16 March 2026

Key Insights: Crude Drives The Tape

Bitcoin Breaks Rank

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

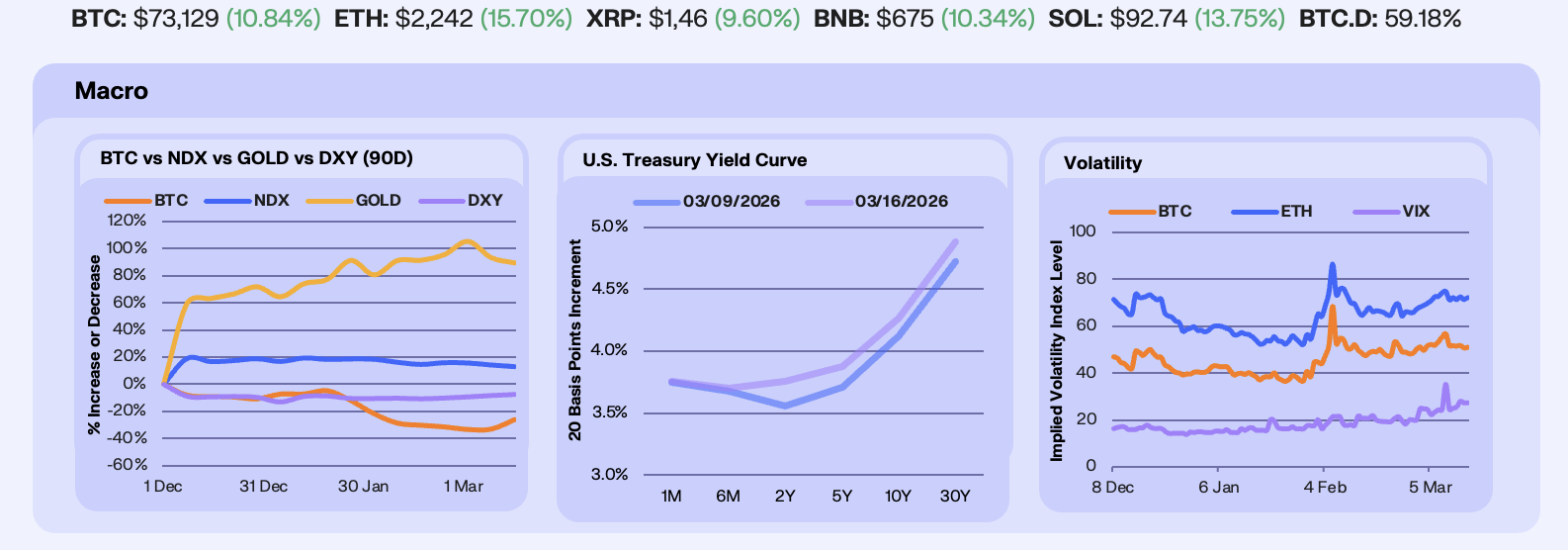

The second week of the Iran war produced a sharp divergence across asset classes. Iran vowed to keep the Strait of Hormuz closed, and the IEA labeled it the largest supply disruption in history, prompting 32 economies to release 400 million barrels from reserves. Brent continues to hold above $100. BTC surged +10.4% to $72,800, its strongest weekly gain since January, driven by roughly $763m in spot ETF inflows in the week as institutional allocators treated the volatility as an accumulation window. Gold edged lower at -2.0%, NDX slipped -1.1%, and the DXY firmed +0.9%, breaking above 100 for the first time since late November.

Treasury yields surged from the 2Y outward as the oil shock fed directly into forward inflation expectations, with the belly and long end adding +15 to +20 bps while the front end barely shifted. Friday’s data compounded the repricing with the Q4 GDP second estimate revised to 0.7% from 1.4% and January core PCE accelerating to 3.1% y/y. Slowing growth alongside re-accelerating inflation puts the Fed in a stagflationary bind heading into next week’s March 17-18 meeting, where futures price a 96% probability of a hold. Only one cut remains priced for 2026, likely December, with summer easing now off the table.

Volatility compressed sharply despite the BTC rally. BTC 30-day ATM implied volatility fell -10.2% WoW to 51.1, ETH IV declined -3.9% to 72.2, and the VIX dropped -22.6% to 27.2 after peaking near 35 earlier in the month. The decline in crypto IV alongside a nearly +10% spot move suggests the rally was spot-driven, with ETF inflows rather than derivatives doing the work. Options flow reflected a clear BTC-ETH split, with the largest BTC trades all bullish, concentrated in $75K-$80K call spreads and short put spreads, while top ETH flow were bearish, dominated by call sellers and put buyers. The VIX remains above pre-war levels, but the fade signals the market has largely absorbed the initial geopolitical shock.

