29 December 2025

Key Insights: All About That Hedge

Real Assets Assert Leadership

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

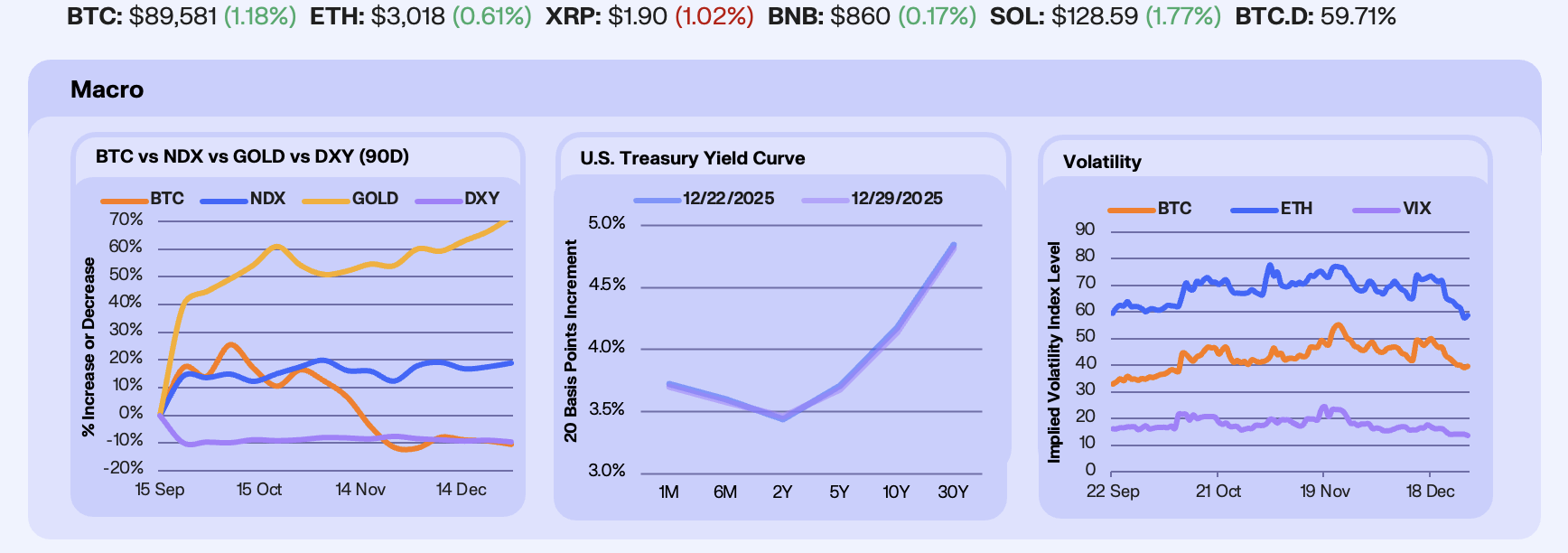

Last week was defined by a powerful continuation in real assets. Precious metals posted a historic run, with silver breaking above $79/oz for the first time ever, Gold clearing $4,500/oz, and copper printing fresh all-time highs. Markets digested this inflation-hedge impulse as BTC fell -1.4%, gold rallied +3.2%, NDX gained +1.2%, and the DXY weakened -0.7%.

Rates markets responded primarily through the lens of growth resilience. US Q4 GDP accelerated to 4.3% QoQ, sharply above expectations of 3.3%, prompting investors to reassess the pace and depth of future easing. Over the week, the front end eased modestly and the long end flattened, with 10Y and 30Y yields down ~3 bps. Markets are now pricing roughly 50 bps of Fed cuts for 2026, reflecting confidence in sustained nominal growth.

Volatility continued to compress across both crypto and traditional markets. Options markets priced meaningfully less uncertainty, with BTC IV down -10.4% , ETH IV down -11.8%, and the VIX falling -6.9%, hovering near year-to-date lows. Notably, crypto volatility compressed even as prices consolidated, suggesting positioning is being rebuilt rather than unwound.

Our Take: As we head into 2026, macro risk is being repriced lower, and liquidity conditions are improving. With QT ended, US midterms approaching, and retail participation at record highs, crypto looks well-positioned. Notably, the gold–BTC divergence is back at 2024 lows, a level that has historically preceded renewed crypto outperformance.

