25 August 2025

Key Insights: Dovish Winds

The Fed’s Pivot

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

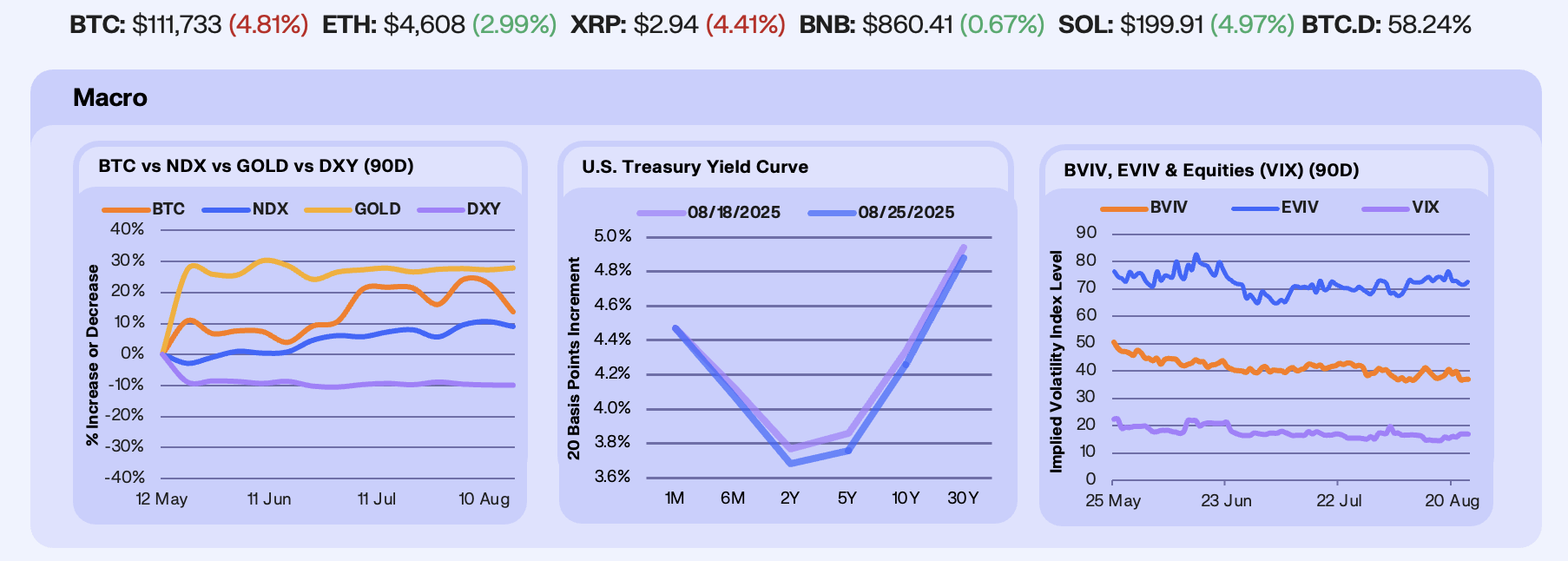

Markets turned after Powell’s Jackson Hole remarks on Friday struck a dovish tone, acknowledging labor market weakness and hinting at a September rate cut. That shift eased fears that inflation would dominate the Fed’s reaction function. BTC (-4.8%), the Nasdaq (-0.9%), and USD (-0.2%) softened over the week, while Gold (+0.5%) held firmer as traders recalibrated expectations toward an earlier policy pivot.

Prediction markets now price a 25 bps September cut at ~80%, while 50 bps remains a long shot at 4%. The Treasury curve bull-flattened as the 2Y–5Y yields fell 9 and 10 bps while the 30Y eased just 6 bps to 4.88%. The move reflects markets leaning into Fed easing expectations, but with the long end less responsive as investors balance rate-cut bets against inflation outlooks.

These crosscurrents fed into options markets where implied volatility stayed muted despite the macro uncertainty. Bitcoin’s IV slipped from 38.5 to 36.8 (-4.4%), while Ethereum’s eased from 73.3 to 71.5 (-2.4%). The VIX sprung higher from last week to 16.81 (+6.9%), yet is still pinned near multi-year lows. The subdued backdrop highlights complacent positioning as markets await upcoming macro catalysts that could quickly jolt sentiment.

