11 August 2025

Key Insights, Chasing the Upside

Risk Appetite Defies Headwinds

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

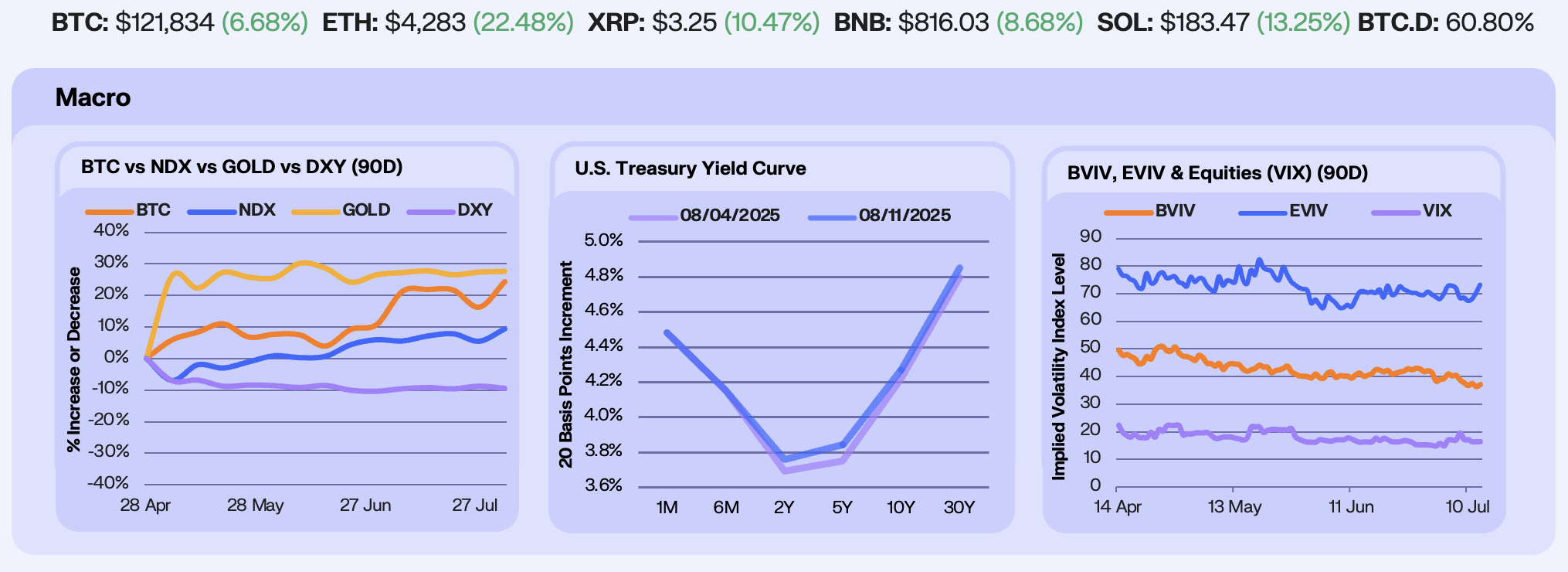

Markets digested a wave of new tariff announcements last week, including measures targeting India and the semiconductor sector. Bitcoin (+6.9%) and the Nasdaq (+3.7%) continue to shrug off weak labor data, while the Dollar fell (-0.8%) and Gold rose (+0.2%), as traders priced in a 25bp rate cut expected in September.

A weak 10-year auction and continuing jobless claims contributed to a steepening of the yield curve, as investors demanded higher returns amid concerns about stagflation, U.S. debt sustainability, and waning foreign demand. The 2Y and 5Y tenors rose 7 and 9 bps, respectively, while the 10Y and 30Y ticked up 5 bps. Front-end yields remained anchored at last week’s levels. Still, markets expect these moves could reverse if Fed cuts materialize as anticipated.

As markets rebounded, implied volatility diverged. Bitcoin’s IV fell from 38.6 to 36.5 (-5.4%), hitting a two-year low, while Ethereum’s remained elevated and climbed from 68.5 to 72.4 (+5.7%). Meanwhile, the VIX extended its decline from 19.56 to 16.48 (-15.8%) despite equities pushing to new highs, underscoring the broader suppression in volatility.

