19 January 2026

Key Insights: Counting the Cuts

Rates Drive BTC’s Edge

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

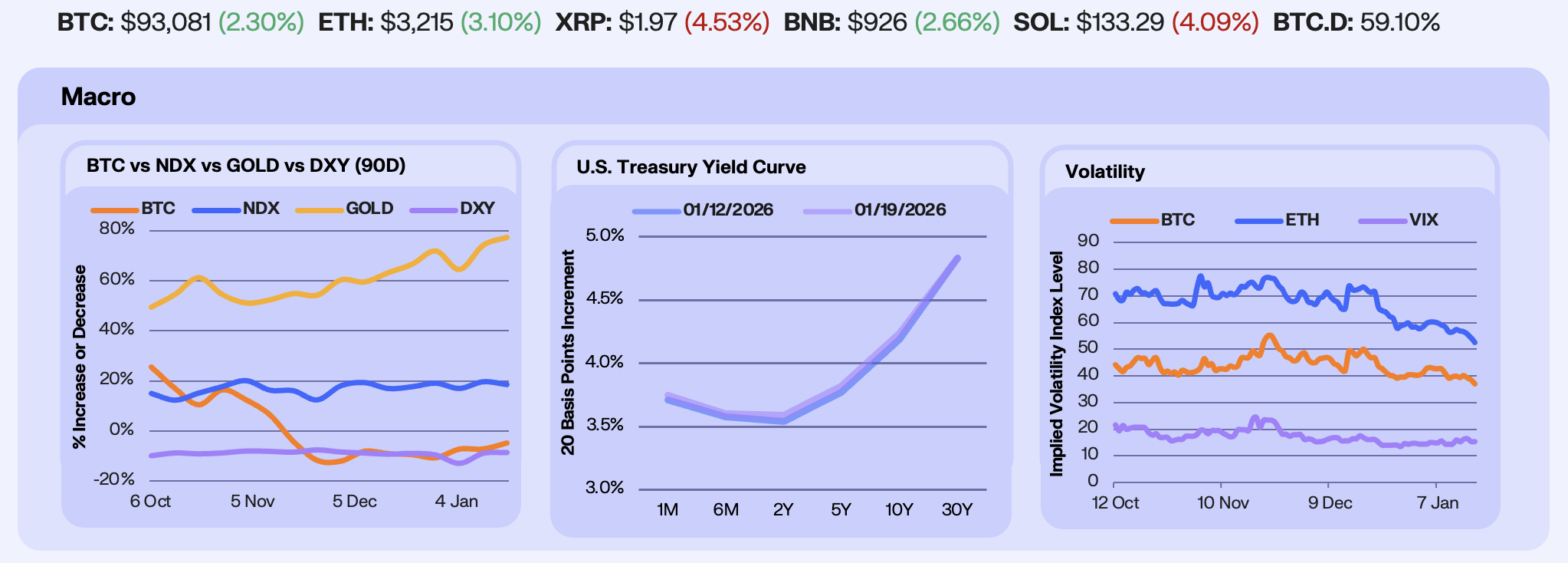

Last week was shaped by a fresh round of economic data and continued strength in commodities, as markets digested inflation readings and geopolitical news while gold and silver extended record-breaking rallies. BTC gained +3.1%, pushing above $97,000 for the first time since mid-November before settling lower, while Gold rose +1.8% to new ATHs, NDX slipped -0.9%, and the DXY strengthened +0.4%. November PPI surprised to the upside at 3.0% versus 2.7% expected, while December CPI printed in line at 2.7%, reinforcing the view that inflation is easing, though persistent labor market weakness has yet to force near-term policy urgency.

