22 September 2025

Key Insights: Cuts Without Conviction

Caution Over Conviction

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

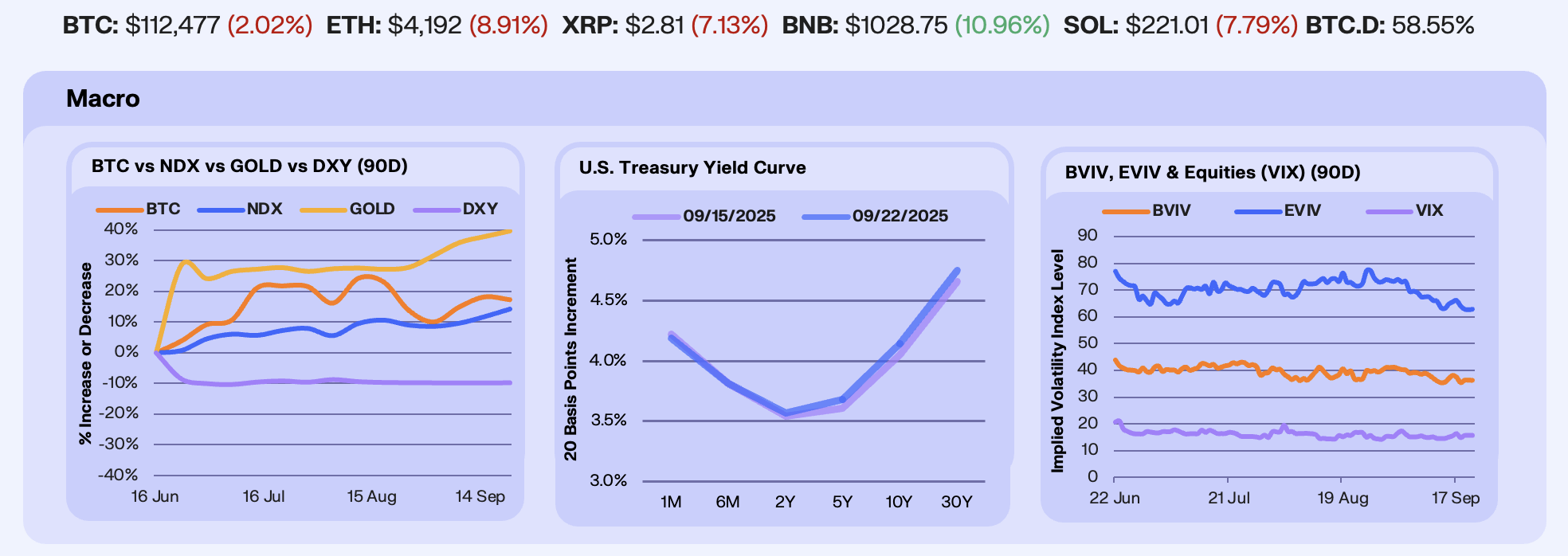

Last week, the U.S. Fed delivered its first rate cut of 2025, lowering by 25 bps in response to a weaker labor market, moderating growth, and rising downside risks to employment. Median projection now show 50 bps in additional rate cuts for 2025. BTC dropped -0.8%, Gold (+1.3%) and the NDX climbed (+2.2%) to fresh all-time highs, while the DXY (+0.1%) largely shrugged off the decision.

The curve reaction this week was subtle. The 10Y now sits at 4.14%, up from 4.05% last week, while the 2Y, 5Y, and 30Y all rose 3-9 bps. The rise in long yields reflects lingering inflation concerns, ballooning government deficit, and the heavy supply of Treasuries weighing on demand. Until those pressures ease, rates are unlikely to fall in a meaningful way. For the long end to rally, markets would need softer inflation prints, weaker growth, tighter mortgage bond spreads, or a Treasury shift toward shorter-dated issuance to relieve duration pressure.

Implied vols were mixed this week as spot markets held post-Fed. Bitcoin IV eased from 37.0 to 36.4 (-1.6%), while Ethereum IV slipped from 64.9 to 62.9 (-3%). In contrast, the VIX ticked higher from 15.1 to 15.8 (+4.1%), hinting at a mild repricing of equity risk even as crypto vols remain muted. The steady grind lower in BVIV and EVIV suggests positioning remains light as sentiment in options markets remains tilted bearish. The next catalyst will be upcoming GDP and labour data, which could accelerate further demand for hedges if macro risks reprice.