Our Take: The defining feature of this week is the context of the BTC rally. Bitcoin gained +10% while yields surged, the dollar strengthened, and equities drifted lower against the largest supply disruption in history and a stagflationary data print. BTC’s 30-day correlation with the Nasdaq dropped from 92% to 69%. The March 18 FOMC commentary is now what the market is looking to next as a hawkish fed commentary that pressures equities without dragging BTC lower would confirm a meaningful regime shift for BTC.

Institutional Bid Returns

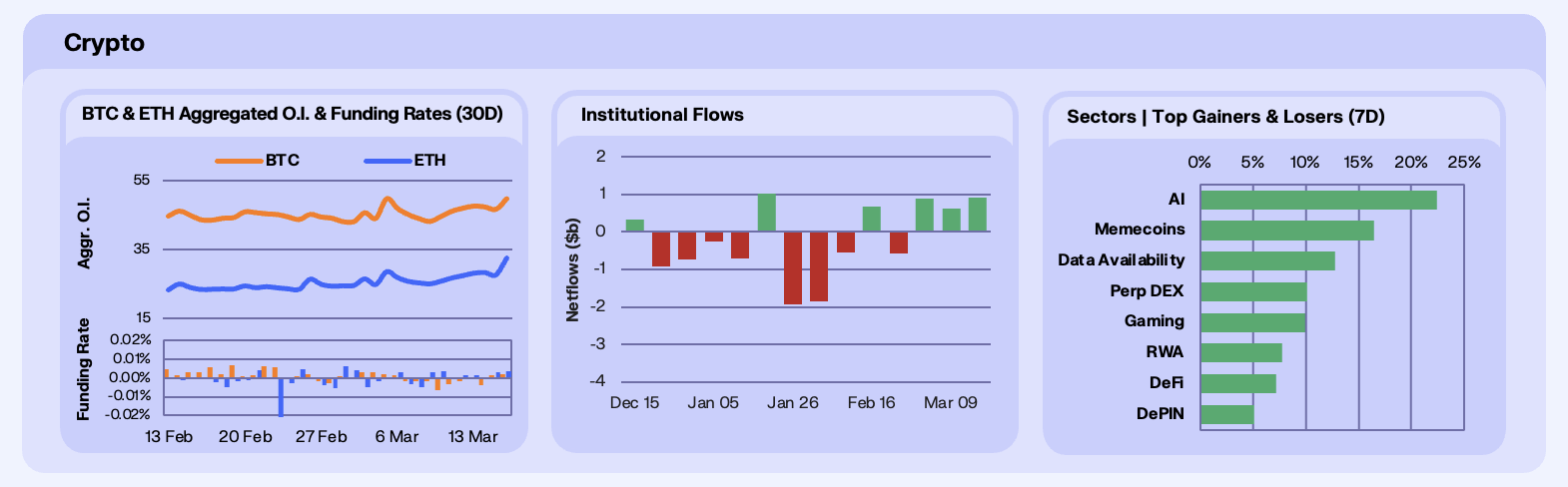

Crypto markets staged a strong recovery this week, with Bitcoin rising 9.9%, Ethereum 14.2%, and Solana 12.6%. Crypto largely shrugged off the risk-off macro backdrop, with BTC recovering from an early-week low near $62,400 to trade above $71,000 by Friday. ETH similarly reclaimed the $2,000 level, while SOL benefitted from ecosystem optimism following the approval of the Alpenglow upgrade, which is expected to reduce Solana transaction finality from approximately 12.8 seconds to 100-150 milliseconds once implemented.

Derivatives markets reflected the renewed bullish momentum, where our desks saw Bitcoin open interest rise 15.3% WoW to $49.7b, while Ethereum open interest surged 29.8% to $32.5b, indicating fresh positioning entering the rally. Funding rates flipped back into positive territory by the end of the week after briefly turning negative earlier, suggesting that short positioning was squeezed as prices moved higher. The sharp increase in ETH open interest alongside the price move points to renewed speculative demand, while BTC’s steadier positioning suggests the rally was supported by both derivatives flows and spot demand.

Institutional flows were also notably constructive on the week, with digital asset investment products recording $910.8m in weekly inflows, led by Bitcoin with $767.3m, followed by Ethereum at $160.8m. Solana products also saw $10.7m in inflows, continuing a steady trend of institutional interest in the ecosystem. The only notable outflow came from Ripple products, down -$28.1m. The sustained inflows into BTC and ETH ETFs mark the third consecutive week of positive institutional demand, reinforcing the view that large allocators continue to accumulate despite macro uncertainty.

At the sector level, performance reflected a clear risk-on rotation within crypto. AI tokens led the market (+22.4%), followed by memecoins (+16.5%) and data availability (+12.8%). Infrastructure segments also performed strongly, with perp DEX (+10.1%), gaming (+9.9%), and RWA (+7.8%) sectors all posting solid gains. The broad-based rally outperformers in more speculative fields suggests capital is rotating back into higher beta segments of the market after several weeks of defensive positioning.

