towards the end of the week. Through Thursday, all three benchmarks were declining in lockstep as the reopening compressed risk premia, with the VIX bottoming at 17.47, its lowest close since before the war. Friday’s closure jolted crypto vol immediately, with BTC IV spiking 3.52 points to ETH IV jumping from 66.03 to 70.04, while the VIX held flat at 17.47. We believe that the weekly print, VIX -8.58% and BTC IV +1.38%, masks the intraweek reversal and overstates the de-risking. We will be watching price action closely approaching the April 24th Deribit expiry, which holds roughly $8B in notional across 90.7k BTC, with max pain at $72,000 and the most actively traded contract the $70,000 put.

Our Take: The 2Y dropping below the FFR upper bound is the most significant rate positioning shift since the war began, although it was short lived. Crypto vol already knows this, with BTC IV snapping back on Friday, while equity vol is pricing a resolution that does not yet exist. If the ceasefire on Wednesday lapses without extension, the tentative easing narrative could unwind, where we’d expect to see the 2Y retrace above the FFR upper bound, and the hike debate resume heading into the April 28th FOMC.

Squeeze Preview

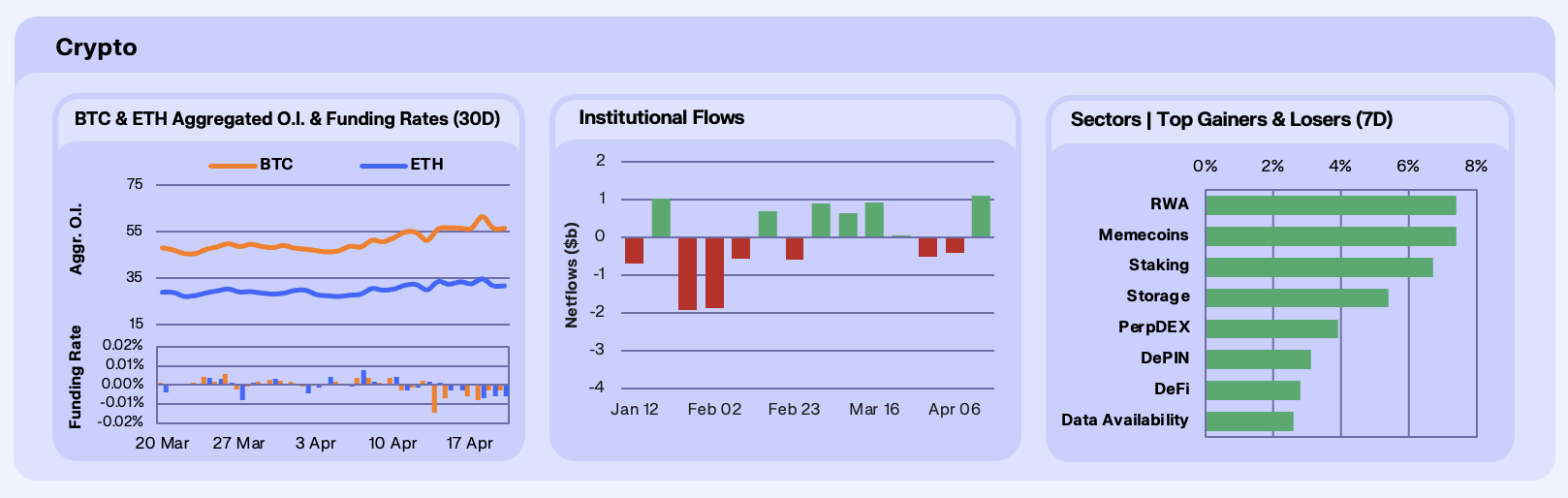

Open interest was flat on the week but the close disguises a violent intra-week swing. BTC OI edged +0.44%, while ETH fell -5.6%. The weekly numbers miss the April 18th event when Iran announced the Strait of Hormuz would reopen under a new ceasefire framework, upon which BTC OI spiked to $61.7B, a $5B increase in a single session, as leveraged longs piled in and shorts were forcibly covered, triggering $820M in liquidations, primarily on the short side. BTC touched $78,348 before Iran’s parliament rejected Trump’s nuclear deal claims within hours, collapsing the bid and unwinding the entire OI build by Saturday. Funding rates remained negative throughout. BTC has now posted negative funding for 46 consecutive days, the longest sustained negative streak since the FTX collapse in November 2022. The persistence of crowded short positioning against a price that has ground from the mid-$60ks to $77k+ creates significant short-squeeze potential, and Friday’s event previewed what that unwind looks like when a catalyst lands, even a false one.

