What are Stablecoin payments? A guide

Stablecoin Payements

Stablecoins have moved far beyond their origins as tools for crypto traders. Today, they are becoming the backbone of a new payments infrastructure, one that promises faster settlement, lower costs, and broader financial access across borders. But to understand this shift, it’s not enough to think of stablecoins only as digital dollars. The real transformation lies in how they move, the rails they run on, and the systems being built around them.

This guide explores those rails. We start with the “stablecoin sandwich” model, a simple but powerful framework for rewiring payments through onchain transfers, and show how it set the stage for stablecoin-linked virtual USD accounts.

From there, we trace the evolution of stablecoin payment platforms into full-stack financial networks, where users can now save, spend, earn, and transact entirely within stablecoin-native systems. What emerges is a picture of money that’s not just more efficient, but fundamentally reshaped: who controls it, how it flows, and what it unlocks for businesses and consumers worldwide.

Stablecoin Virtual Accounts

Stablecoin rails enhance existing payment systems by allowing users to bypass parts of the legacy banking payments stack. In doing so, they cut out layers of intermediaries and build a more unified financial infrastructure that links everything from currency issuance to point-of-sale transactions.

As stablecoins shift from their original trading purpose toward mainstream payments, stablecoin payment companies are simultaneously transforming into comprehensive payment networks. These platforms reach consumers directly and enable users to save, spend, earn, and send money on a single platform.

The ‘Stablecoin Sandwich’ model streamlines cross-border payments through three layers: fiat currency on one side, stablecoins in the middle for transfer, and fiat currency on the other side. This replaces the middle layer of correspondent banks with a simple bridge.

- Onramp: Sender converts their local fiat (e.g., USD) into a stablecoin (e.g., USDC).

- Transfer: The stablecoin is then transferred onchain to an address or “virtual account”

- Offramp: The recipient’s stablecoins are converted into their local fiat (e.g., BRL) for withdrawal or use

To make this model more accessible, scalable, and bank-compatible, companies began layering in stablecoin virtual accounts: digital USD accounts that mimic the functionality of U.S. bank accounts but run entirely on stablecoin infrastructure.

“We’ve used the stablecoin sandwich model with PSPs like dLocal for years. What’s evolving now is orchestration. Layer1 automates flow between wallets, ramps, venues, and banks. As more assets get tokenized, this coordination layer becomes essential. Stablecoins will increasingly displace local rails, but near-term transactions still involve fiat, making orchestration the core capability for scaling.” — Chris Harmse, Co-Founder and CBO of BVNK

BVNK was one of the earliest companies to operationalize this model by combining stablecoins with named, non-custodial virtual USD accounts. This allowed users to seamlessly convert between fiat and stablecoins. Virtual accounts offer a key benefit for banks. By enabling self-custody, they sidestep local banking systems and reduce exposure to any single jurisdiction.

This model removes reliance on local or correspondent banks for dollar deposits. Because stablecoins sit outside the banking system until needed for settlement, users avoid delays, visibility issues, and compliance burdens. Funds remain accessible and pre-positioned, ready to move across borders without triggering regulatory flags in intermediary countries. With virtual accounts, any wallet can function as a bank account.

For banks, this model is both simpler and more secure. Their role is limited to facilitating the onramp or offramp through local banking rails like ACH. Once fiat is converted into USDC, the transaction is complete from the bank’s point of view. They’re no longer responsible for custody, fraud risk, or chargebacks, and in many cases, compliance requirements fall by up to 90%.