Our Take: The Fed’s dovish shift and signs of labor market softness strengthen the case for a September cut, giving risk assets a more supportive backdrop. The bull flattening of the yield curve underscores growing conviction in near-term easing. In crypto, subdued vols reflect confidence rather than complacency, while ETH’s stronger call interest signals traders positioning for medium-term upside. With macro headwinds easing, the balance is tilting toward a more constructive risk environment.

ETH Conviction Builds

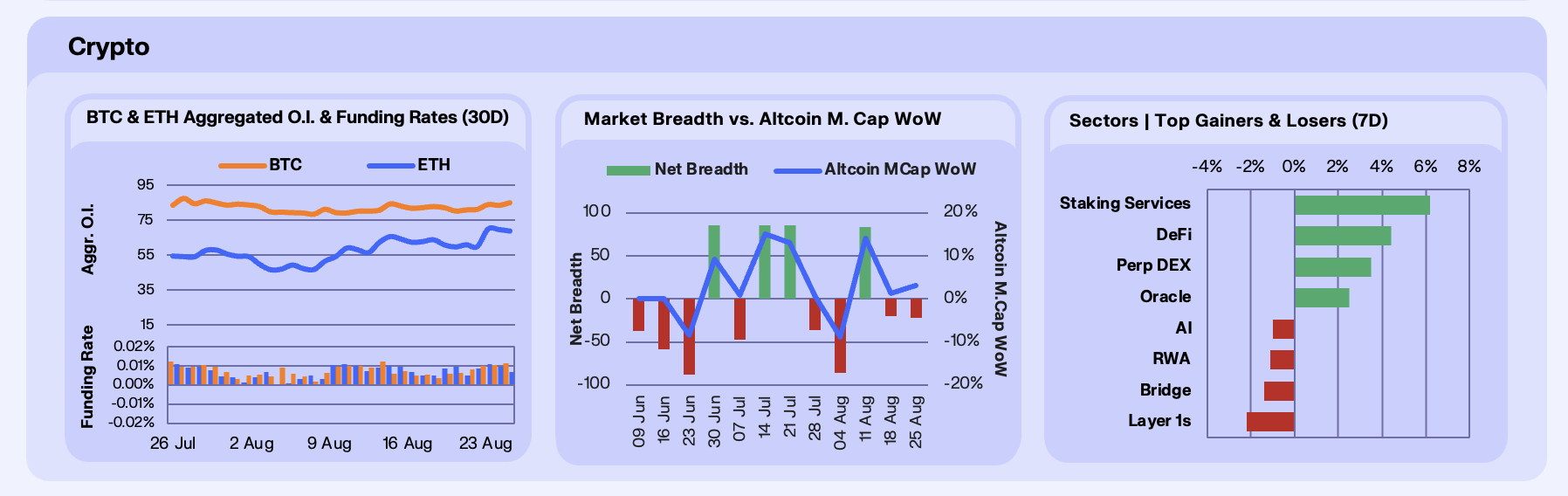

Following the market’s rally last week, altcoins rose +3% last week. Altcoin breadth stayed negative with just 39 advancers against 61 decliners (-22 net breadth). Despite headline gains, breadth volatility continues to show that “altcoin season” has yet to materialize, with ETH still the relative leader while most of the market struggles to sustain momentum.

By sector, performance was led by staking services (+6.2%), DeFi (+4.4%), and Perp DEXs (+3.5%), underscoring where investor conviction was strongest. Staking names benefited from renewed flows into yield-bearing strategies, while DeFi was lifted by strength in AAVE and MORPHO as lending activity picked up. Perp DEXs also gained as higher funding rates drove more onchain trading activity. The leadership across these segments highlights where capital is concentrating, even as broader altcoin participation remains narrow.

Bitcoin and Ethereum derivatives positioning strengthened this week, with open interest climbing despite choppy spot markets. BTC OI rose from $82.8b to $83.4b (+0.8%), while ETH surged +9.2% to ~$70b, marking a new all-time high. The buildup in ETH positioning highlights growing speculative interest from institutions while elevated funding rates signal trader willingness to pay up for leverage. While this highlights growing conviction in upside, it also leaves the market more vulnerable to liquidations should momentum falter.

