2 March 2026

Key Insights: All Quiet on No Front

Geopolitics Shake Risk Assets

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

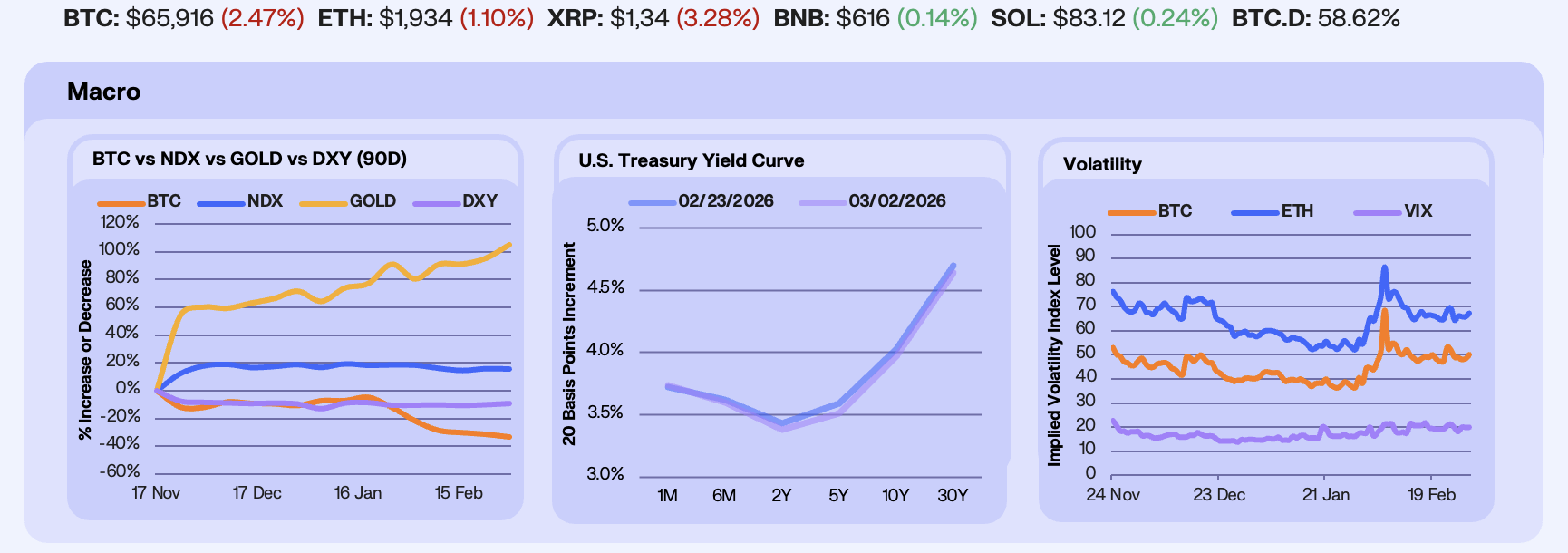

Markets navigated mixed macro and geopolitical signals this week following the U.S. military action in Iran, alongside economic data that added further uncertainty to the policy outlook. Jobless claims came in modestly below expectations and core PPI surprised to the upside, tempering rate cut expectations and sending risk assets lower. At the same time, investors are reassessing AI risk premia as software stocks underperform the broader Nasdaq by their widest margin on record. Despite a blowout NVIDIA earnings print, the stock fell, highlighting how elevated expectations have become. BTC declined -2.8% on the week after briefly breaking below $64,000 amid liquidation-driven selling, gold rose 5% and held above $5,000/oz, while the DXY gained 0.9% amid persistent U.S.-Iran tensions, and the NDX edged down -0.2%.

Rates markets delivered a repricing as bond investors weighed mixed macro signals. Yields on the 10-year dipped below 4%, near three-month lows, as traders digested softer inflation data and repositioned duration ahead of future Fed decisions, even as headline inflation remains above target and job market concerns persist. Safe-haven demand amid geopolitical uncertainty also lent support to longer maturities, contributing to a modest flattening of the curve as short-term yields held relatively firm. This is a market that is less focused on aggressive easing and more on balancing sticky inflation, geopolitical risk, and slowing growth expectations, a backdrop that has kept the Fed on hold and traders cautious on rate-cut timing.

Volatility remained elevated and term structure continued to reflect cautious positioning. BTC 30-day IV rose +5.8% to 50 and ETH IV climbed +3.8% to ~67, while the VIX ticked up about 1 point to 20. Options metrics last week show a defensive skew, with put strikes around key support zones attracting more relative demand as traders buy protection, a read consistent with reported increases in downside hedging activity. Notably, data from Deribit indicates large Bitcoin ETF holders and treasuries have been actively buying 6-12 month $60,000 downside puts, signaling institutional demand for longer-dated protection as AI-driven equity fragility bleeds into crypto positioning.