Our Take: Positioning remains mixed as resilient risk appetite runs up against persistent stagflation and debt-sustainability concerns, with traders adding upside exposure via September calls to position for further gains after the recent rebound. For the Sep. 26 expiry, the largest concentration of call open interest sits at the $140,000 strike. If rate cut expectations materialize and risk appetite holds, Bitcoin and Ethereum could extend their upward momentum through August.

Altcoin Rally Signals Maturity

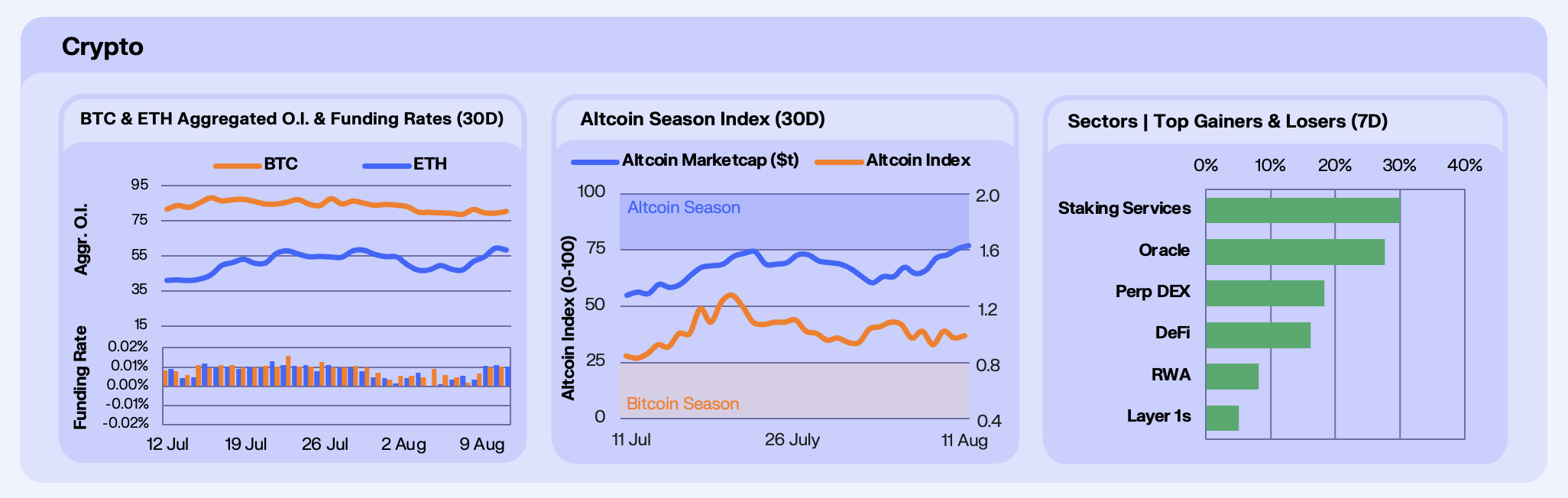

Following Bitcoin and Ethereum’s rebound last week, funding rates for both assets jumped, while Ethereum’s open interest hit all-time highs. Bitcoin’s OI rose from $79.5b to $80.1b (+0.8%) while Ethereum’s rose from $47b to $58.1b (+23.6%). The rise is especially notable as ETF flows between both assets were tepid last week, +$188.9m (BTC) and +105.4m (ETH), indicating that previously institution-driven growth is now showing increasing signs of retail participation. While retail activity appears to be picking up, Ethereum remains a key lever for institutional speculation. Large OI Holders of CME Ether Futures (≥25 contracts) climbed to an all-time high of 101, coinciding with the CFTC’s announcement of an initiative to enable trading of spot crypto asset contracts on registered futures exchanges.

Altcoins surged last week (+14%), adding $200b in market cap after sharp losses the week prior. Gains were led by Ethereum-beta plays and fundamentally strong protocols, with Staking Services, Oracles, and Perp DEXs outperforming. Despite last week’s broader slowdown, altcoins with Ethereum alignment and solid fundamentals continue to trend higher, suggesting the rally may be stickier than anticipated and reinforcing signs that crypto markets are maturing.

Our Take: Risk appetite remains firm but selective, with investors rotating into sectors showing genuine fundamental traction. The rebound in altcoins looks more than just a beta move, led instead by protocols with clear Ethereum alignment. Flows are concentrating in high-conviction themes, while incentive-driven tokens lag. With altcoins now reclaiming their July highs, the next breakout is likely to be powered by DeFi and RWA sectors, particularly those benefiting from Ethereum-beta exposure, accelerating stablecoin velocity, and tokenization tailwinds.