Rates markets reflected a recalibration and hesitation of policy expectations. Treasury yields moved modestly higher at the front end, with 1M to 2Y yields up 2 to 4 bps, while the long end edged lower, leaving the curve slightly flatter overall. Short-dated yields rose after signs of labor-market resilience eroded expectations for near-term rate cuts, highlighted by an unexpected drop in US unemployment claims. Yields in the 2Y to 5Y sector, most sensitive to Fed policy, remained elevated after paring initial gains as traders trimmed bets on a mid-year rate cut and a second cut by year-end. Markets now broadly expect the Fed to pause rate cuts at the Jan. 28 meeting, with policy likely on hold until clearer signals of labor market improvement emerge.

Volatility continued its steady grind lower despite a heavy macro calendar. BTC ATM 30-day implied volatility fell -7.3% to 37, while ETH IV declined -8.5% to 53, reaching its lowest level since 2024. Notably, crypto volatility has continued compressing even as Bitcoin grinds higher, a dynamic that has historically preceded larger directional moves.

Our Take: A defining theme the last couple weeks has been Bitcoin’s relative strength versus Nasdaq, as investors rotate away from slow-moving growth equities and toward alternative risk assets. Interest rate expectations remain a key macro driver, with Bitcoin increasingly trading as a levered expression of policy optionality. With additional labor and inflation data set to hit the tape over the coming month, BTC appears well positioned to respond should incoming prints reinforce the case for a faster Fed cutting path.

Flows Flip Green

Majors begin the week with a heavy pullback, following a constructive bounce last week, with BTC up 3.1%, ETH up 5.3%, and SOL lagging, down 6.5%. Risk appetitive initially improved into mid-January, buoyed primarily by the supportive macro data, though liquidations late-Sunday night almost all but wiped this performance out. Interestingly, crypto is behaving more like a macro risk asset with buyers willing to add exposure when the data reduced near-term tail risk. We see derivatives positioning looking constructive, with BTC OI rising slightly, up 0.6% WoW, while ETH OI climbed +3.7%, consistent with traders adding exposure alongside the spot rebound. Funding stayed muted-to-positive across the week, suggesting last weeks move was more spot-led or cautiously levered. The clear read here is that upside expression skewed toward ETH beta this week rather than broad risk.

Institutional flows were standout this week, and it’s a signal we’ve been looking to see in recent market commentary outputs. Digital asset investment products recorded $1b of new inflows, driven primarily by BTC at $891m, while ETH at $97.6m, and SOL at $40.4m were also positive. This is an important reversal after a run of redemptions across late December and into the new year. While this is still relatively fragile until we see sustained inflows, it’s clear that an improved macro backdrop is translating meaningfully into institutional sentiment surrounding digital assets, now we just need the backdrop to sustain.

The sector that managed to hold on to neutral performance this week was privacy, where the sector printed 0.7% on the week, led by DASH’s sharp repricing on a wave of payments and integration headlines, hitting over 100% performance WoW during the week. These include Alchemy Pay support, as well as AEON Pay enabling merchant acceptance at scale. Aside from this, we saw sector dispersion, with most alts in the red, which reinforces that this was a selective week.

Our Take: This was a constructive week that fell at the last hurdle, which looked to our desk to be a cleaner rebound with higher majors, OI rising in a contained manner, and importantly, institutional flows back in the green. The risk remains the extent to which the move is headline-sensitive, which we are beginning to see this morning, and how quickly those headlines will be replaced.