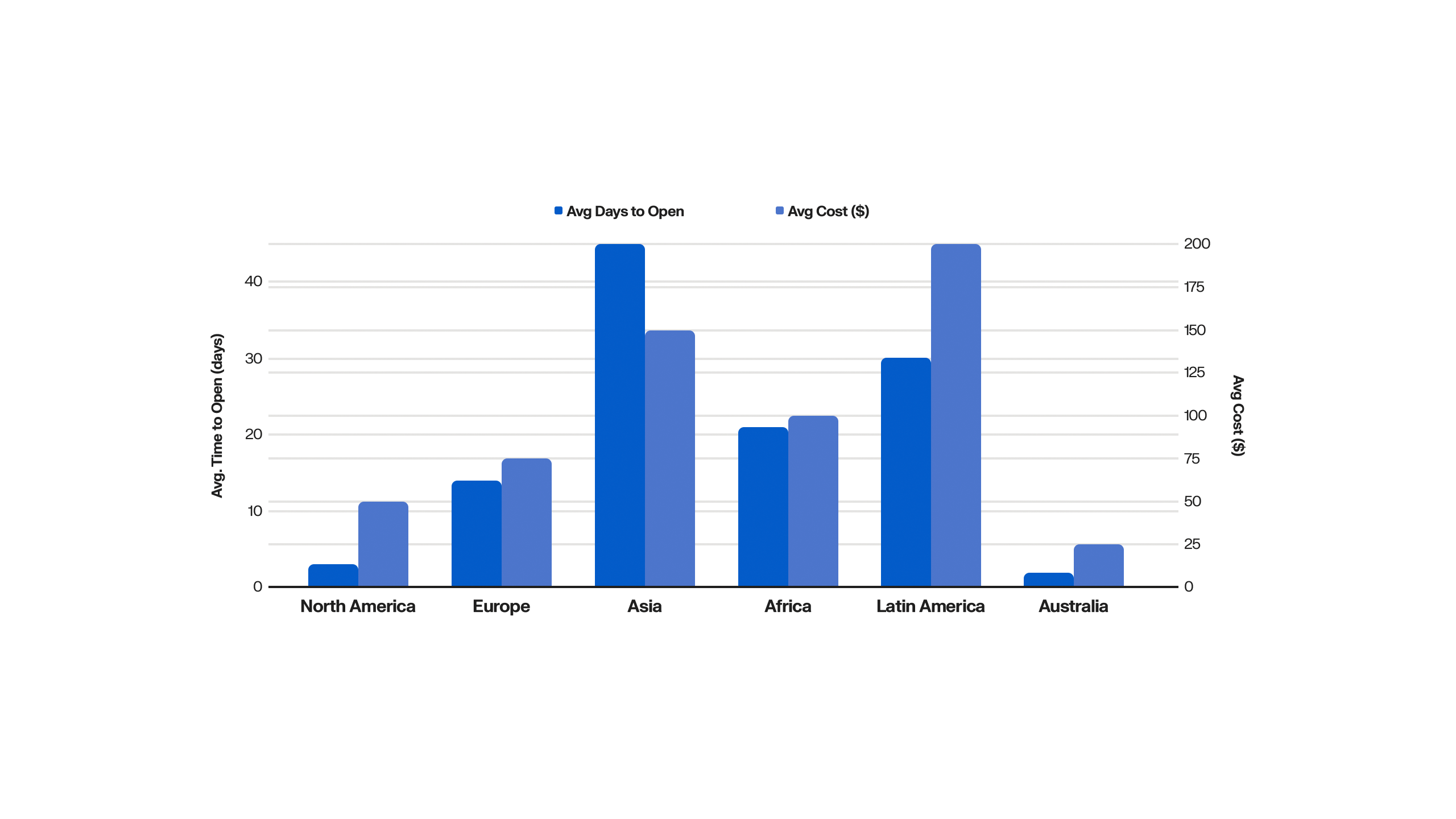

The impact is especially profound for entrepreneurs in emerging markets. Previously, it could take up to six weeks just to obtain an Employer Identification Number and open a business bank account. With stablecoin-linked USD virtual accounts, that process now takes minutes. More importantly, these accounts unlock access to developed markets. For example, U.S. companies like Amazon require merchants to have ACH-enabled, named USD accounts that match their business registration. Virtual accounts make this possible across borders. Geographic restrictions disappear, and every market becomes reachable.

Time and Cost to Open a Business Bank Account

The Stablecoin Payments tech stack

Stablecoin payment platforms are moving beyond the sandwich model and evolving into full-fledged payment networks where users can spend, save, and earn directly within stablecoin-native accounts. These networks have the potential to monetize every layer of the stablecoin stack: issuance (treasury deposits), network activity (transaction fees), capital markets (DeFi yield), and end-user services (consumer applications), all while delivering more value back to users.

“We’re seeing a clear shift: stablecoin payment companies are evolving into full-stack financial networks. Stripe’s recent acquisitions are a signal of that direction. SphereNet is built on that same thesis, a shared ledger tailored to regulated payment firms, offering a new backbone for interoperable, compliant payments infrastructure.” — Arnold Lee, CEO and Co-Founder of Sphere Labs

Companies like Stripe are positioned to own the full stablecoin value stack. Issuers capture the most economic upside, so firms like Bridge have allowed fintechs to introduce their own stablecoins (e.g., USDB), allowing them to capture fees throughout the whole payments process.

This shift helps explain why major fintechs are launching their own stablecoins. Programmable money lets them control the full payment stack, streamline reconciliation and yield, and leverage their existing distribution advantages (e.g. Revolut’s 50 million active users). Stablecoins are entering a new phase of verticalization, where early pioneers face growing competition from institutions that already command scale and market reach.

“The biggest opportunity is in onboarding real users and building distribution channels that work. Crypto has always been great at innovation, but distribution is our Achilles’ heel. That’s where centralized exchanges like Coinbase and Binance are winning.” — Stefan George, Co-Founder of Gnosis Pay

This transformation is already in motion. Across the financial stack, stablecoin players are expanding their capabilities:

- Stablecoin issuers like Circle (with its Circle Payments Network) are expanding beyond issuance to build orchestration networks that facilitate transaction routing and settlement between members.

- Payment orchestrators like BVNK (Layer1) are creating blockchain-enabled systems to connect PSPs, banks, and wallets on a unified network.

- Payments-focused blockchains such as Sphere (Spherenet) are also moving closer to the end-user, embedding themselves deeper in the payment stack.

Stablecoin payments are fast becoming the foundation of a new global payment stack. What began with the simple “stablecoin sandwich” has evolved into full-scale networks, giving users direct access to saving, spending, and earning in dollars without geographic barriers. For banks and fintechs, this shift reduces friction and risk; for entrepreneurs and consumers, it opens access to markets and financial services once out of reach.

Stablecoin payment companies are consolidating legacy payments rails and end-user experience into integrated ecosystems. As distribution scales and institutions embrace programmable money, the competition will no longer be about whether stablecoins work, but about who controls the stack, how value accrues, and what new opportunities are unlocked in a payments system built natively for the internet age.