Rates Under Pressure

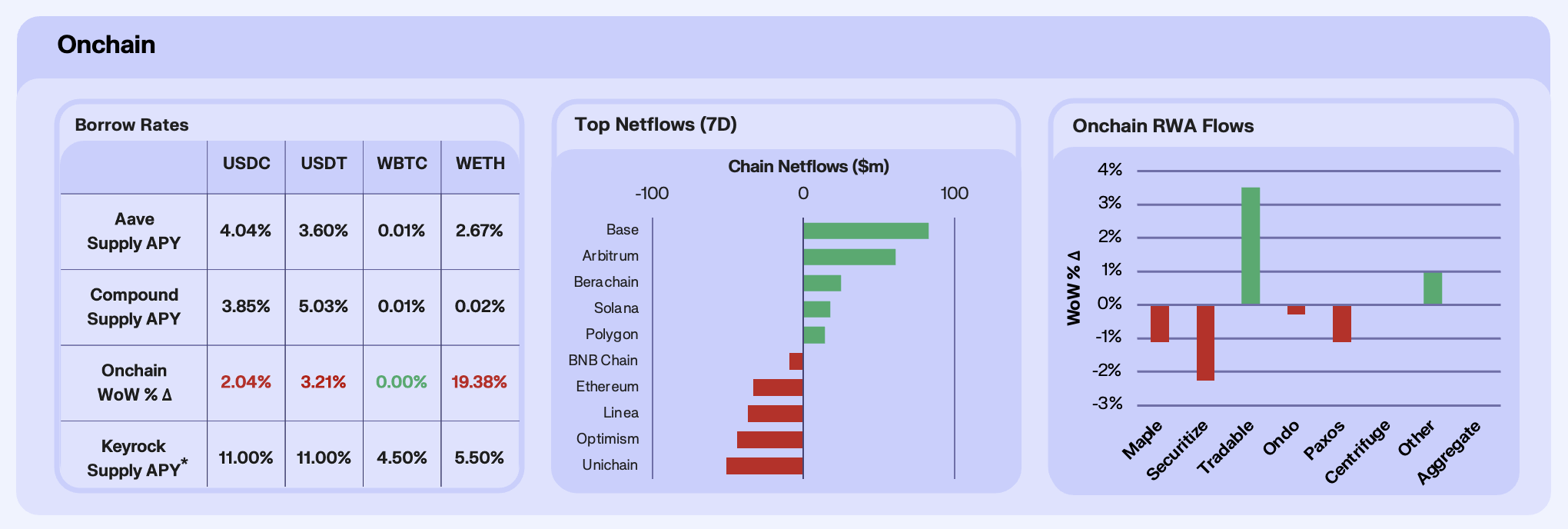

Onchain supply rates cooled across the board for majors this week, led in part by an influx of supply to lending pools. WETH exemplifies this trend, with rates down 22.3% WoW amid a 95% increase in onchain borrow capacity. USDT, for which rates are down 3% WoW, saw a capacity contraction, indicating this compression in rates is purely demand led. The rise in OI across majors paints the story here, with traders opting for leverage in perps and futures as opposed to onchain borrowing.

Chain flows show selective rotation into L2s. Arbitrum took the top spot in inflows, closely followed by Berachain and Base, each racking up tens of millions. In contrast, Unichain suffered the steepest outflows, exceeding $100m, with other mid-tier rollups like Polygon and Sonic also seeing modest exits. The pattern signals cautious repositioning rather than wholesale capital flight.

RWA liquidity was muted overall. Maple (+3.0%) and Paxos (+2.7%) gained modest traction, the majority derived from permissionless, onchain products like syrupUSDC, while Centrifuge dropped –12.5%. All-in, RWA onchain AUM dipped a slight –0.1% WoW. Looking at asset classes of onchain RWA’s, actively managed strategies grew the most in AUM this week, up ~25% amid Midas’ diversified private credit and digital asset fund pushing above $45m. Onchain stocks, up ~10% WoW, also saw strong growth, with Strategy, Nasdaq and Amazon xStock leading the growth.

