5 January 2026

Key Insights: A Quiet Kickoff

Risk Shrugs Headlines

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

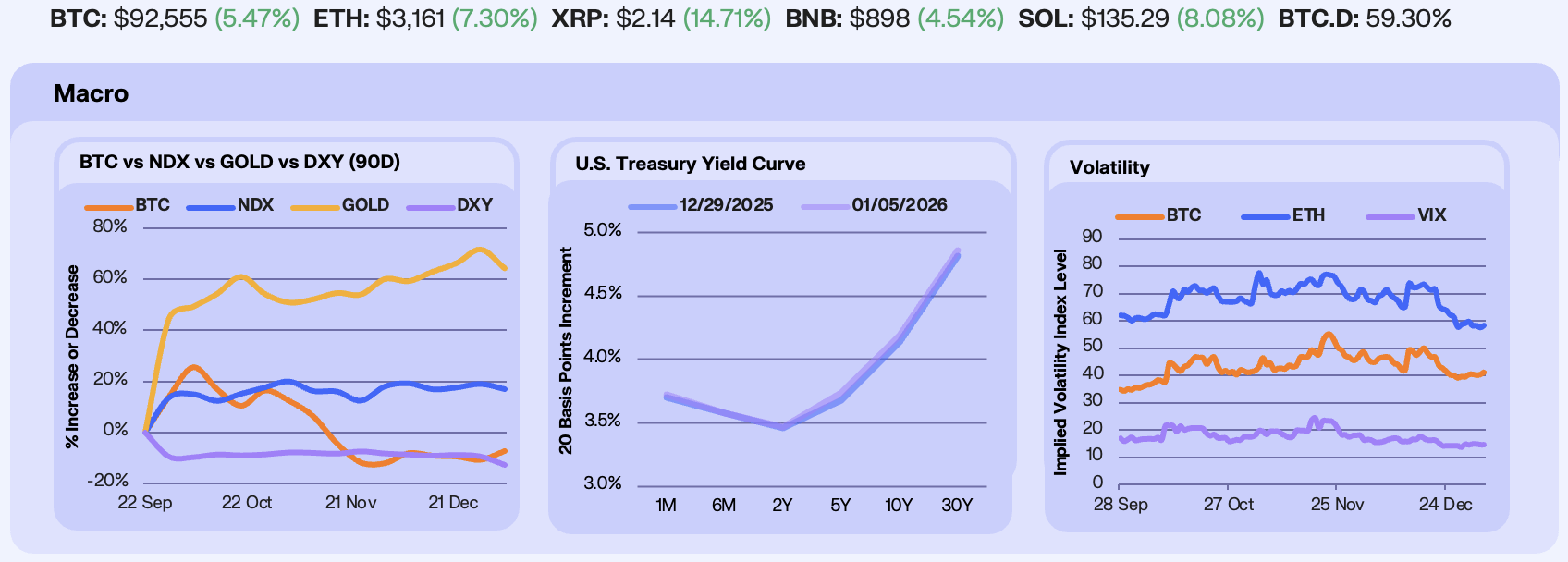

Last week unfolded against a backdrop of rising geopolitical tension, as the US administration arrested Venezuelan president Nicolás Maduro, raising concerns around energy supply and broader geopolitical spillovers. Despite the headline risk, markets remained notably composed. BTC rallied +5.4%, while gold fell -4.31%, NDX declined -1.71%, and the DXY weakened -3.69%. Energy markets were less sanguine, with oil slipping back below $57/bbl, nearing its lowest levels since 2021, and US natural gas kicking off 2026 with losses.

Rates markets edged higher across the curve, reflecting a subtle repricing of duration risk. The front end was little changed, while the belly and long end moved modestly higher, with 10Y and 30Y yields up ~5 bps WoW. Looking ahead, 2026 introduces a growing risk that premature rate cuts from an increasingly dovish Fed could push longer-term yields higher, particularly if inflation expectations reaccelerate.

Volatility continued to compress across assets. BTC ATM 30-day implied volatility rose +4.18%, while ETH IV fell -1.27% and the VIX declined -1.23%, leaving equity and crypto vol near recent lows. The calm stood in contrast to the geopolitical developments over the weekend and reinforces how little risk premium is currently embedded in markets. Historically, similar periods of compressed crypto volatility have often preceded renewed price turbulence rather than prolonged stagnation.

Our Take: Markets appear to be moving through a corrective phase that could extend into Q1, with price action digesting both macro and geopolitical uncertainty. However, with the Fed already on a rate-cutting path and preparing to expand its balance sheet via short-term Treasury purchases, the policy backdrop remains highly accommodative. Add to that the likelihood of a more politically aligned Fed leadership under a Trump administration, and the risk of inflation re-emerging later in 2026 becomes increasingly tangible. In that environment, both Bitcoin and gold may face near-term headwinds.