Our Take: The macro backdrop today carries echoes of 2019, when softening growth clashed with stubborn inflation signals and a labor market that was starting to wobble. That mix raises the risk of a stagflation, where weak growth collides with elevated prices, squeezing consumers and dragging on the broader economy. In such conditions, leaning too heavily on risk assets can leave portfolios vulnerable. Broadening into safe haven assets classes like treasuries, gold, and Bitcoin provides a more balanced stance, offering potential resilience if this cycle extends into a low-growth, high-inflation regime.

Altcoin Rally Reverses

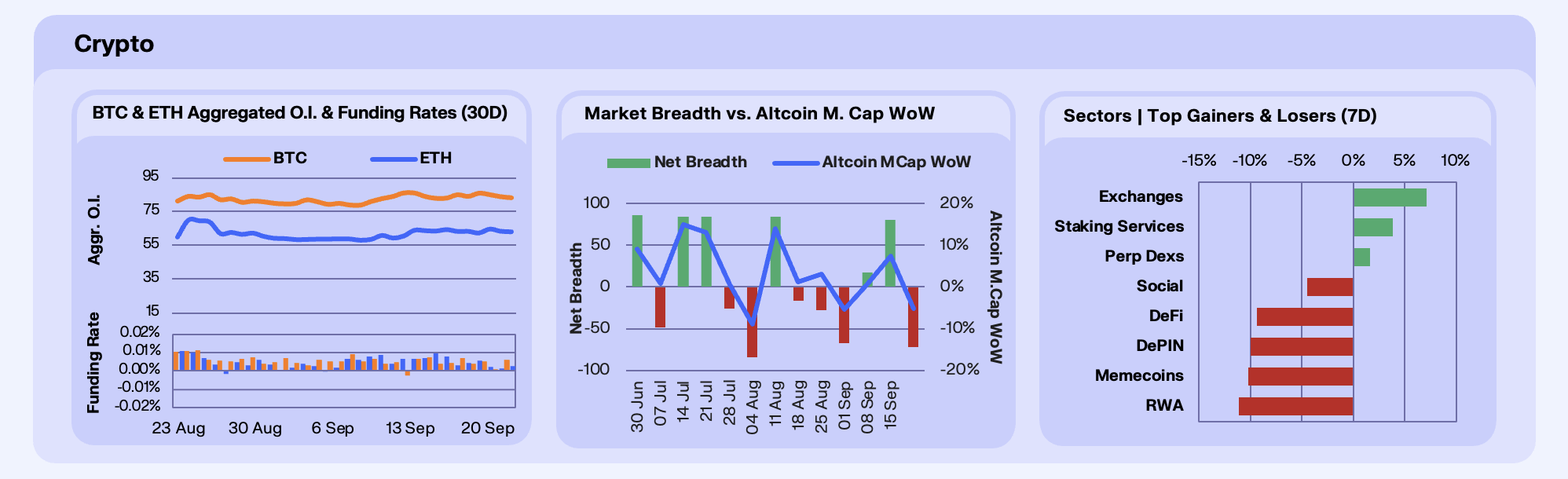

For crypto, the data points to elevated open interest and steady funding. BTC OI rose to $83.1b from $82.8b at the start of the week (+0.4%), while ETH OI edged lower to $63.1b from $63.6b (-0.7%). Funding rates have been consistently positive, indicating a persistent willingness to pay for long exposure despite a rangebound spot price in both BTC and ETH and a bearish skew in options markets. This buildup leaves positioning sensitive to a macro surprise, where a sharp move in spot could quickly trigger liquidations or, conversely, fuel a breakout.

Outside of BTC and ETH, altcoins snapped their two-week winning streak, falling -5.17%. Breadth flipped negative at -72 (14 advancers, 86 decliners), a sharp reversal from last week’s broad rally (+80 breadth, +7.4% cap). The pullback highlights fading risk appetite, with participation narrowing and sector-specific catalysts struggling to offset broader weakness.

Within that backdrop, sector performance was largely uniform. Gains were led by Exchange tokens (+7.1%), Staking Services (+3.8%), and Perp Dexs (+1.6%), with ASTER and AVNT standing out after their recent airdrops revived the airdrop meta and spurred users to resume farming points in perp DEX protocols. Outside of a handful of winners, most sectors bled this week, with Social (-4.5%), DeFi (-9.4%), DePIN (-10.0%), Memecoins (-10.2%), and RWAs (-11.1%) all posting steep losses. The breadth of weakness across speculative segments points to fading risk appetite, as capital retreats from higher-beta trades and narrows toward defensive or narrative-driven pockets.