Our Take: The sustainability of AI-driven margins remains the central macro variable in the weeks ahead. Equity leadership, rate expectations, and Bitcoin’s beta are all currently tethered to confidence in large-cap tech profitability. If AI optimism stabilizes, risk assets can re-rate higher; if margin durability comes into question, volatility is likely to reaccelerate, with Bitcoin continuing to trade as a high-beta extension of tech.

Weekend Flow Shifts Onchain

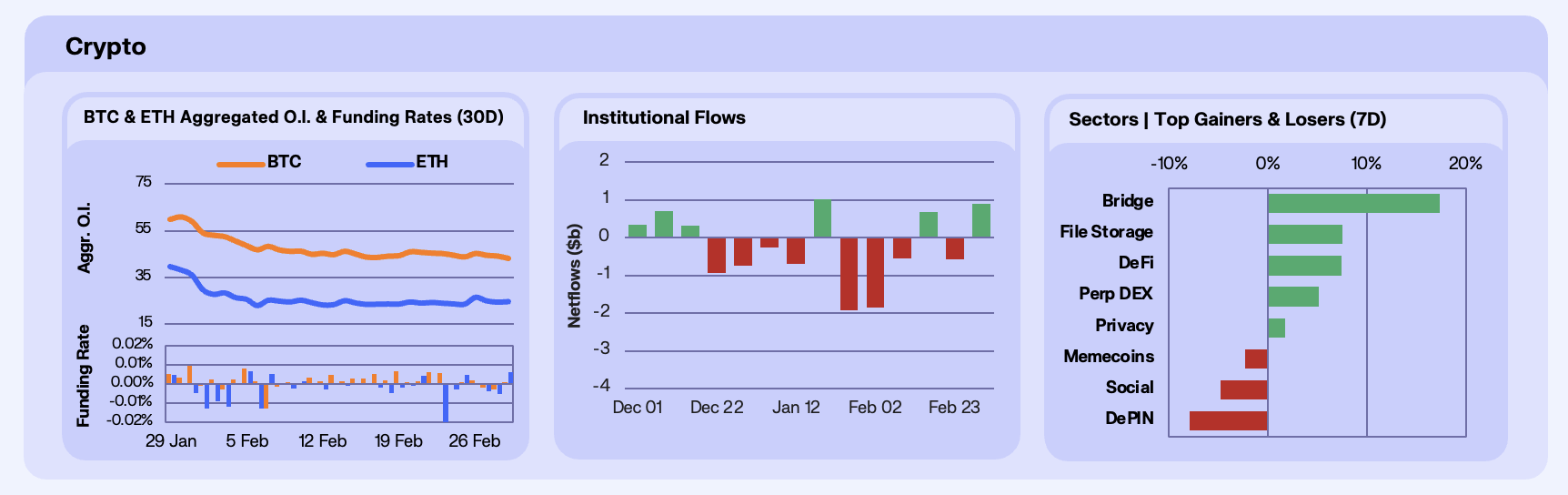

Crypto markets remained fragile as derivatives positioning turned decisively defensive. Open interest stayed leveled (BTC −5% WoW to $43b, ETH +2.9% to $24.5b), and there was a relative rebuilding in ETH positioning. Funding dynamics, however, deteriorated meaningfully. After a period of sideways rates during BTC’s consolidation between $65K and $70K, funding dropped sharply as spot briefly traded near $62K. ETH funding fell to its most negative level since the October 10 liquidation. Selling pressure has now reached its highest level in three months as funding increasingly trends negative.

Institutional flows, however, turned constructive with $900m inflows last week. Bitcoin ETFs snapped a five-week streak of net outflows with their strongest weekly performance since mid-January. IBIT accounted for over half of the three-day inflows, drawing roughly $652m, while GBTC recorded its largest single-day inflow since converting to an ETF. The Coinbase Premium Index also flipped positive after 40 consecutive days in negative territory, suggesting U.S. spot demand is re-emerging even as futures positioning remains cautious.

Altcoins staged a midweek rebound, logging their strongest daily gains after the February 25 State of the Union address. Gains were broad-based across Bridges (+17%), buoyed by ZRO after Citadel announced a strategic investment in February, DeFi (+7.4%), and Perp DEXs (+5%), driven by HYPE as traders flocked to Hyperliquid over the weekend to trade commodities and oil amid heightened geopolitical conflict in the Middle East. The continued high correlation with Nasdaq remains a headwind to sustained alt outperformance.

