Stablecoin Payments: The Trillion Dollar Opportunity

What are B2B stablecoin payments? A guide

Introduction

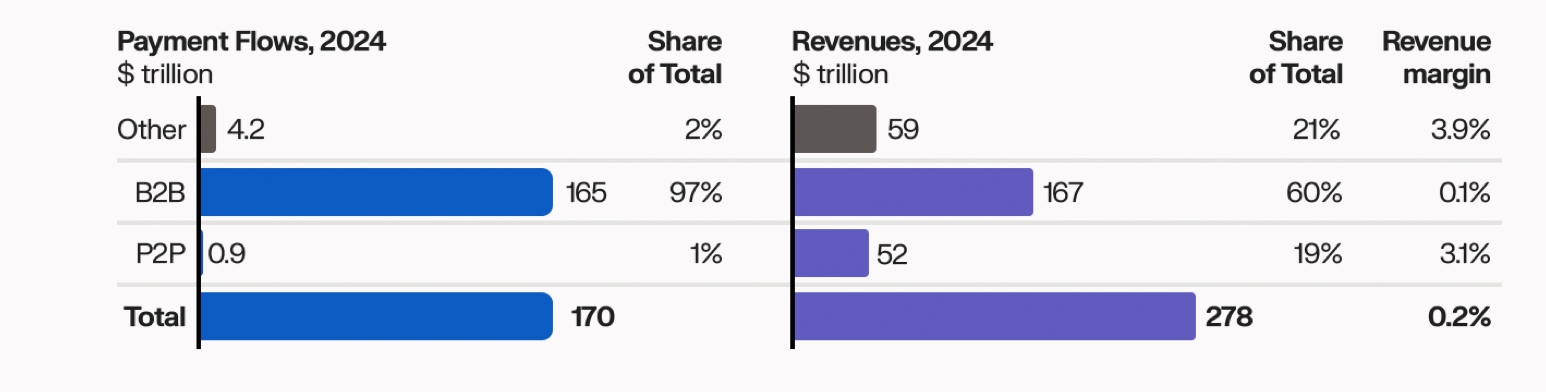

Source: McKinsey

B2B payments, transactions between companies and their suppliers, vendors, or service providers, form the backbone of global commerce. By 2027, the average mid-sized company is expected to make over 1,400 domestic payments annually, underscoring just how heavy the operational load can be.

Stablecoins offer a new way to move money. Pegged to fiat currencies like the U.S. dollar but running on blockchain rails, they combine the familiarity of traditional money with the speed, transparency, and programmability of digital assets. Though adoption in B2B contexts is still early, stablecoin payments already account for roughly $36 billion annually, just ~0.02% of global payments, yet nearly half of all stablecoin transaction volume today.

For businesses, the impact is beginning to show up in the back office. Treasury teams are using stablecoins to simplify cash management, unlock yield opportunities, and free themselves from fragmented balances. Supplier settlement is also shifting, as companies experiment with faster, lower-cost, cross-border payments. This guide explores how stablecoins are starting to transform these two critical categories of B2B finance.

“When we launched Bitso in 2014, crypto was still experimental. Bitcoin traded below $1,000, Ethereum didn’t exist yet, and few believed in the space. Fast forward to today, Bitso is Latin America’s leading crypto-powered financial platform. Our B2B arm, Bitso Business, has become a trusted payments infrastructure partner for over 1,900 institutions. With more than a decade of LATAM expertise, we help businesses send, receive, and convert local currencies through blockchain rails, faster, cheaper, and with full regulatory coverage” — Daniel Vogel, CEO and Co-Founder of Bitso

