Stablecoin Payments: The Trillion Dollar Opportunity

What are Remittances with Stablecoins? A guide

Introduction

While stablecoins are reshaping how businesses move money, their impact is equally profound at the person-to-person (P2P) level. These transactions, whether cross-border transfers to family, tuition payments, or emergency support, make up one of the largest and most consistent global payment flows.

In 2024, low- and middle-income countries received roughly $685 billion in remittances, with South Asia, Latin America, and East Asia & Pacific leading the way. Yet despite their scale, traditional remittance channels remain slow and expensive, with fees averaging 4–6% and hidden FX markups adding further cost. Stablecoins offer a fundamentally different path: instant, low-cost, transparent transfers that behave more like sending a text than wiring money through a bank.

“We’re not targeting the U.S. It’s crowded, expensive, and saturated with players. Instead, we’re focused on emerging markets, like Latin America, Southeast Asia, parts of Africa, where crypto has real utility beyond speculation. That’s where Gnosis Pay can make the biggest difference.” — Stefan George, Co-Founder of Gnosis Pay

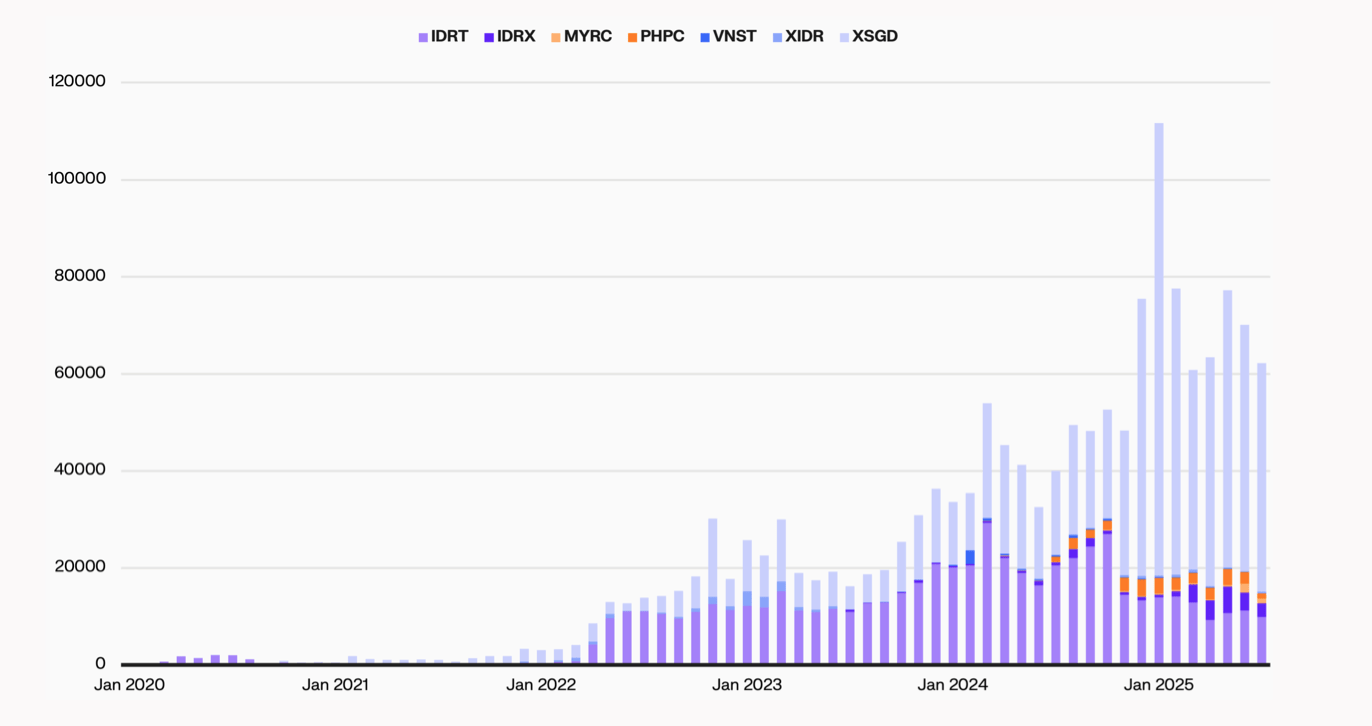

While remittance inflows measure in the hundreds of billions annually, stablecoin activity in these corridors is still in early stages, but rising fast. The dashboard below tracks monthly transaction counts across key Southeast Asian stablecoins such as XSGD (Singapore), XIDR (Indonesia), and VNST (Vietnam), spanning multiple chains.