Our Take: The week’s price action suggests crypto continues to demonstrate relative resilience to macro shocks, with institutional inflows and derivatives positioning helping drive the recovery. Our desk states the key level to watch for Bitcoin remains the $73k resistance zone, which marks the upper boundary of the current range. A sustained break above this level would likely signal a broader continuation of the market recovery, while failure to hold above $70k support could see volatility return in the short term.

Specialised DeFi Liquidity

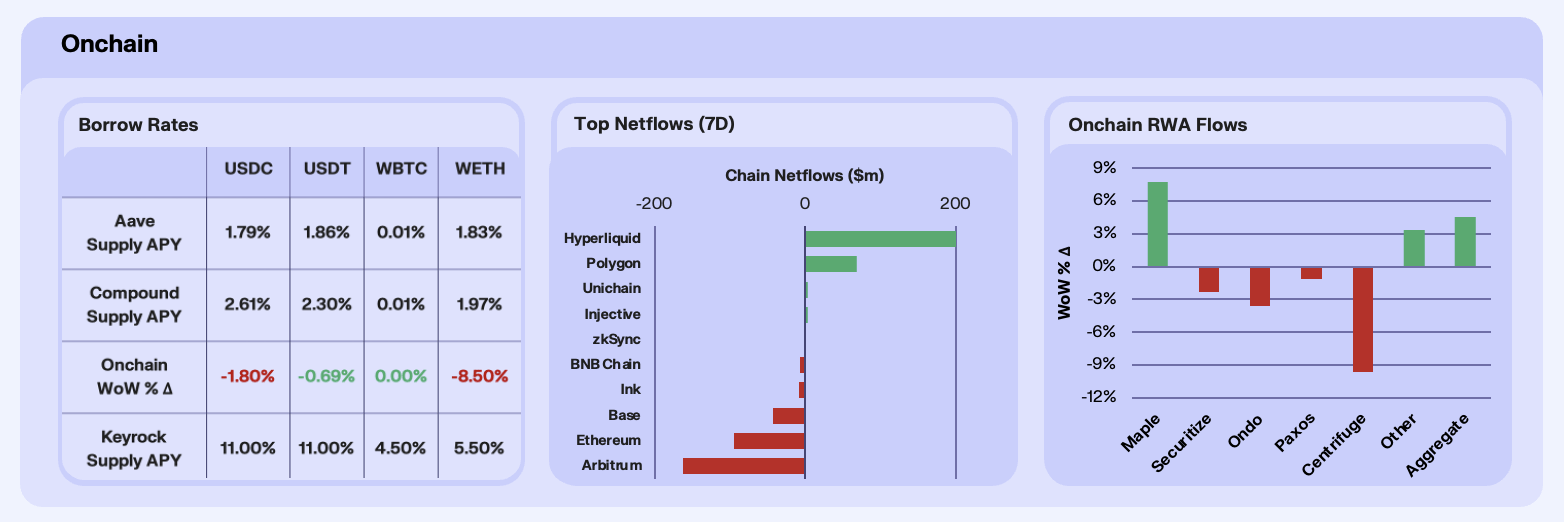

Onchain supply rates fell marginally across the board this week. Stablecoin yields moved slightly lower, with USDC supply APY declining 1.8% WoW while USDT fell 0.7%, leaving lending rates across major venues clustered between 1.8% and 2.6%. ETH-denominated yields weakened more meaningfully, with WETH supply APY down 8.5% WoW, suggesting that demand for leveraged ETH exposure remains muted, at least via looping, despite the broader price rally seen across crypto markets this week. Utilisation across lending markets remains relatively low, indicating that capital is still positioned defensively, though we are increasingly of the view that alternative venues for expressing market views, such as Hyperliquid, impact the extent to which looping strategies are utilised.

Chain-level netflows told a more directional story, with capital concentrating in ecosystems that benefited from specific catalysts during the week. Hyperliquid led inflows with +$248.7m, driven primarily by a surge in activity around tokenised commodity perpetuals. Polygon also recorded solid inflows of +$69.3m, building on momentum from recent network upgrades and strong stablecoin activity. Continued expansion of stablecoin payments and DeFi activity on the network has positioned Polygon as a relatively efficient settlement layer during periods of market volatility, particularly for lower-cost transactions and payment-focused use cases.

Within RWAs, the sector remained broadly resilient despite mixed performance across individual protocols. Aggregate RWA AUM rose 1.56% WoW, supported primarily by strong growth in onchain credit markets. Maple led the sector with a 7.8% increase in AUM, reflecting growing demand for tokenised lending products and increased composability of Maple’s syrupUSDC across DeFi protocols, where it is increasingly used as collateral and yield-bearing liquidity.