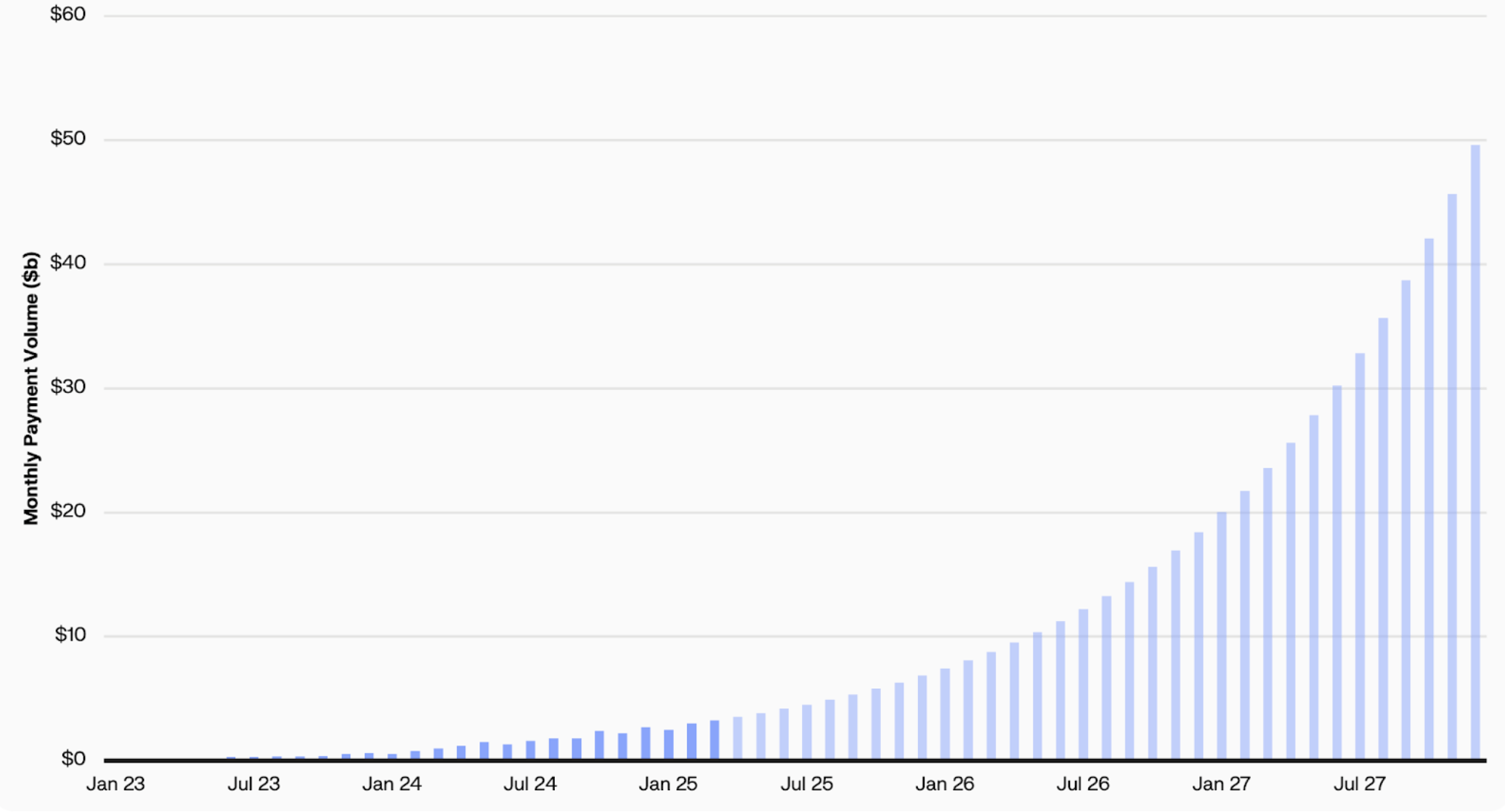

Stablecoin B2B Volumes Set to Surge 17x to $50b

Source: Artemis, Keyrock

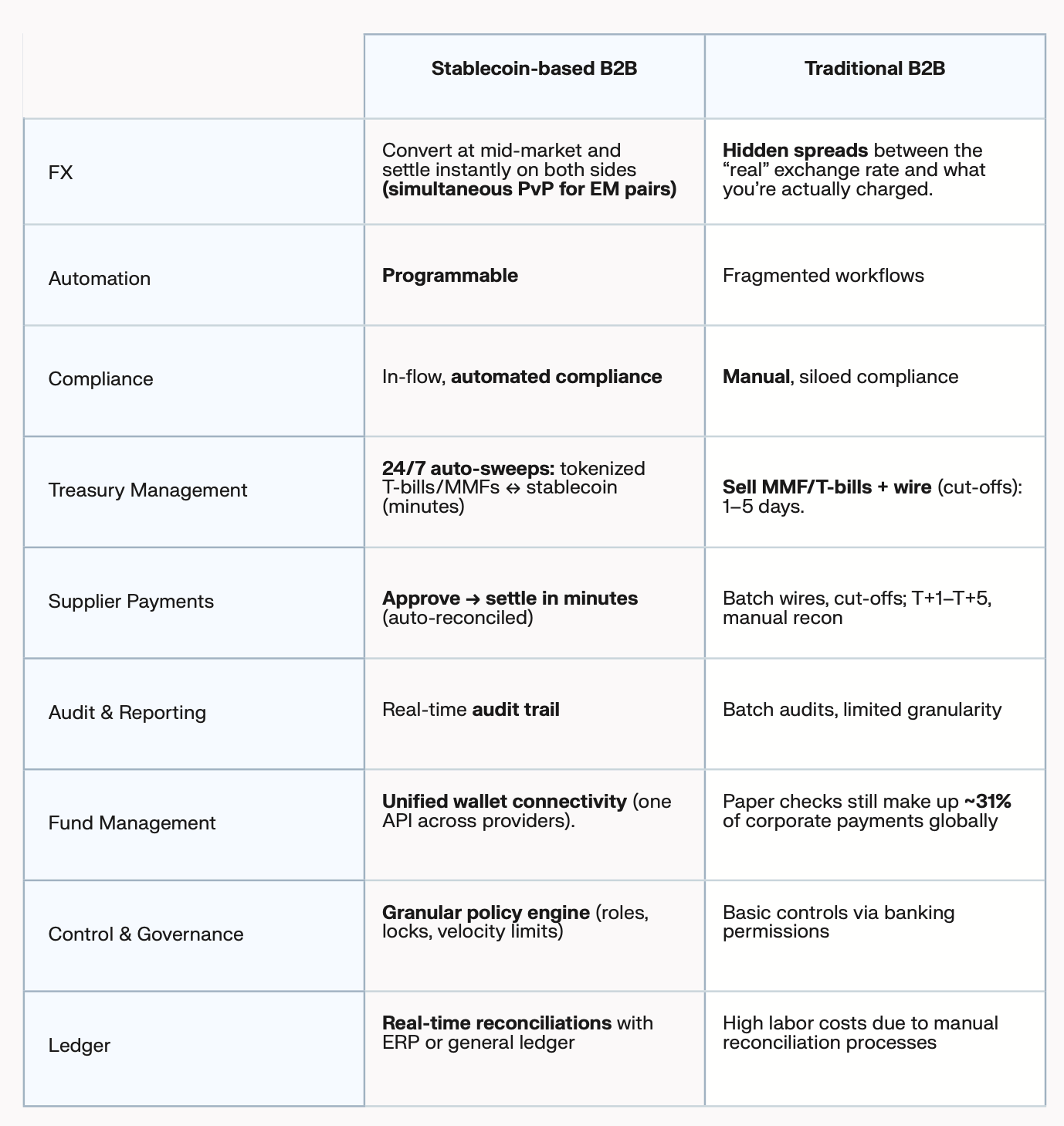

Despite decades of optimization, B2B payments remain expensive. Companies still face $14 to $150 in fees by intermediary banks and FX conversions per $1,000 transferred, while allocating around 32 cents for every $1,000 of revenue to treasury functions. These costs represent just one component of broader treasury expenses.

These costs persist in part because most payment operations (98% of them) are still manual. Paper checks still make up 31% of payments, taking up to three weeks to clear and costing $13–$40 per transaction.