Despite transaction volumes remaining orders of magnitude below traditional remittance flows, the steady month-over-month growth from 2,920 transactions in January 2022 to ~70,000 transactions in June 2025 points to increasing adoption.

“In the past, moving from USD to a long-tail currency involved multiple intermediaries and days of delay. Now, you can swap FDUSD to PHP or IDR instantly with better transparency and lower cost. That unlocks massive efficiency for payment companies.” — Devere Bryan, General Manager of First Digital

SE Asia Stablecoin Transactions Have Surged 24x Since 2022

Source: Mou_raf, Keyrock

Because remittance costs remain high, local stablecoins are likely to see continued growth, not just as a workaround for expensive remittance rails, but as a practical tool for spending in local currency. While many users may prefer to receive funds in U.S. dollars, day-to-day expenses still happen in pesos or rupiah. Stablecoins denominated in local currency bridge that gap. As stablecoin rails continue to get built out, with better liquidity, integrations, and off-ramp access, local stablecoins are expected to accelerate.

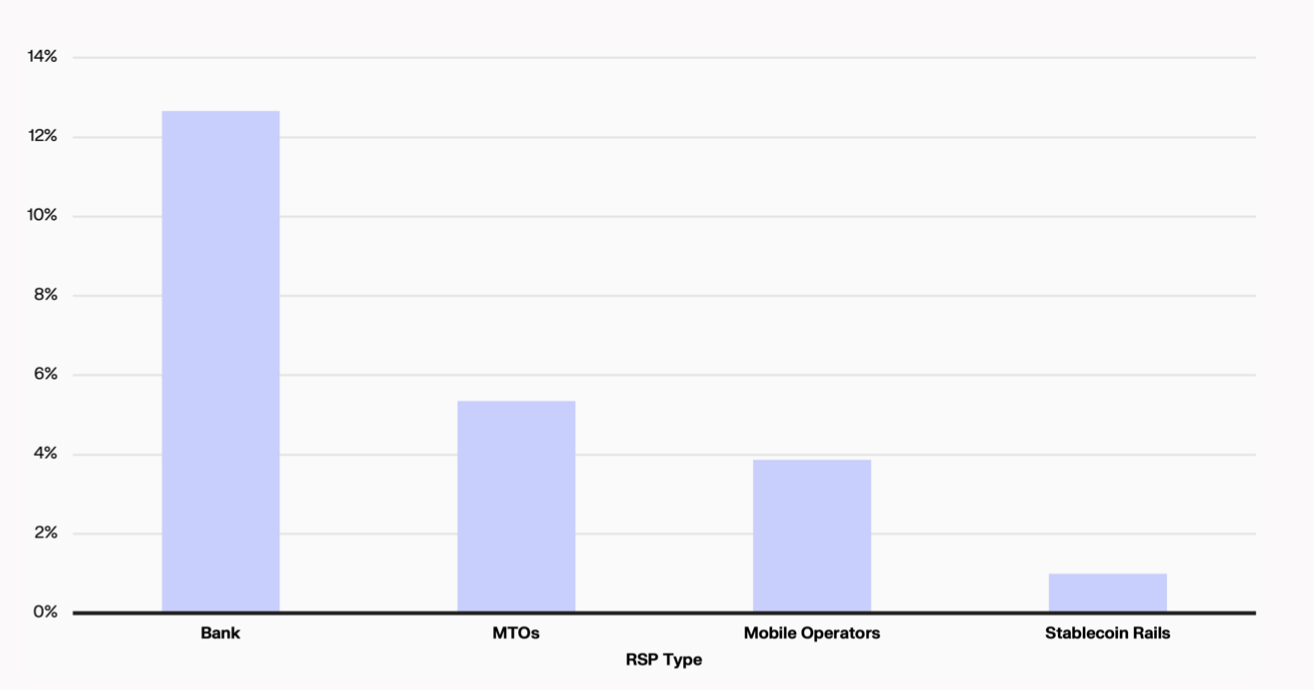

On average, sending $200 costs roughly 6.3% and $500 costs 4.3%. These fees include service charges (by banks, Western Union, etc.) plus currency exchange markups. In practice, providers often offer worse than market exchange rates and keep the difference as profit. Across corridors, FX markups typically account for ~35% of the cost, and in some emerging markets they can be as high as 80%.