Our Take: Historically, periods of strong altcoin breadth and performance are often followed by a moderation phase, suggesting that participation could taper off in the weeks ahead unless a clear macro catalyst revives risk appetite. With the altcoin index now in altcoin season territory, we expect short-term momentum to cool, with gains likely to become even more selective and concentrated in sectors and protocols with clear catalysts.

Stable Looping and RWA Growth

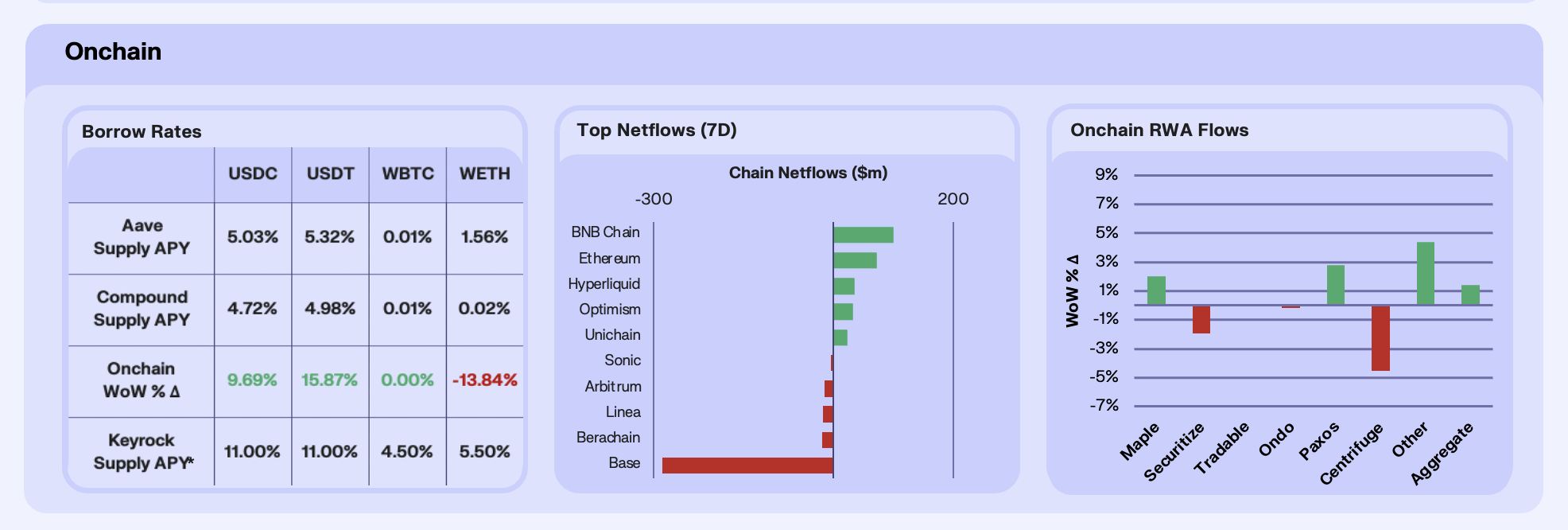

Onchain rates were mixed this week, with stablecoin yields climbing while ETH rates weakened. USDC APY rose 9.7% WoW and USDT gained 15.9% WoW. The moves came as supply contracted significantly, with USDC on Aave losing 25% of its capacity. WETH yields slipped 13.8% WoW as Aave supply jumped nearly 14%, pointing to ETH accumulation by users chasing yield, and softer borrow appetite. The divergence reinforces how traders are selectively extending risk into stablecoin lending while shying away from ETH leverage.

Chain netflows showed sharp divergence across ecosystems, with Base seeing $271m outflows, continuing its struggle with user retention, thin liquidity, and reputational setbacks. Ethereum also recorded $87m outflows, tied to a 2.6m ETH exit queue. Meanwhile, BNB Chain posted $91m inflows, riding record activity, token burns, and post-CZ sentiment as it broke to new all-time highs.

RWAs extended gains, with aggregate AUM up 2.3% WoW. Ondo led with an 8.5% gain, pushing TVL to ~$1.66b as tokenised Treasuries trading drew strong demand post-Fed cuts. Maple rose 2.4%, surpassing $4b AUM on the back of syrupUSDC scaling across Solana and Arbitrum. Paxos gained 2.5%, with PAXG inflows tied to gold’s strength and stablecoin integrations. Ondo and Maple continue to anchor growth, positioning RWAs as one of the most structurally consistent themes in DeFi.