Our take: The onchain economy is becoming increasingly specialised. Rather than broad, synchronous capital flows across DeFi, liquidity is now rotating toward specific venues where clear catalysts exist, whether that is commodity volatility driving derivatives activity, stablecoin payment networks expanding usage, or tokenised credit markets attracting institutional demand. As the ecosystem matures, this type of selective capital allocation is likely to become a defining feature of the next phase of onchain market structure.

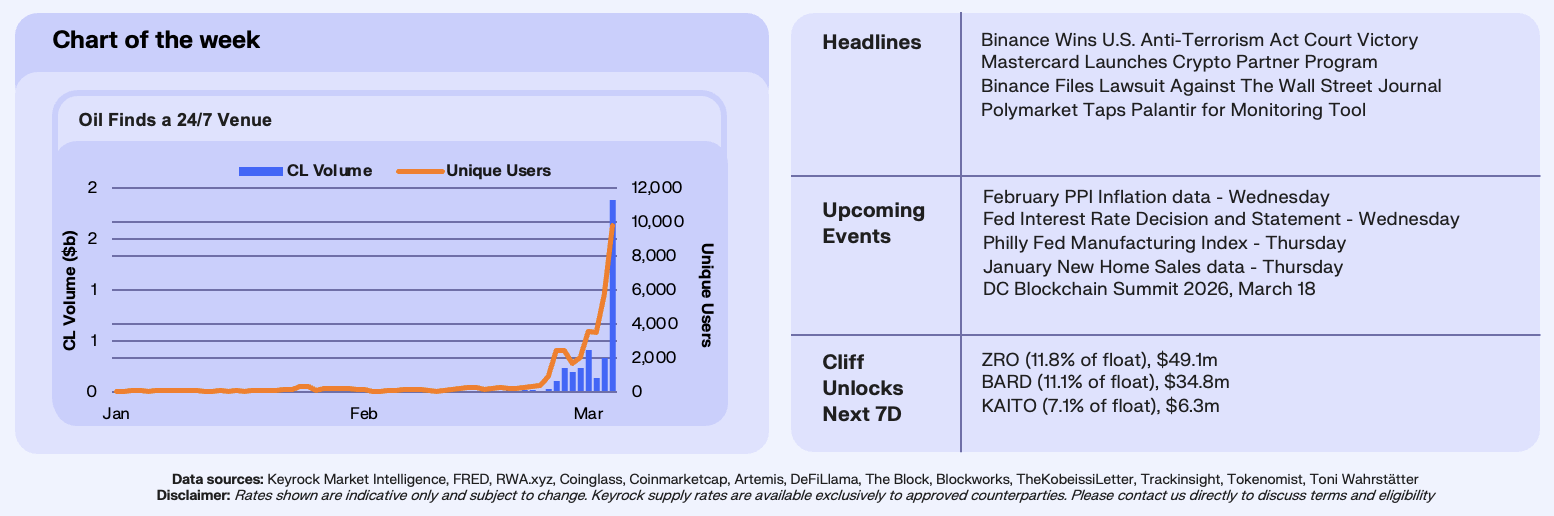

Crude Goes Onchain

Hyperliquid’s non-crypto perpetual markets (HIP-3) have become one of the fastest-growing venues in trading. Through HIP-3, traders access leveraged exposure to commodities, indices, equities, and FX on a 24/7 basis. The Strait of Hormuz closure has stress-tested Hyperliquid’s infrastructure. With traditional exchanges closed for the weekend, the oil supply disruption needed to be priced somewhere.

WTI crude volume (CL) on Hyperliquid surged from roughly $7M per day in late February to $413M on March 6 and $1.88B on March 9. That single day exceeded CL’s entire January volume of $75M by 25x. Nearly 10,000 unique addresses traded the contract, generating $140M in liquidations. Combined oil products hit $2.5B, overtaking silver ($504M) as the dominant HIP-3 asset for the first time. For the month, CL has already reached over $5B versus $216M for all of February.

HIP-3 overall has climbed from 19.7% of Hyperliquid volume in February to 30% in March, peaking at 40.1% on March 9. Cumulative volume is approaching $100B since launching in October. CL’s unique address count scaled from roughly 400 in late February to nearly 10,000 on March 9, suggesting genuine trader demand for 24/7 commodity access during a geopolitical crisis.

Our Take: This is what the beginning of 24/7 market pricing looks like, built on crypto infrastructure. When the oil supply disruption in the Strait of Hormuz hit, traditional commodity exchanges were dark yet nearly 10,000 traders priced it on Hyperliquid instead. As CFTC engagement around legal frameworks for continuous perps progresses, the gap between what onchain venues can offer and what traditional exchanges provide will only narrow. The signal to watch is whether CL and HIP-3 volumes sustain once these crises fade, which would confirm weekend onchain trading as a structural migration.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.