Our Take: Lending markets risk drifting into oversupply unless onchain leverage demand rebounds, keeping rates suppressed near-term. L2 inflow leaders like Arbitrum and Base could see liquidity snowball into DeFi activity if perp volumes keep climbing. RWAs look primed for a breakout quarter, with permissionless credit and tokenised equities likely driving the next wave of onchain capital rotation.

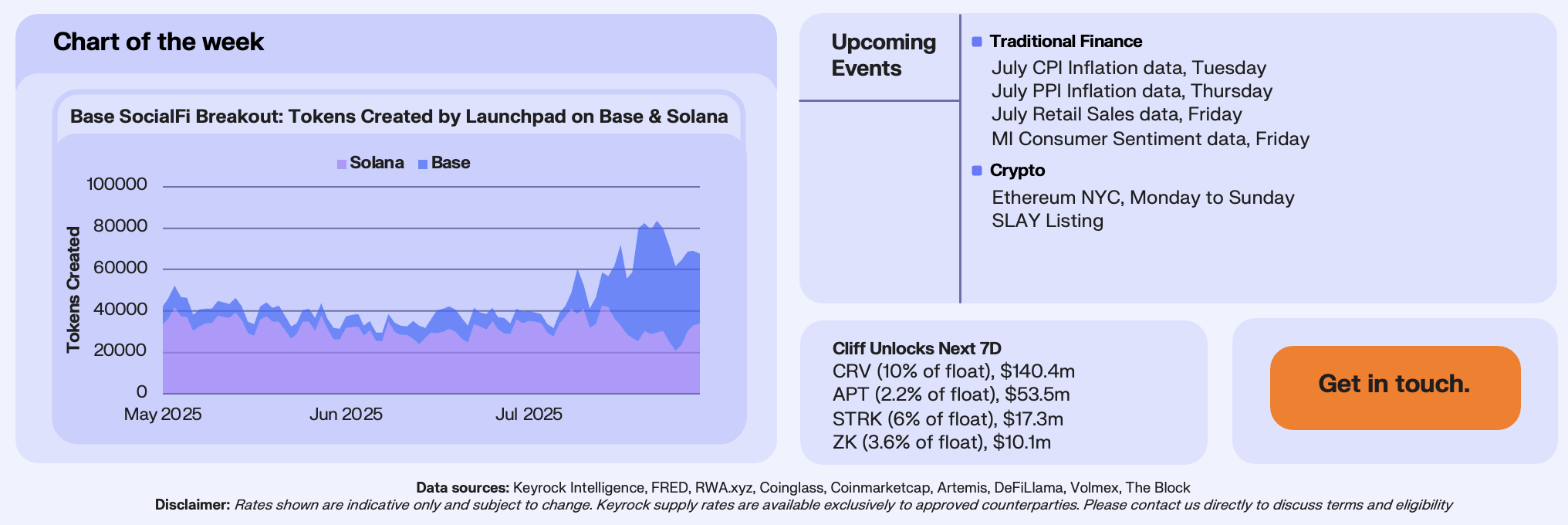

Base SocialFi Breakout

Base daily token launches surged past Solana’s in late July, peaking at ~54k on July 27th, more than double Solana’s ~25k. The lead has held for over two weeks, with Zora alone driving 64.6% of combined Base and Solana launches as of August 2, dwarfing Solana’s Pump.fun and LetsBonk. This growth comes despite Solana still commanding the lion’s share of trading activity, often generating more DEX volume than Ethereum, Arbitrum, and Base combined on peak days.

The flip is powered by Base App’s integration of Zora with Farcaster, enabling users to tokenise social posts into ERC-20s with 1b supply, auto-generated Uniswap liquidity pools, and a 1% creator fee in ZORA. This has created a frictionless social-token pipeline, turning viral posts into instant memecoins. Zora’s recent upgrades, such as lower mint fees, enhanced creator rewards, and onchain secondary markets, have supercharged adoption, positioning Base as the hub for SocialFi token creation.

Our Take: Base now leads in sheer token creation, but Solana’s unmatched execution speed and liquidity depth mean it remains the trader’s chain of choice. The key question is whether Base can translate its SocialFi boom into sustained liquidity and community retention. If it can, Base could carve out a durable niche as the go-to chain for creator-driven tokens, while Solana continues to dominate high-velocity trading.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.