Our Take: Stablecoin yields and Arbitrum inflows highlight a sustained risk-on tilt, with traders selectively seeking looping yield via stables and chasing ecosystem narratives. RWAs remain the standout growth engine, and if Ondo and Maple sustain current momentum, tokenisation could become the primary driver of DeFi AUM growth heading into Q4.

Chainlink Dominates Again

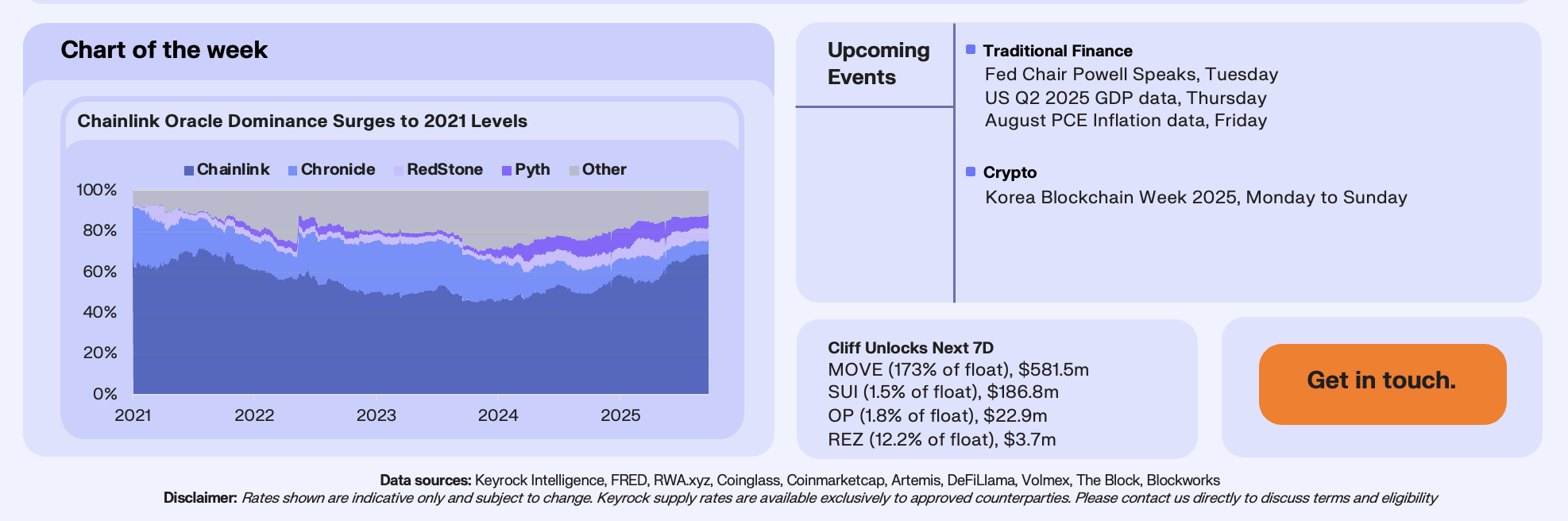

Chainlink has surged to an oracle market dominance level not seen since April 2021 this week, with market share of oracle total value secured hitting 69.4%. The market share growth, which has been in a general upward trend since November 2023, coincides with Polymarket’s decision on September 12th to adopt Chainlink for resolving price-based bets. This is a major validation for the oracle, given Polymarket’s rise as what’s been dubbed ‘the wisdom of the crowds in financial form’, in an industry that bridges crypto-native infrastructure with non-native capital, that is regularly achieving $1b in trading volume per month. Beyond Polymarket, Chainlink’s multi-chain footprint, spanning Ethereum, Arbitrum, Base, and Solana, has reinforced its status as the default oracle layer across DeFi.

This resurgence matters because oracles are the invisible backbone of onchain finance. Over the past two years, Chainlink’s market share had eroded as rivals like Pyth and Redstone gained traction with faster, cheaper price feeds. The return to near 70% dominance highlights how institutional-facing, reliability-first demand is reasserting itself, particularly from platforms where trust in final settlement is critical.

Our Take: Chainlink’s momentum is likely to sustain. With Polymarket setting a precedent, other prediction and derivatives platforms could follow suit, especially those scaling into regulated environments. If this adoption wave sustains, Chainlink could push back above 70% dominance in late 2025, cementing itself once again as the oracle layer of choice for high-value DeFi and prediction markets.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.