Our Take: Despite recent drawdowns, the structural backdrop for revenue-generating protocols continues to improve. The proposed CLARITY Act would formally delineate SEC versus CFTC jurisdiction, potentially reducing regulatory overhang and clarifying listing pathways. Meanwhile, increasing engagement from traditional asset managers in tokenized products and DeFi infrastructure signals gradual institutional normalization. While near-term volatility persists, improving regulatory clarity and maturing token value-accrual models suggest that the altcoin market is in an accumulation zone.

Onchain Barbell

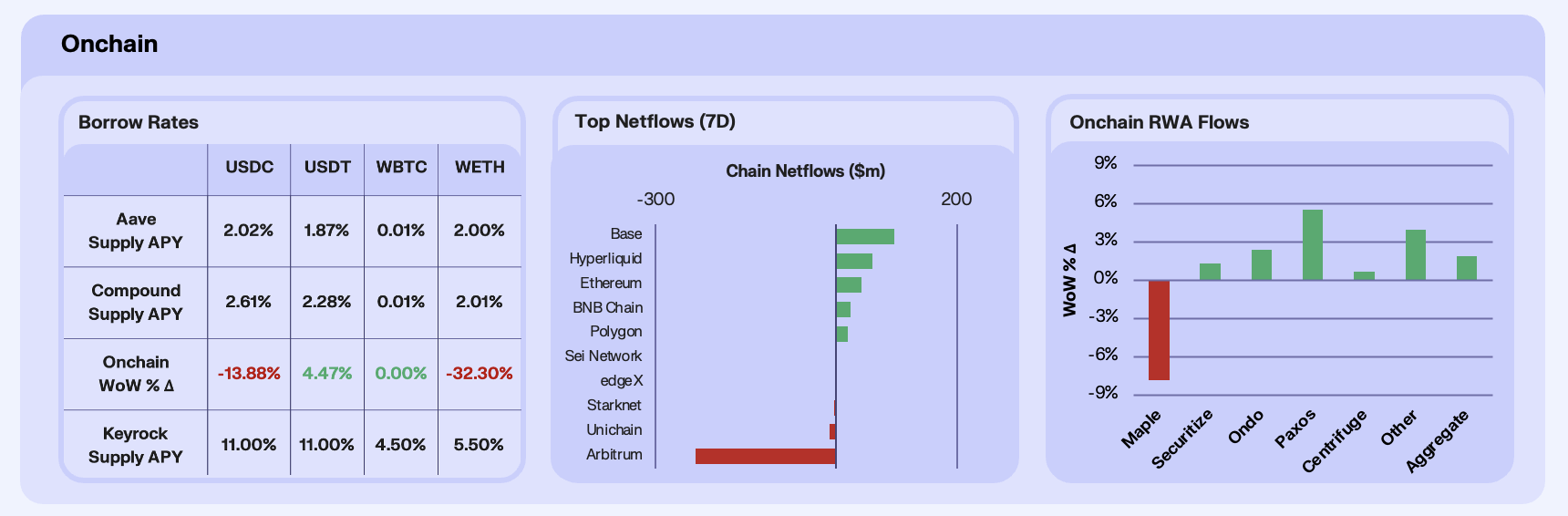

Onchain rates collapsed this week, with USDC supply yields softening by 14% and WETH by over 32%, while USDT firmed modestly Rate returns on the week suggest dollar liquidity is returning unevenly across stablecoins, favouring the more regulated USDC. The more notable signal was the influx of supply on ETH, consistent with a market that is still de-grossing ETH beta and expressing risk selectively, rather than recycling stables into broad onchain looping.

Chain flows reinforced that interpretation where we saw capital rotate toward clear ‘winner’ venues with concrete catalysts. Base (+$97m) led inflows as markets continued to price in the implications of its recent move toward a more independent, unified stack that allows for faster iteration and clearer long-run control while remaining Ethereum-aligned. Hyperliquid (+$61m) also absorbed fresh capital, helped by a genuinely institutional on-ramp moment of CoinShares’ physical Hyperliquid staking ETP launch and a weekend volatility impulse that tends to push traders into always-on perps when traditional markets are shut. Ethereum (+$42m) saw modest stabilisation, while Arbitrum (-$235m) stood out on the downside as distribution and competitive rotation dominated, with flows preferring higher-momentum ecosystems.

RWAs remained net positive (+1.89% WoW), but the composition varied drastically, in what we see as a clean risk-off barbell inside RWAs. Paxos (+5.56%) did most of the work as tokenised gold absorbed the geopolitical hedge bid, while Securitize (+1.31%) continued to grind higher on steady demand for liquid, onchain Treasuries. Ondo (+2.41%) benefited from its tokenised securities landing on Binance Alpha, while Centrifuge (+0.69%) saw targeted support from institutional-style product plumbing with a $100m JAAA strategy deployment into DeFi rails. In contrast, Maple (-7.82%) retraced as allocators pulled back from the private-credit sub-sector.