“From the B2B side, the appetite for stablecoin payments is strong. What’s holding them back isn’t the tech, it’s the lack of regulatory clarity. Businesses need a clear framework that tells them what’s compliant and what’s not. Add to that the need for bulletproof security, something that gives enterprises the confidence to transition from legacy systems to blockchain-backed solutions.” — Caio Barbosa, Founder of Lumx

Meanwhile, stablecoins automate core treasury functions (escrow, conditional transfers, and invoice settlement) and enable wallet orchestration with real-time ERP syncs, slashing labor and reconciliation costs. Compliance tools (OFAC, KYB/KYT, travel rule) can be embedded directly into payment flows, while governance is enforced via smart contracts with programmable roles, locks, and velocity limits.

Real-Time Business Treasury Management

Corporate treasury is one of the clearest areas where stablecoins offer an immediate advantage.

Multinational firms often juggle fragmented balances across dozens of accounts, currencies, and legal entities, restricting yield opportunities and tying up working capital. Many also face cash pooling burdens and the risk of holding illiquid emerging-market currencies.

Meanwhile, fintechs and SMEs collectively pool billions in customer deposits yet pass on none of the yield. As shown below, 21% of U.S. commercial deposits ($3.85 trillion) earn no interest at all, giving banks a free spread on capital they don’t compensate for. At a 4% savings rate, that’s $154 billion in potential yield going to banks. This legacy model disproportionately benefits financial institutions, not the businesses fueling them.

Yield on Idle Treasury Cash

The stablecoin model flips this. Businesses can hold reserves in yield-bearing stablecoins (e.g., tokenized T-bills or money market funds), collect that yield automatically, and use those same tokens for disbursements, payroll, or supplier settlement. No batch cycles, no cutoff windows. Over time, we believe these balances will shift into stablecoins to capture yield until traditional finance institutions offer yield on stablecoin balances. Over $600m has already been distributed directly through yield-bearing stablecoins.

“Stablecoins give users in emerging markets access to U.S. dollars. USDY takes that one step further, it gives them access to U.S. dollar savings. USDY is backed by U.S. Treasuries and pays yield, but It can also be used as collateral. This allows USDY to be utilized while it steadily accrues yield .” – Ian De Bode, Chief Strategy Officer of Ondo

Even large corporations are taking note. At its investor day, Sony revealed plans to issue an internal stablecoin to facilitate intragroup payments, while capturing yield on idle treasury balances. The logic is simple: if email works globally in real time, why shouldn’t money?

“Stablecoins are reshaping treasury for fintechs. Instead of pre-funding local accounts, firms can use just-in-time liquidity and deploy capital globally within minutes. Operations run 24/7, no more batch processing or weekend delays. Treasury visibility moves from lagging reports to real-time data. CFOs can track every dollar across their global operations instantly, impossible with traditional banking infrastructure.” — Chris Harmse, Co-Founder and CBO of BVNK