Onchain Funding Suppressed

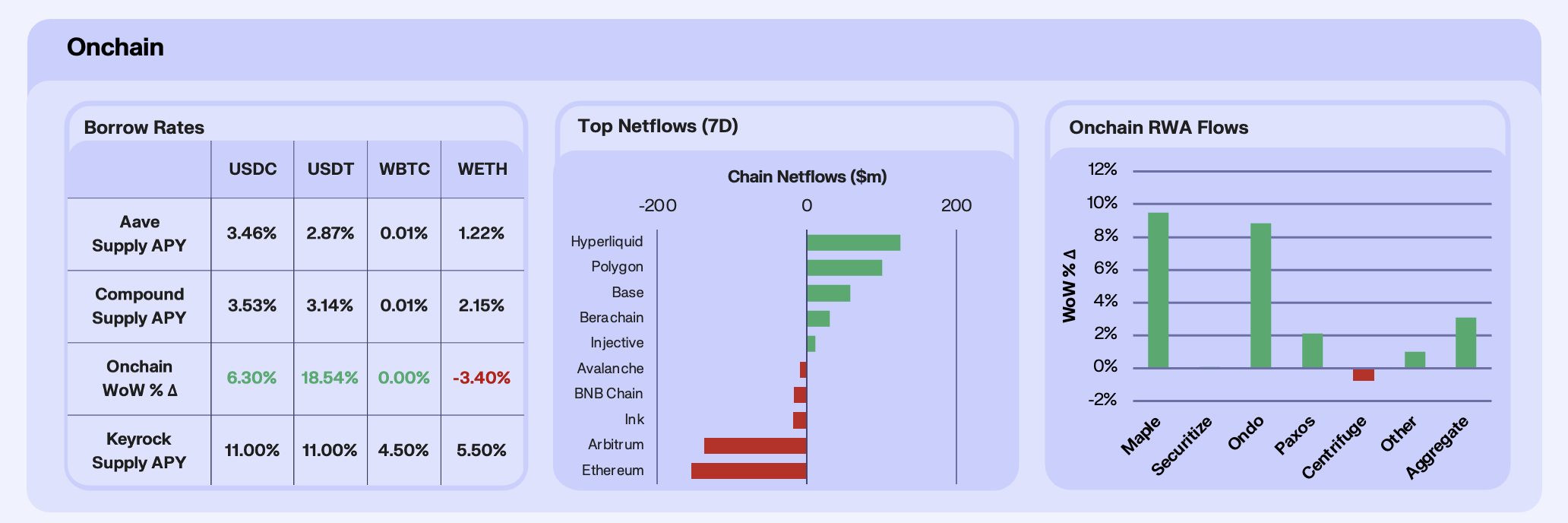

Turning out attention onchain, we saw mixed yields this week across majors, but the stablecoin complex continued to look firmer in aggregate. USDC supply APY rose 6.3% WoW, though remains suppressed, while USDT rose considerably again, up 18.5% WoW. The USDT acceleration was driven by a material supply shock, in which it saw supply fall 17.3% WoW. As has been the case the past few weeks, these moves are liquidity-driven, as opposed to demand-driven.

Chainflows reflected headlines this week, with StarkNet up $480m and Polygon PoS up $474m. Polygon’s boost came as a result of Polygon Labs announcing definitive agreements to acquire Coinme and Sequence, pushing an ‘open money stack’ narrative, centered around regulated on- and off-ramps in conjunction with wallet infrastructure on Polygon rails. StarkNet’s inflows are less exciting, with the STRK unlock on January 15th as the likely driver for the increased liquidity. Hyperliquid inflows fit the pattern we’ve seen in recent weeks, in which speculative behaviour follows price action.

RWAs saw aggregate AUM up 3.1% WoW, led by Maple, up 9.5%, and Ondo, up 8.9%. Maple’s incentive cycle appears to have pulled forward allocations into its credit rails, with the final Drips claim going live on January the 18th. Ondo benefited from a cluster of product and liquidity catalysts around tokenised equities and RWA financing, most notably Felix’s integration messaging around Ondo Global Markets.

Our Take: The onchain ecosystem is still improving, but it’s improving selectively. Stablecoin rates are doing the heavy lifting, and the liquidity picture shows this week’s strength was about constrained funding. Flows confirm capital is rotating toward execution and volatility venues, while RWAs are compounding on concrete distribution catalysts.