New Year Bounce

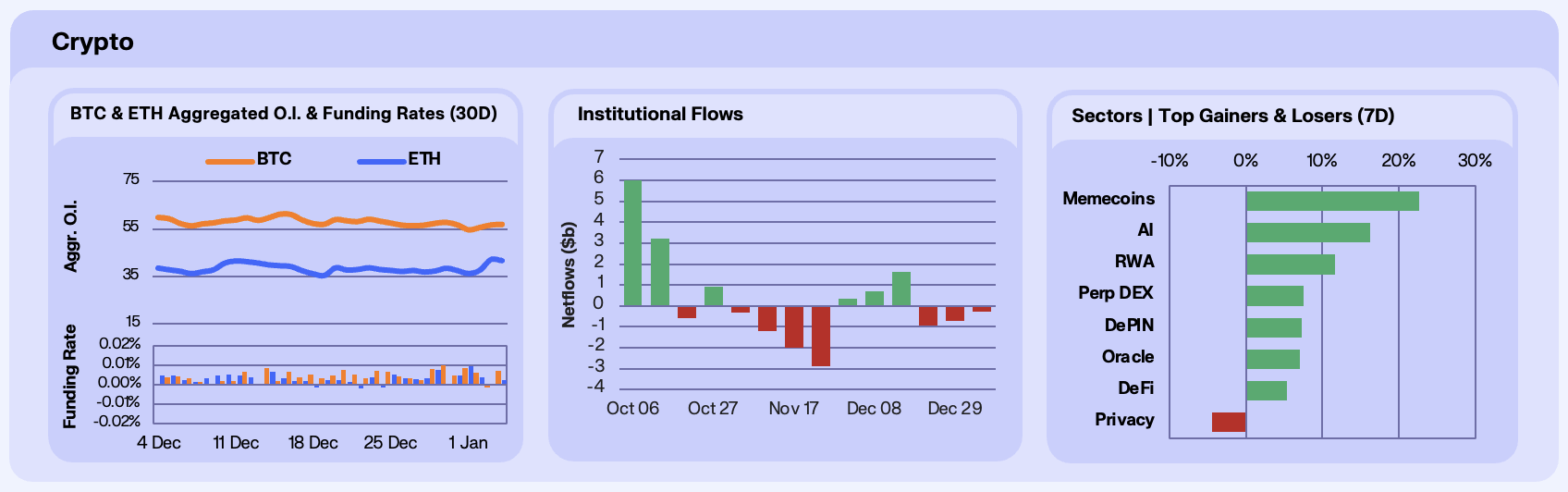

As traders return to their monitors following the festive celebrations, crypto markets have opened the year with positivity. We have seen a broad-based rebound, led by high-beta assets, as sentiment improved into thin year-end liquidity. December’s defensive close appears a fleeting memory, as majors are up in unison, with BTC rising 5.4% WoW, ETH by 7.3%, and SOL outperforming at +8%. In our opinion, narrative has followed price here, rather than the other way round. Unbias shows consensus turning decisively constructive, with BTC polling ~63% bullish and ETH ~65% bullish over the past 7 days, reflecting growing confidence that the year-end macro pressure is easing. While participation remains selective, the tone across majors improved meaningfully relative to the prior two weeks.

Derivatives positioning showed a nuanced reset relative to price’s clear directional move. BTC open interest declined modestly, down 1.5% WoW to, suggesting spot-led gains rather than leverage chasing, while funding oscillated around neutral with brief negative prints midweek. In contrast, ETH OI expanded considerably, up 8.4% WoW, accompanied by consistently positive funding, signalling renewed speculative interest concentrated in ETH. The divergence suggests traders are expressing upside views through ETH rather than broad beta, aligning some core bullish narratives, such as the ETH validator bullish as 745k ETH enters staking, which historically has preceded 90+% rallies, and a 21d MA breakout for the blue coin.

Institutional flows remained a headwind, though pressure eased versus late December. Digital asset investment products saw ~$264m of net outflows, driven primarily by BTC (-$168m) and ETH (-$64m), extending the run of redemptions into the new year. SOL also saw modest outflows (-$32m), though price action suggests marginal flows mattered less amid thinner liquidity. The disconnect between positive spot performance and continued institutional selling reinforces that the early-January bounce has been driven by sentiment reset and positioning cleanup, though our desk views the shift in momentum as a positive sign that reflects broader market optimism.

Sector performance reflected a decisive rotation down the risk continuum, something we have not seen on a sustained basis in a while. Memecoins led with a +22.7% WoW surge, followed by AI (+16.2%) and RWAs (+11.7%), signalling a return of speculative appetite after December’s de-risking. Perp DEXs (+7.6%), DePIN (+7.3%), and Oracles (+7.0%) also participated, pointing to renewed interest in both high-beta and infrastructure-adjacent narratives. Privacy was the sole laggard (-4.4%), likely reflecting profit-taking after outsized 2025 gains, as capital rotated away from defensive narratives toward momentum-driven trades.