The breakdown of remittance fees by provider” underscores the inefficiency of traditional channels. For a $200 transfer, banks charge the highest fees (~12.66%), while money-transfer operators (MTOs) charge ~5.35% and mobile carriers ~3.87%. By contrast, stablecoin platforms can dramatically undercut these rates. For example, the Coinbase Developer Platform USDC on-ramp/off-ramp charges 0%, whereas other gateways (e.g. MoonPay) may charge up to ~4.5%. With growing competition, these fees are trending downward.

Stablecoins Can Reduce Remittance Costs by ~92%

Source: World Bank

BCRemit (serving Filipino migrant workers) slashed its total transfer cost (fees + FX) to just over 1%, while avoiding the liquidity shortfalls that force traditional providers to use costly short-term loans.

Similarly, Sling Money lets users fund “virtual accounts” and send money at real-time mid-market FX with no hidden markups, charging only up to 0.1% on deposits while banks charge ~13% to send a $200 transfer. Funds on Sling are converted to the USDP stablecoin and can then be sent globally in under a second for free.

“We can instantly send photos or a text message anywhere in the world at almost no cost, and money should work the same way,” said Mike Hudack, CEO and Co-Founder of Sling Money.

Speed of Sending Remittances

Source: World Bank

Stablecoin rails represent an order-of-magnitude improvement in remittance economics, being 4-13x cheaper while providing near-instantaneous settlement compared to traditional methods that could take one to multiple days. This efficiency is already prompting incumbent players to adapt as legacy remittance firms like M-Pesa added regulated stablecoins (e.g. USDC) to their product suites.

“At Bitso, we’ve built our payment rails around emerging markets. We created MXNB, a peso-pegged stablecoin, and helped launch BRL1 in Brazil. In 2024 alone, Bitso Business processed over $12b in cross-border payments. These products give our clients efficient access to local currencies, enabling global companies to serve LATAM markets with lower fees and faster settlement.” — Imran Ahmad, General Manager at Bitso Business

Bitso Commands LATAM CEX Volumes

Source: Dune, Keyrock

Bitso, which handles over 10% of remittance flows between the U.S. and Mexico (the world’s largest corridor), now dominates LATAM crypto exchange volumes. Bitso processed nearly $850m in July, around 6.5× more than its closest rival. In a region where stablecoins made up ~39% of all crypto purchases in 2024, Bitso’s early bet on stablecoin-native infrastructure is paying off.

As the payments landscape evolves, centralized exchanges and crypto-native remittance providers are increasingly expanding into payments by launching payments apps (e.g. Kraken’s Krak) and local stablecoins (e.g. Bitso’s MXNB & BRL1). These stablecoins serve as the destination, not just the medium in the stablecoin sandwich model, allowing users to stay onchain without needing to withdraw to bank accounts.

Looking ahead, we expect more exchanges and remittance platforms to issue regional stablecoins and leverage their internal liquidity for swaps. In general, these players are shifting focus toward improving payments while keeping users onchain by offering yield on balances and branching into adjacent services like credit/debit cards (e.g. Coinbase’s “One” card).

“The stablecoin market today is almost entirely denominated in USD, but that won’t last. As tokenized payment use cases expand, we’ll see growing demand for domestic currency stablecoins. The future of tokenization is multipolar.” — Harvey Li, Tokenization Insight Founder

Stablecoins are reshaping remittances by making transfers faster, cheaper, and more transparent, cutting fees by up to 90% while enabling real-time settlement. With regional stablecoins gaining traction and incumbents adapting, P2P payments are set to become one of the strongest drivers of mainstream stablecoin adoption