Liquidity Constrains Momentum

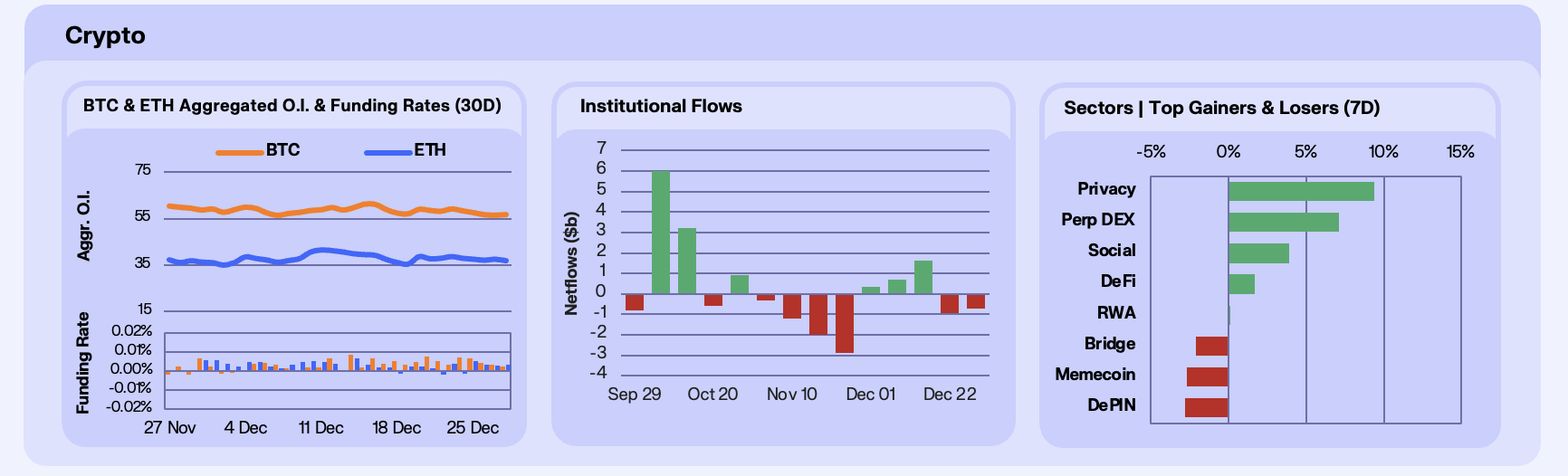

Derivatives positioning drove the week’s crypto narrative. After BTC reclaimed $90,000 and ETH pushed back above $3,000, funding rates briefly surged to their highest levels since November. Open interest declined on the week, with BTC OI down -2.67% WoW and ETH OI down -2.81%. This reinforces the view that participants remain tactically positioned and unwilling to chase upside in a low-liquidity environment.

Institutional flows turned negative on the week, with net outflows of -$736m, driven primarily by redemptions in Bitcoin-linked products. While the near-term signal looks challenged heading into 2026, total assets across digital investment products remain elevated at approximately $113.8bn, highlighting that recent withdrawals reflect positioning adjustments rather than a breakdown in institutional engagement.

At the sector level, privacy led the complex (+9.4%), with ZEC at the forefront as the privacy meta continues to assert itself as a durable 2026 theme. Perp DEXs (+7.1%) also outperformed, led by HYPE (+7%), as token unlock concerns faded and attention shifted toward the Lighter TGE and the conclusion of its pre-TGE trading incentives. In contrast, more speculative segments lagged, with Memecoins (-2.7%) under pressure, underscoring investors’ preference for the revenue narratives.

Our Take: Crypto continues to trade choppy, but the underlying structure is improving. Liquidity remains thin, and much of the macro uncertainty that weighed on markets earlier this year, from tariffs to government shutdown risk to questions around US economic durability, is still being digested. In that context, with positioning cleaner, the setup increasingly favors patience over momentum chasing as the market builds a base for the next phase.

Selective Re-Risking

Onchain rates continued to soften. Stablecoin supply yields moved lower, with USDC and USDT APYs down -4% and -6% WoW, driven primarily by increased stablecoin supply rather than a resurgence in borrowing demand, consistent with capital being parked defensively as risk appetite stabilized. The mix remains more supply-driven than demand-led, but the relative improvement in ETH rates is consistent with early-stage re-risking rather than outright leverage expansion.

Chain netflows reflected broad dispersion, but with a clear leader. Arbitrum (+$1.7bn) saw the largest net inflows on the week, driven in part by users depositing capital onto Arbitrum as a staging ground for activity on Hyperliquid, a dynamic that points to traders beginning to re-risk selectively rather than exiting onchain entirely. Outflows were concentrated in Ethereum (-$827m) as the flow profile continues to prioritize execution. RWA flows weakened at the aggregate level, with total AUM down -12.86% WoW, driven largely by drawdowns in smaller and non-core allocations. Within that, Paxos (+7.05%) stood out, benefiting directly from the sharp rally in gold and precious metals, which continues to drive demand for tokenized commodity-linked products. Maple (+2.82%) and Ondo (+0.83%) also attracted modest inflows, while Securitize (-0.30%) remained broadly flat, suggesting the pullback reflects rotation and rebalancing rather than waning structural interest in RWAs.