Institutional flows accelerated for a second consecutive week, with Bitcoin ETFs recording +$996.5M in weekly inflows, with Ethereum adding +$276M, Solana +$35M, and Ripple +$55M, for a combined +$1.36B. This is ****nearly double last week’s +$700M and the strongest weekly total since January. BlackRock’s IBIT captured $871M of the BTC total, while Morgan Stanley’s MSBT, the first spot BTC ETF from a major US bank, launched April 8th at a category-low 0.14% fee, crossed $100M in its opening week. BTC ETF AUM now sits at $91B and ETH at $14B. The flow acceleration coincides with exchange reserves falling to 2.21M BTC, a seven-year low representing just 5.9% of circulating supply, and Strategy adding 13,927 BTC on the week, valued at north of $1B, as a result of its healthy STRC product. YTD crypto ETF flows have now turned positive at $2.3B after Q1’s persistent outflows.

Sector performance was uniformly positive, a shift from recent weeks of clear winners and losers. RWA and Memecoins co-led at +7.4%, with RWA continuing to benefit from structural institutional flows, with tokenised RWA AUM hitting $27.6B, BlackRock’s BUIDL crossing $1B in market cap, and Franklin Templeton partnering with Ondo to issue tokenised versions of five ETFs for 24/7 blockchain-native trading. Memecoins caught a specific catalyst in Canary Capital’s PEPE ETF filing, with PEPE surging +10% on April 17th alone. Staking gained +6.7%, led by Lido after approval of a second $20M LDO buyback programme. On the downside of a green board, DeFi’s +2.8% underperformed the field, weighed by the Kelp DAO exploit on April 19th, a $292M bridge hack via LayerZero that marked the largest DeFi exploit of 2026 and forced Aave, SparkLend, and Fluid to freeze rsETH markets.

Our Take: The April 18th Hormuz reversal is the most informative event of the week purely for what it previewed in the market. A single geopolitical headline generated $5B in OI, $820M in liquidations, and a $78K print within hours. The structural setup behind that move has not changed, and our desk notes that the last two instances of this funding regime, March 2020 and November 2022, resolved with violent upside moves within weeks. The April 22nd ceasefire expiry remains the proximate trigger, whereby if it extends, short-squeeze pressure should continue to build with institutional capital reinforcing the floor. If it lapses, the test is whether the $1.36B in fresh ETF positioning holds or joins the leverage unwind.