Early Signs of Speculation

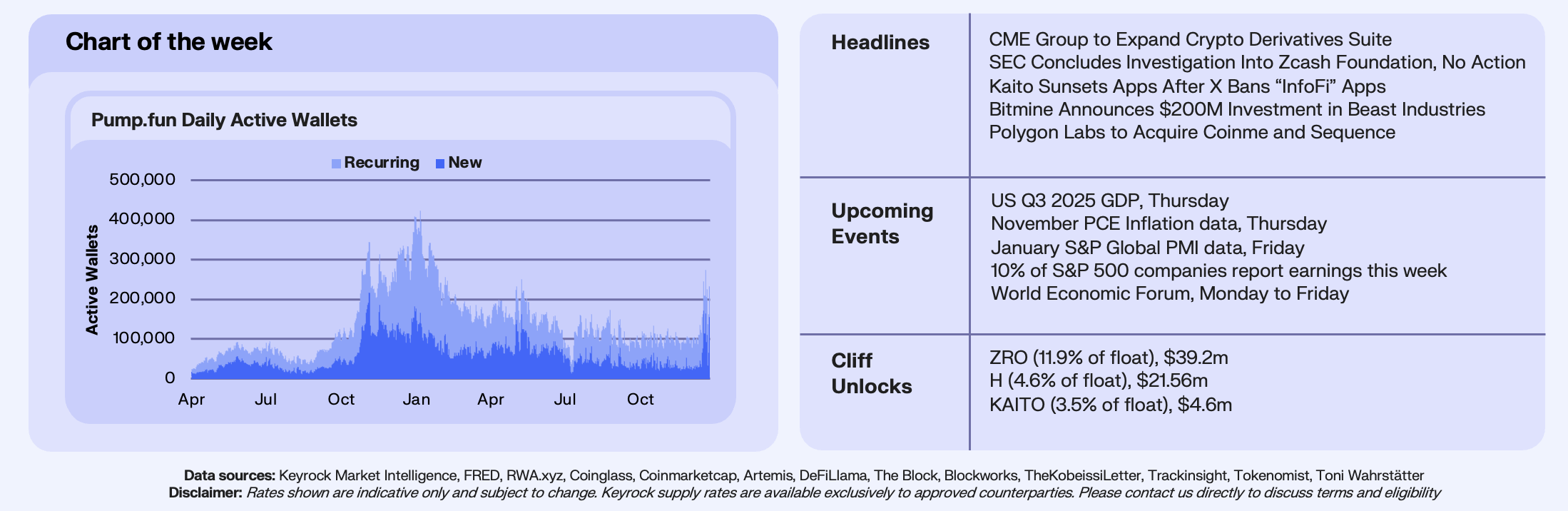

Pump.fun activity reaccelerated meaningfully this past week, with daily active wallets rising to roughly 275,000 at the peak, a level not seen since early 2025, when the platform was at its most active. That earlier period coincided with peak speculative intensity in the memecoin market, as user participation and token launches surged alongside broader risk-on conditions. The recent rebound stands out not just for its magnitude, but for how quickly activity recovered after a prolonged cooling phase.

The pickup was driven by a surge in new wallets, while recurring users remained elevated, suggesting the move was largely driven by a fresh influx of participants. Historically, spikes in new wallet activity on pump.fun have coincided with renewed speculative appetite, as users return to onchain venues that reward speed and risk-taking. After Bitcoin reclaimed $97,000, activity on pump.fun surged and remained elevated relative to Q4 2025, a sign that risk-on behavior could emerge once Bitcoin crosses $100,000.

Pump.fun can be viewed as an early grassroots signal for whether speculative energy is returning to the memecoin segment. While debate continues around the durability of memecoins, they have been a consistent feature of every crypto cycle. In periods where risk appetite turns higher, experimentation typically resumes first at the fringes, with memecoin launches accelerating before broader market participation follows.

Our Take: The rebound in pump.fun activity suggests early signs of risk appetite rebuilding at the edges of the market if Bitcoin is able to cross $100,000. While it is too early to call a full return to risk-on conditions, especially given renewed geopolitical conflict driving the tape, rising participation in memecoin issuance often precedes broader speculative engagement. With ETH open interest on Hyperliquid now exceeding its October highs, even as SOL remains below prior peaks, the setup points to selective re-risking that could broaden if macro and liquidity conditions improve.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.