Our take: With the geopolitical events that took place this week, it was unsurprisingly a choppy week for the onchain economy. The selective risk expression reflected this, with some traders opting for high volatility venues in Hyperliquid, and other opting for risk-off positions like Paxos gold. The next upside tell we’re watching for is utilisation-led rate strength, as opposed to the headline-driven flows or liquidity shocks that have dominated the year to-date.

FIDD Finds Velocity

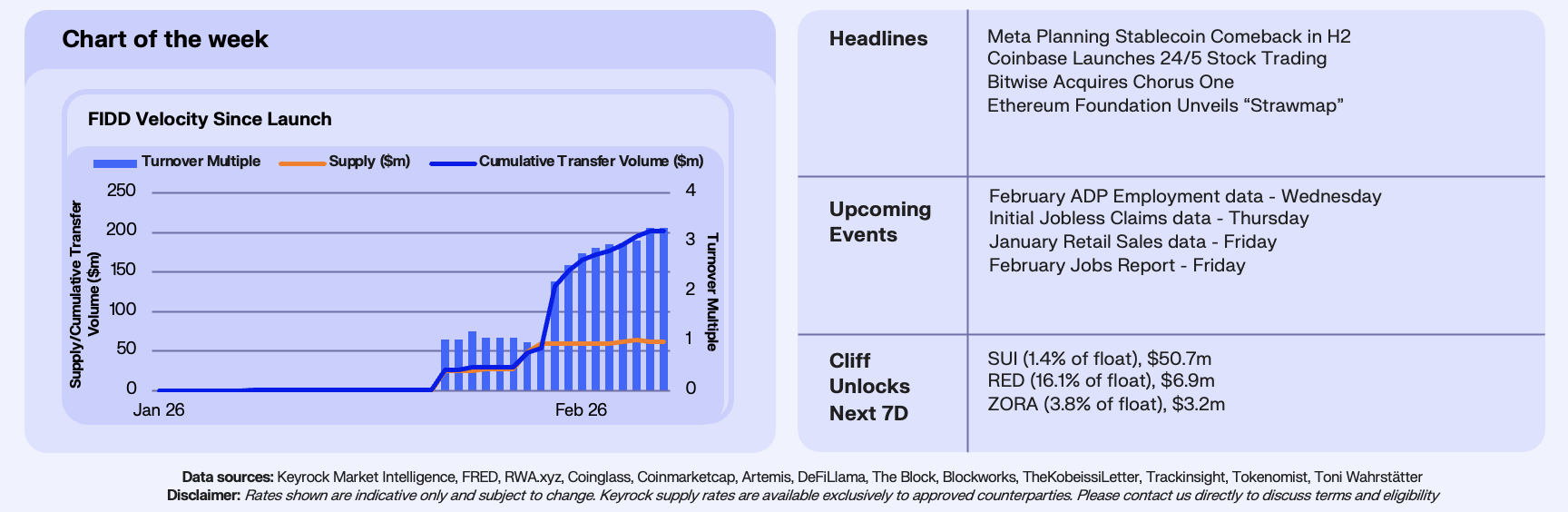

This week’s chart looks at Fidelity’s Digital Dollar (FIDD) onchain activity, breaking down supply, transfer volume, and the underlying transaction and active wallet counts. For context, Fidelity positions FIDD as a dollar stablecoin designed for payment and settlement use cases across its platforms. Despite still being early in its lifecycle, FIDD supply has already reached $61.5m, while cumulative transfer volume has climbed to $202.3m, with several standout daily spikes in activity.

The headline statistic for FIDD is velocity, in line with its institutional positioning. Cumulative transfers are already at 3.3x circulating supply, implying FIDD is being utilised onchain rather than simply warehoused. The pattern of bursty volume is consistent with institutional-style settlement flows of large average ticket sizes, a refreshing sight from retail payments or long-tail DeFi activity logging miniscule transfer volume size. That’s directionally what you’d expect from a Fidelity-distributed stablecoin early on, with fewer wallets, but higher-value activity as access ramps and initial use cases concentrate around treasury movement, exchange transfers, and internal platform settlement.

Our Take: FIDD represents distribution, trust and compliance in a stablecoin, leveraging the stellar corporate reputation of Fidelity Investments. The early data is already pointing to institutional utility over the retail adoption often seen in stablecoins without this privilege. The core metrics we’re watching for continued success here is velocity holding up as supply expands, which would signal sustained and growing real settlement demand.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.