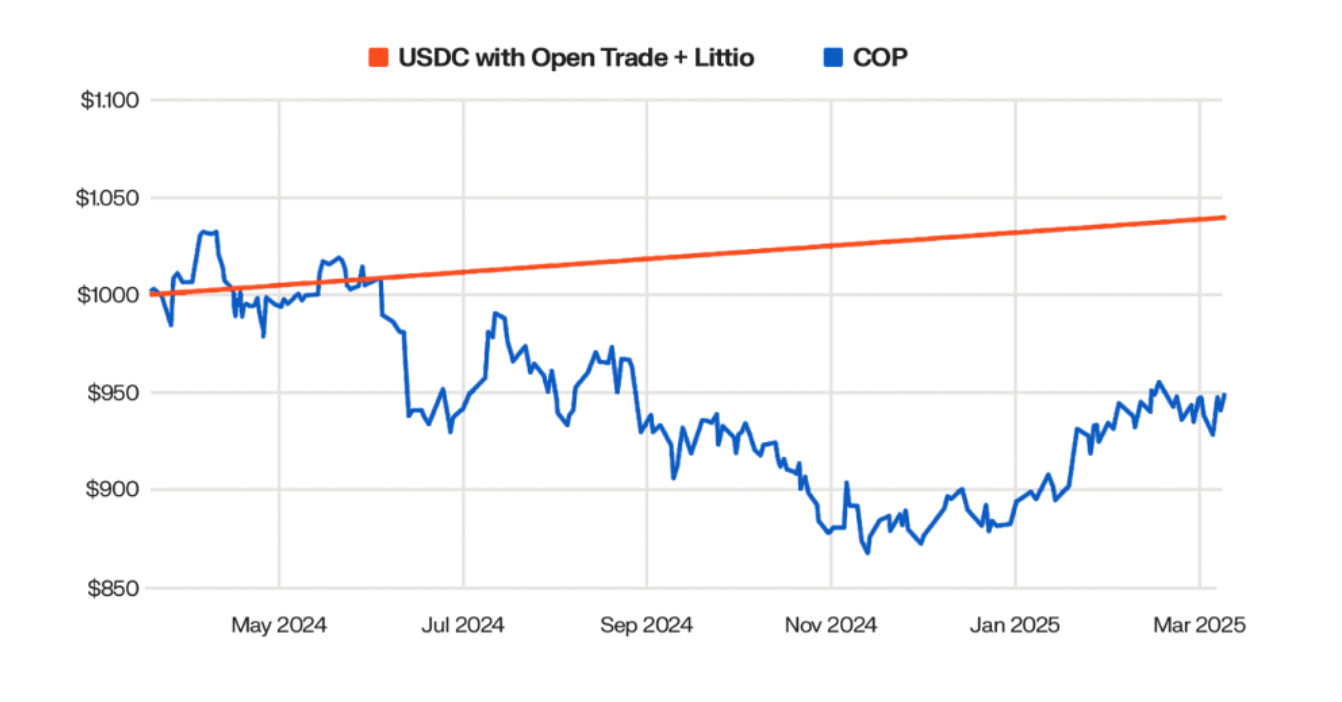

This benefit is already playing out in volatile FX environments. In Colombia, where the peso dropped below $900 per $1 during recent currency swings, OpenYield’s platform enabled users to hold USDC and earn yield on real-world assets, generating up to 6% APR, compared to just 0.4% returns on dollar accounts from local banks. The chart below illustrates how $1,000 in pesos lost significant value while $1,000 in USDC held on Open Yield + Littio would have preserved purchasing power and accrued yield.

Source: Conduit

Supplier Settlement with Stablecoins

Beyond treasury optimisation, stablecoin rails are unlocking real gains in supplier settlement, particularly for import/export businesses, logistics firms, and SMEs that routinely deal with foreign partners. These firms are often exposed to FX volatility, bank fees, and settlement delays.

“Think of how dropshipping transformed inventory management. Stablecoins like USDC and EURC are doing the same for treasury. Fintechs can centralise capital and push out stablecoins for last-mile payouts just in time, instead of locking up funds in local accounts around the world. The result is significantly improved capital efficiency.” — Circle

Stablecoins simplify this to a direct peer-to-peer settlement format:

- Payers send USDC (or any stablecoin)

- Receivers cash out locally via exchanges, on/off-ramp APIs, or banking partners.

- There’s no need for the payer to maintain a local account in the supplier’s country, nor to prefund a nostro account in advance.

Conduit exemplifies the B2B infrastructure development by connecting domestic payment rails to a unified onchain payments layer. The platform processes payments across stablecoins and local currencies with reported costs up to 22% lower than traditional alternatives. Brazilian businesses settling payments in Euros achieve settlement times over 500x faster, saving thousands of hours of transaction settlement time annually.

“At Conduit, we see stablecoins as driving a generational change in cross-border payments that could displace SWIFT. We’re already seeing it work at scale. With our partner Braza in Brazil, we enable Brazilian Real to be minted into a stablecoin, swapped in real time for USD or EUR-backed stablecoins, and settled within minutes, replacing what used to take days.” — Kirill Gertman, CEO and Founder of Conduit

For finance teams managing cross-border operations, the value proposition is clear: instant settlement, transparent pricing, and programmable money at a fraction of traditional costs. The question for businesses is no longer whether to integrate stablecoin rails, but how quickly they can implement them to maintain competitive advantage in an increasingly digital-first global economy.