Our Take: Given the poor market breadth, altcoin season remains elusive for now, but the backdrop is turning more supportive. ETH’s new all-time high in open interest and concentrated upside positioning show that speculative conviction is building. With the Fed signaling a dovish shift, liquidity conditions are improving and traders are increasingly positioned for a broader risk-on move. That suggests breadth could expand quickly once a clear macro or crypto-native catalyst emerges

Stables Diverge

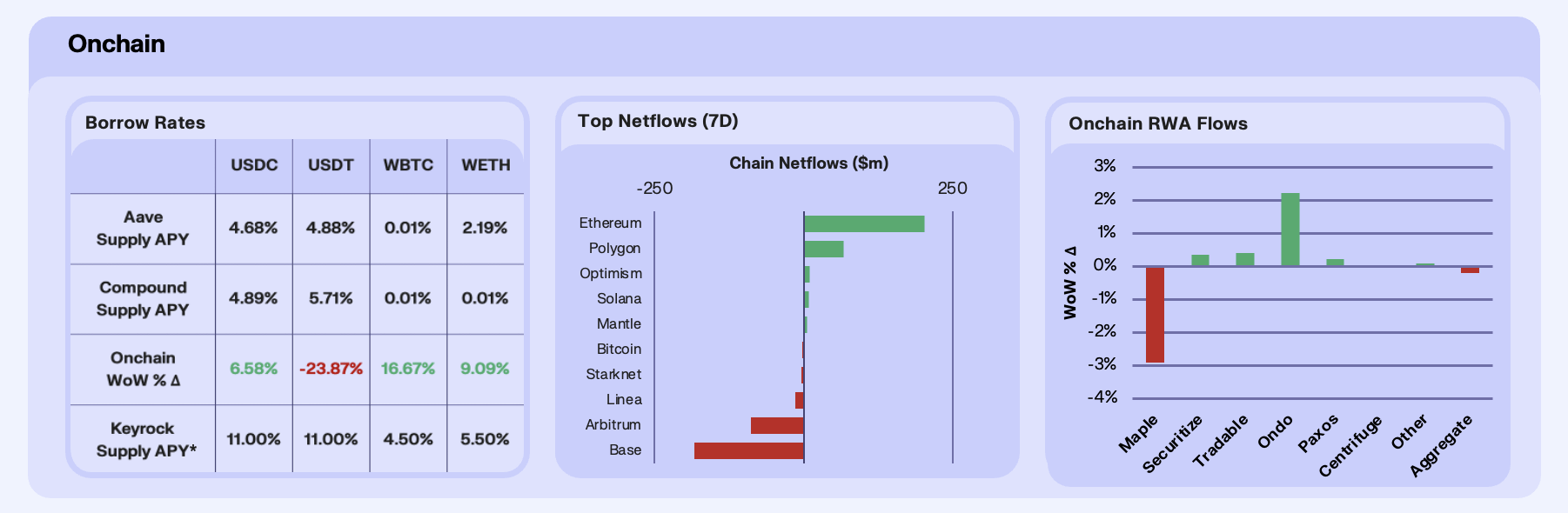

Onchain stablecoin rates diverged this week as supply shifts reshaped utilisation. USDC supply rates climbed 6.6% WoW as Aave capacity fell 4.2%. The extraction of capital likely being the primary driver, although leverage demand also could have driven the rate hike with market speculation rising amid market conditions. By contrast, USDT rates slipped 23.9% as pool deposits nearly tripled, diluting utilisation rates after weeks of capacity volatility. Despite this, USDT remains the stablecoin of choice onchain if seeking yield, with a 20 bps premium over USDC. WETH supply expanded 65% as lenders reentered pools amid longer-term conviction, pushing rates modestly higher to 2.19%.

Ethereum dominated inflows, pulling in over $200m on strong price action this week. Polygon followed with $100m inflows as stablecoin payments neared $1b for the month. On the other side, Base, down ~$200m, bled liquidity following on from its August 5th outage and congestion, while Arbitrum, down ~$100m, saw outflows tied to treasury transfers and retail rotation.

RWAs dipped 0.20% WoW, holding sector AUM near $26.3b. Ondo led with a gain of 2.24% on explosive tokenised treasuries adoption, backed by Coinbase and BlackRock, while Tradable, up 0.41% and Securitize, up 0.35%, saw steady governance-driven inflows. Maple fell 2.91% as late-week redemptions offset early growth in syrupUSDC pools, with Powell’s Jackson Hole comments weighing on yield-sensitive lenders.