Our Take: The first week of 2026 marks a clear sentiment reset, starting the year off on a positive note. Price strength across majors, improving narrative consensus, and ETH-led leverage rebuild point to a market willing to re-engage, but institutional flows remain net negative and participation is still uneven. This looks clearly a risk-on rotation driven by positioning, liquidity, and narrative relief rather than fresh capital. Sustained upside will require confirmation, we would imagine via institutional inflows or broader macro follow-through, but the tone has improved meaningfully versus December’s close.

Onchain Reset Begins

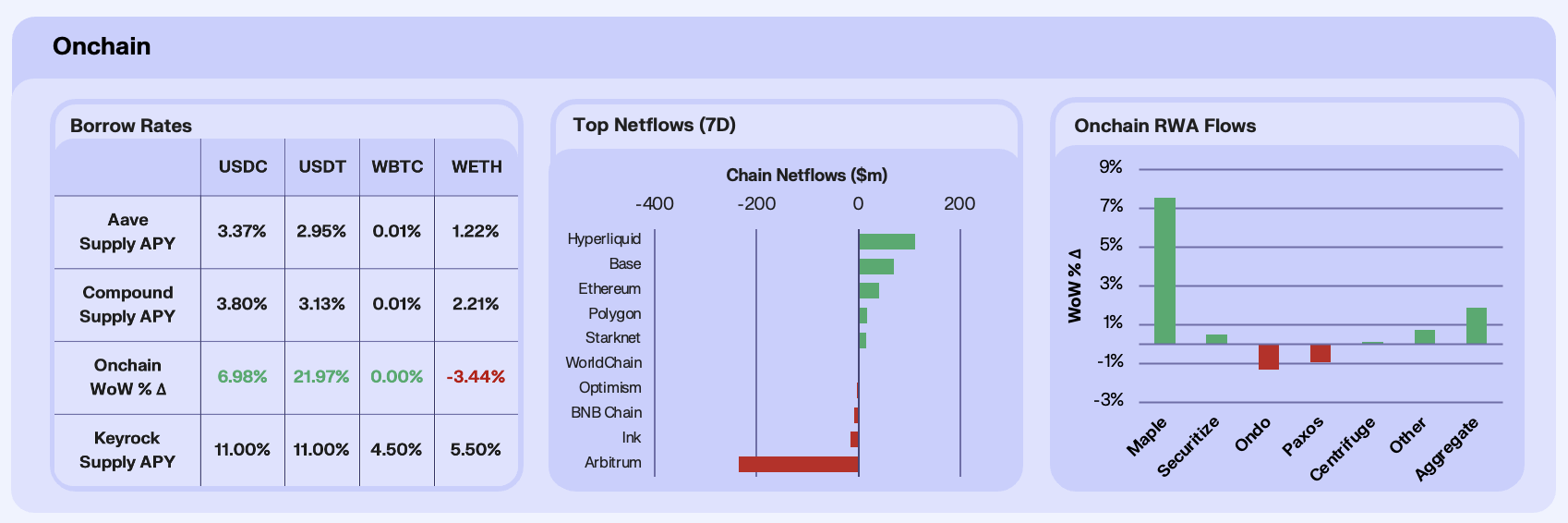

Turning our attention to onchain, borrow rates and onchain yields firmed modestly this week, marking a clear shift away from December’s defensive positioning. Stablecoin rates moved higher on a WoW basis, with USDC up ~7% and USDT up ~22%, suggesting improving utilisation as capital rotated back into onchain activity. Beneath the surface, the drivers diverged for the two largest stables, for USDC supply fell sharply on Aave, down 24% WoW, pointing to supply-led pressure, not renewed borrowing demand. For USDT, rates rose alongside stable utilisation, consistent with demand-led borrowing as traders repositioned into early-January strength. Borrowing conditions for volatile assets remained muted, with WBTC and WETH rates broadly unchanged, reinforcing that leverage appetite remains concentrated in stables rather than directional crypto exposure. We believe this looks less like a leverage rebuild and more like capital cautiously re-engaging via low-risk funding channels.

This week’s chain netflows reflected early-year rotation. Base (+$63.6m) and Ethereum (+$57.5m) led inflows, with Base benefitting from retail-driven activity in its low-fee environment, and Ethereum continuing to absorb capital as the primary settlement layer for stablecoins and institutional DeFi. Hyperliquid also saw strong inflows (+$54.7m), consistent with renewed speculative engagement following BTC’s sharp recovery into the new year. In contrast, Arbitrum (-$173.9m) saw significant outflows, a combination of bridging to Hyperliquid, and allocations towards higher-beta execution venues. The dispersion highlights that capital is reallocating selectively, favouring either liquidity depth or volatility exposure.