Our Take: Onchain signals suggest risk appetite is building selectively. Capital is beginning to deploy toward equity perpetuals, where leverage offers opportunity amid the ongoing run in equities, while tokenized precious metals are emerging as the clearest real-world bridge for RWA adoption amid the surge in gold and silver. Together, these two vectors represent the most immediate sources of incremental onchain demand.

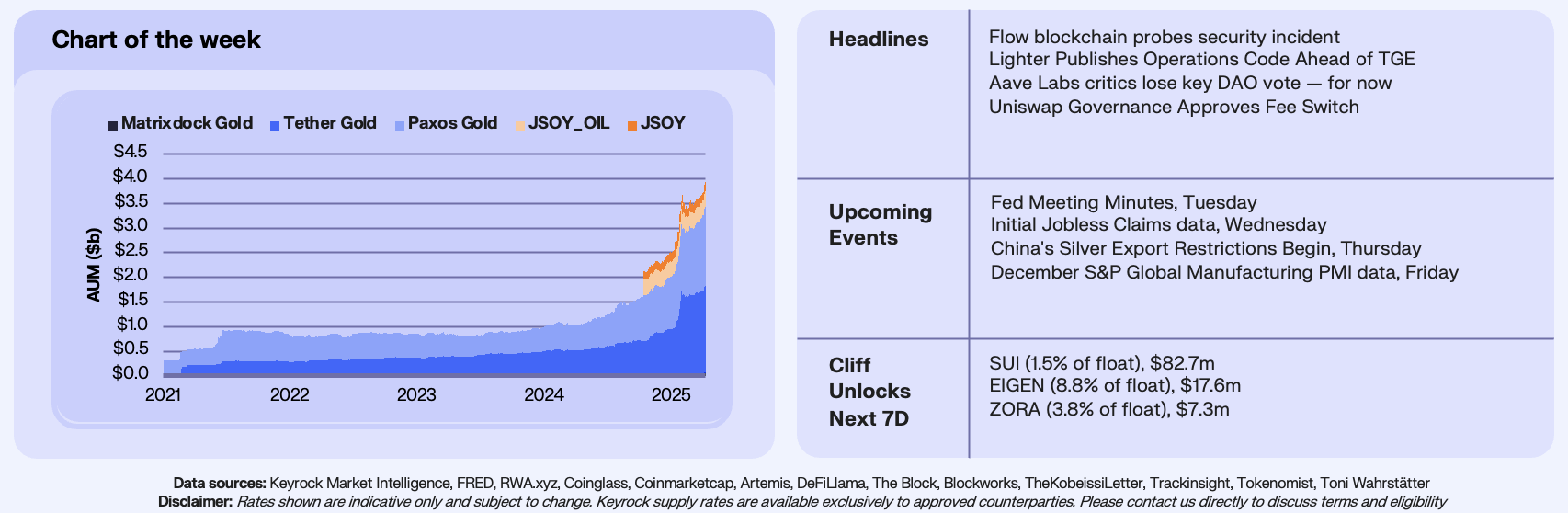

Tokenized Commodities Hit Scale

The surge in commodities has been one of the defining macro themes of the year, and it has accelerated meaningfully since the end of QT. Broad-based strength across precious metals and industrial commodities has pushed gold, silver, and copper to all-time highs, driven by a combination of elevated geopolitical risk, renewed safe-haven demand, and easier monetary conditions. With the Fed pivot complete and markets increasingly pricing additional easing into 2026, non-yielding real assets have reasserted their role as macro hedges. Layered on top of this is a persistent structural supply tightness across several key commodity markets, reinforcing the durability of the move rather than framing it as purely cyclical.

That backdrop has translated directly onchain. Tokenized commodities have reached exit velocity, with total AUM nearing $4B, an all-time high. The market remains highly concentrated, with Tether Gold (~$1.76B) and Paxos Gold (~$1.63B) together commanding over 85% of total tokenized commodity AUM. The growth profile has steepened notably over the past year, reflecting both rising underlying commodity prices and growing comfort with tokenized wrappers as liquid, onchain access points to real assets. Importantly, this growth has occurred alongside broader RWA adoption, but at a pace that now clearly separates commodities from other RWA verticals.

Our Take: Tokenized commodities are shaping up to be the least volatile and most durable segment of RWAs. While gains may not compound at the same pace seen during the sharp repricing of 2025, the trajectory remains structurally higher over time. As more commodities move onchain and distribution expands across wallets, venues, and institutional channels, tokenized commodities are likely to continue absorbing capital steadily.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.