Beyond Derivatives

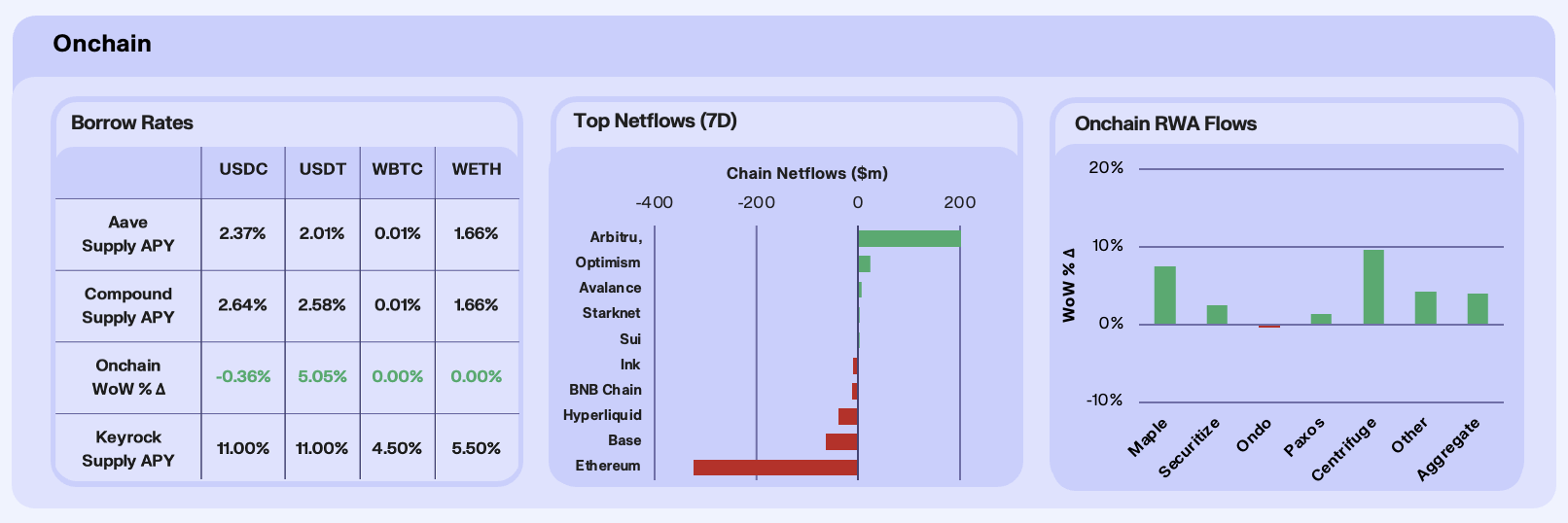

Stablecoin lending rates stabilised this week after several weeks of oscillation. USDC supply APY was essentially flat at -0.36% WoW across major venues, with utilisation holding steady near 0.80. USDT rose 5.05% WoW, with utilisation also expanding, reinforcing the pattern of borrowing demand concentrating in Tether-denominated markets rather than broadening across assets. The stabilisation in rates, rather than continued compression, is notable and aligns with our view from recent weeks that onchain lending markets are finding a floor defined by selective demand rather than broad-based borrowing.

Chain-level flows broke from the pattern that has defined recent weeks, with Arbitrum posting a dominant +$444.9M in net inflows, displacing Hyperliquid, which had led inflows for four consecutive weeks, as the primary destination for capital. The catalyst was Arbitrum’s high-visibility presence at ETHCC[9] in Cannes, where targeted activations around scaling and RWA infrastructure converged with the formal approval of ArbitrumDAO Procedures on April 2nd and continued momentum from its STEP tokenization program with Franklin Templeton, Spiko, and WisdomTree.

RWA AUM rose +3.97% WoW in aggregate, with Centrifuge leading at +9.62%, continuing to benefit from adoption of deSPXA on Base. deSPXA is the tokenised S&P 500 Index Fund licensed by S&P Dow Jones Indices and sub-advised by Janus Henderson, which is increasingly being integrated as collateral across Base DeFi protocols. Maple posted +7.47%, driven by steady institutional demand for its overcollateralised syrupUSDC and syrupUSDT lending vaults.

Our Take: Arbitrum’s ability to absorb nearly $450m in a single week suggests the market for onchain capital is widening beyond the derivatives-versus-payments binary we identified in recent weeks. A third lane of institutional infrastructure is emerging as the market shows flickers of recovery. Our desk is watching for whether Arbitrum can sustain these flows once the event-driven narrative fades, or whether capital rotates back to the structural winners.