RWA flows turned modestly positive at the aggregate level (+1.9% WoW) to kick off the year, signalling yet another sub-sector showing stabilisation after a volatile December. Maple stood out with a +7.6% increase in AUM, reflecting renewed demand for private credit as investors sought duration and yield following lingering macro uncertainty. Securitize and Centrifuge saw small but steady inflows, consistent with continued institutional interest in compliant tokenised securities and structured finance. By contrast, Ondo and Paxos recorded mild outflows, suggesting some rotation away from treasury-style liquidity products toward higher-yield credit RWAs as risk appetite improved at the margin.

Our Take: Onchain activity improved meaningfully to start the year, but the behaviour remains measured. Stablecoin rates rising alongside muted crypto borrowing suggests capital is re-engaging cautiously, preferring flexibility over leverage. Chain flows show selective risk-taking, while RWAs continue to act as a structural beneficiary of institutionalisation and regulatory clarity. This feels like an early-January reset driven by positioning and liquidity normalisation.

Bitcoin Volatility Compresses

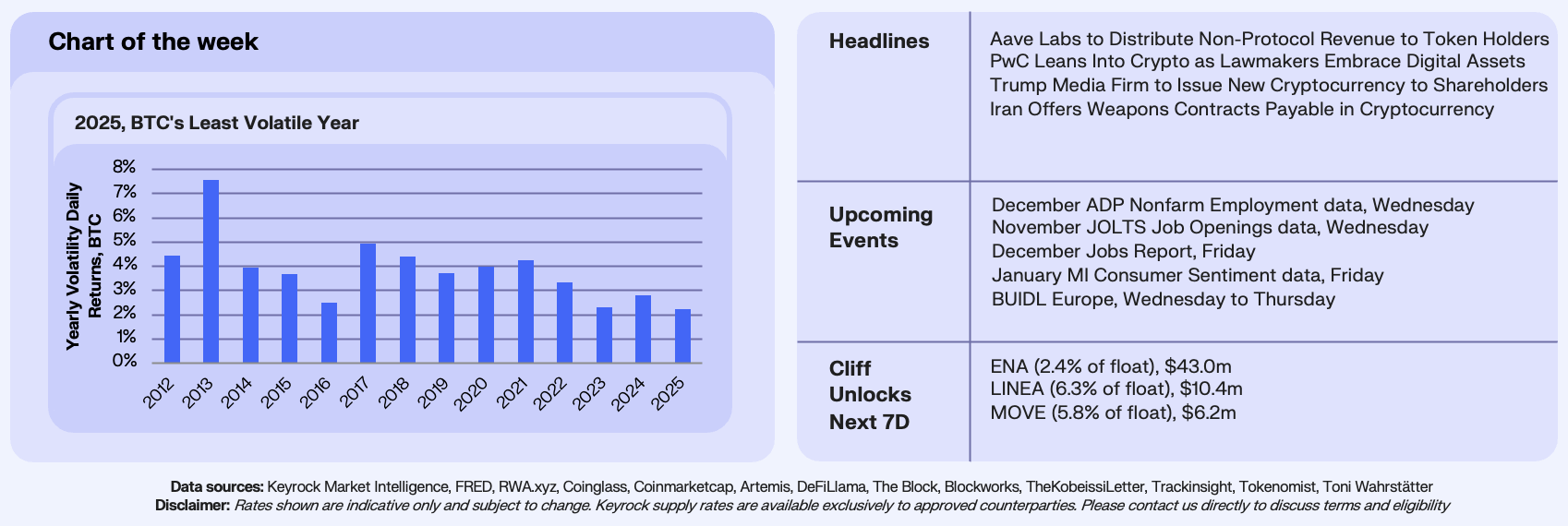

Bitcoin just recorded the least volatile year in its history. According to K33 Research, BTC’s volatility, measured by the average deviation of daily returns, fell to just 2.24% in 2025, the lowest level on record. After volatility peaked in Bitcoin’s early years, it has steadily compressed over time.

This downward trend reflects a market that is increasingly institutionally anchored. As Bitcoin has grown and participation in crypto has broadened, large price swings driven by reflexive speculation, regulatory uncertainty, and fragmented liquidity have become less frequent. BTC is trading like a macro asset, responsive to liquidity, rates, and risk appetite.

Our Take: Bitcoin’s lower volatility is the consequence of maturation. Many of the existential questions that once drove extreme volatility (activity, regulation, legitimacy, etc.) have largely been resolved, particularly with the emergence of spot ETFs and the start of crypto’s institutional era. As this process continues, assets like ETH and SOL are likely to follow a similar path toward volatility compression. That said, this dynamic remains far from reaching the long tail of crypto, where thinner liquidity and unresolved narratives mean volatility will remain a defining feature for years to come.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.