Our Take: Liquidity is consolidating into majors. Ethereum for networks, USDC for stablecoins, and Ondo for RWAs. This concentration is bullish in the near term, with ETF flows, onchain credit, and stablecoin adoption all reinforcing each other, but it risks fragility if one leg stumbles. We see stables and RWAs as primed for continued inflows should September see further rate cuts.

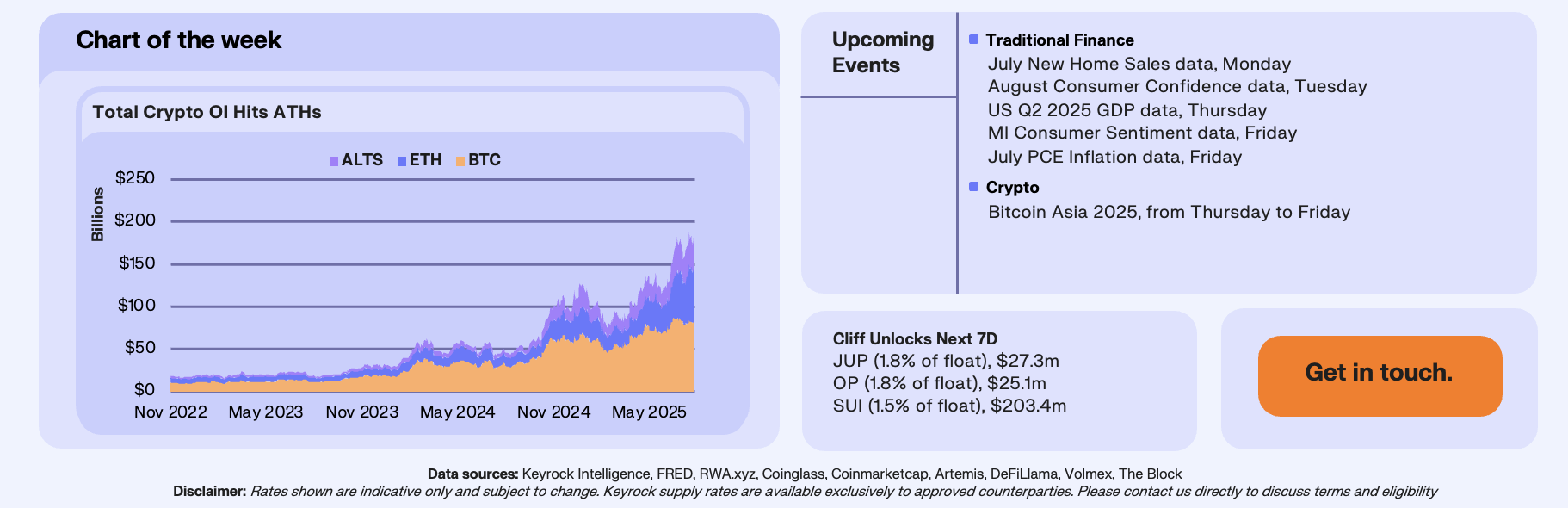

Record Levels of OI

With prices soaring this week, we’re seeing market participation kick back into gear, with total crypto OI retaking ATHs at over $218b. This growth has been rapid since mid-March, and has coincided with BTC’s push above $120k, and ETH’s push up towards $5k. OI is concentrated primarily on Binance, at x% dominance, though Bybit and Bitget have carved out a significant share at over x% each. Interestingly, though this rise in participation has coincided with BTC’s growth, ETH and altcoins now represent over 55% of total OI, with ETH alone at 34%, showing a clear rotation away from BTC dominance.

So, why’s this happening now? Price action and market FOMO is the clear driver. But if we scratch a bit deeper, we’re looking primarily at ETH ETF inflows, macro tailwinds such as rate cut bets and the liquidity backdrop, and the promise of altseason around the corner as the main catalysts. We still think there’s room for OI to run up however, with rising funding rates, averaging around 7-11%, signalling optimism but not yet at levels that indicate extreme overheating. That said, as OI rises it introduces the risk of higher volatility, with much of this week’s price action being driven by short liquidations in majors.

Our Take: Current )I levels are a double-edged sword. They clearly signal strong conviction, but leverage risks point towards sharp pullbacks if we see weaker than expected Fed cuts, or other temporary market disruptions. Near-term we expect chop and continued liquidations, though medium- to long-term we see the continued diversification of asset OI, with ETH’s perps dominance and ETF inflows setting it up for a $6k breakout, dragging alts higher and potentially pushing total OI toward the $300b mark by EOY.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.