DeFi's Deadliest Month

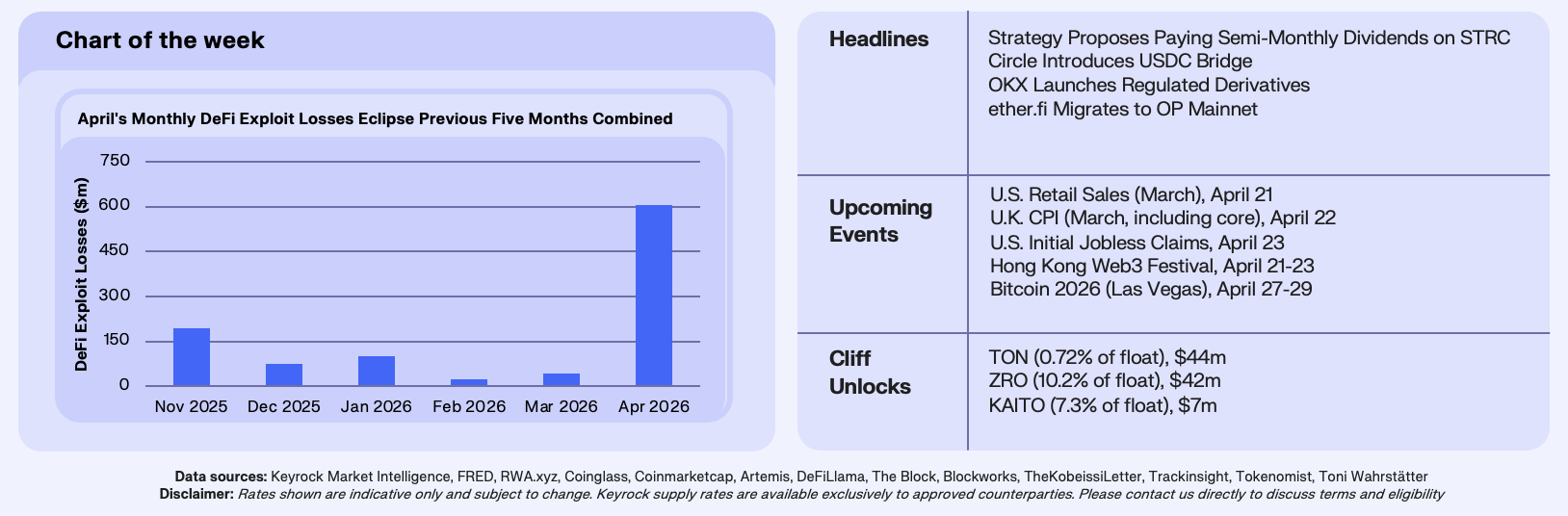

This week’s chart tracks monthly DeFi exploit losses over the past six months, whereby the trajectory through Q1 told a reassuring story. After a $194M November, losses declined steadily through December ($76M), stabilised in January ($100M), and fell to a cycle low of $24M in February, with March only marginally higher at $41M. The combined Q1 total of $165M was comfortably below Q4 2025’s run rate. Then April happened, and with ten days still remaining in the month, losses have already reached $606M, more than the entire previous five months combined, and the worst single month for DeFi exploits since October 2022.

This month’s damage is concentrated in two mega-exploits, both attributed to North Korean state-linked actors. On April 1st, Drift Protocol on Solana was drained of $296M after DPRK-linked operatives spent six months infiltrating the team, social-engineering two of five Security Council multisig signers into pre-signing hidden authorisations via Solana’s durable nonces feature, then seizing admin control and executing 31 rapid withdrawals in 12 minutes. Then, more recently, on April 18th, KelpDAO’s rsETH bridge was exploited for $293M, roughly 18% of the rsETH circulating supply, through a configuration flaw in its LayerZero integration. This flaw was a 1-of-1 DVN setup that allowed attackers to forge a single verifier attestation and authorise fund release. Neither exploit was a smart contract bug, instead both were failures of operational security and infrastructure configuration.

The KelpDAO contagion was immediate and severe, with the attacker depositing stolen rsETH as collateral across Aave V3 and V4, borrowing over $236M in WETH and wstETH. Aave’s TVL fell $6.3B in 24 hours, from $26.4B to roughly $20B, and WETH pools hit 100% utilisation, with bad debt estimated at $177-200M. rsETH depegged approximately 42%, while wrapped rsETH stranded across 20+ Layer 2 chains as backing reserves was drained. AAVE fell 16%, while SparkLend, Fluid, and Upshift all froze rsETH markets within hours.

Our Take: We think the composition of, and type of, the exploits in April matters more than the size. Both exploits were operational, meaning smart contract audits, which the industry has spent years and billions improving, would have caught neither. The structural risk exposed here is the supply chain of trust that feeds into the protocol governance. Aave’s contracts worked exactly as designed, it was the collateral that failed. As LRT and restaked assets proliferate as DeFi lending primitives, the attack surface is no longer the protocol itself but the security assumptions of every external asset it accepts.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.