Tokenization

Tokenized Commodities: 147% Monthly AUM Turnover and DeFi Collateral Use

Tokenised commodities move more than their entire market cap every month. No other tokenised asset class comes close. The reason is DeFi.

The turnover anomaly

Most tokenised assets behave like buy-and-hold instruments. Investors acquire them for yield, exposure, or diversification. They sit in wallets. They settle slowly into portfolios.

Commodities do something different.

Tokenised commodities turn over 147% of their AUM each month. That means the entire market cap cycles through transactions roughly 1.5 times every 30 days. This is not speculative flipping. It is structural activity driven by a specific use case: DeFi collateral.

How the collateral engine works

This cycle creates velocity. The same tokenised commodity moves through multiple transactions: deposit, borrow, repay, withdraw, redeposit. Each movement counts toward turnover. The 147% figure reflects a market where the primary use case is not holding. It is leveraging.

The collateral use case is self-reinforcing. As more DeFi protocols accept tokenised commodities, more holders deposit them. More deposits deepen the lending pools. Deeper pools attract more borrowers. The flywheel builds.

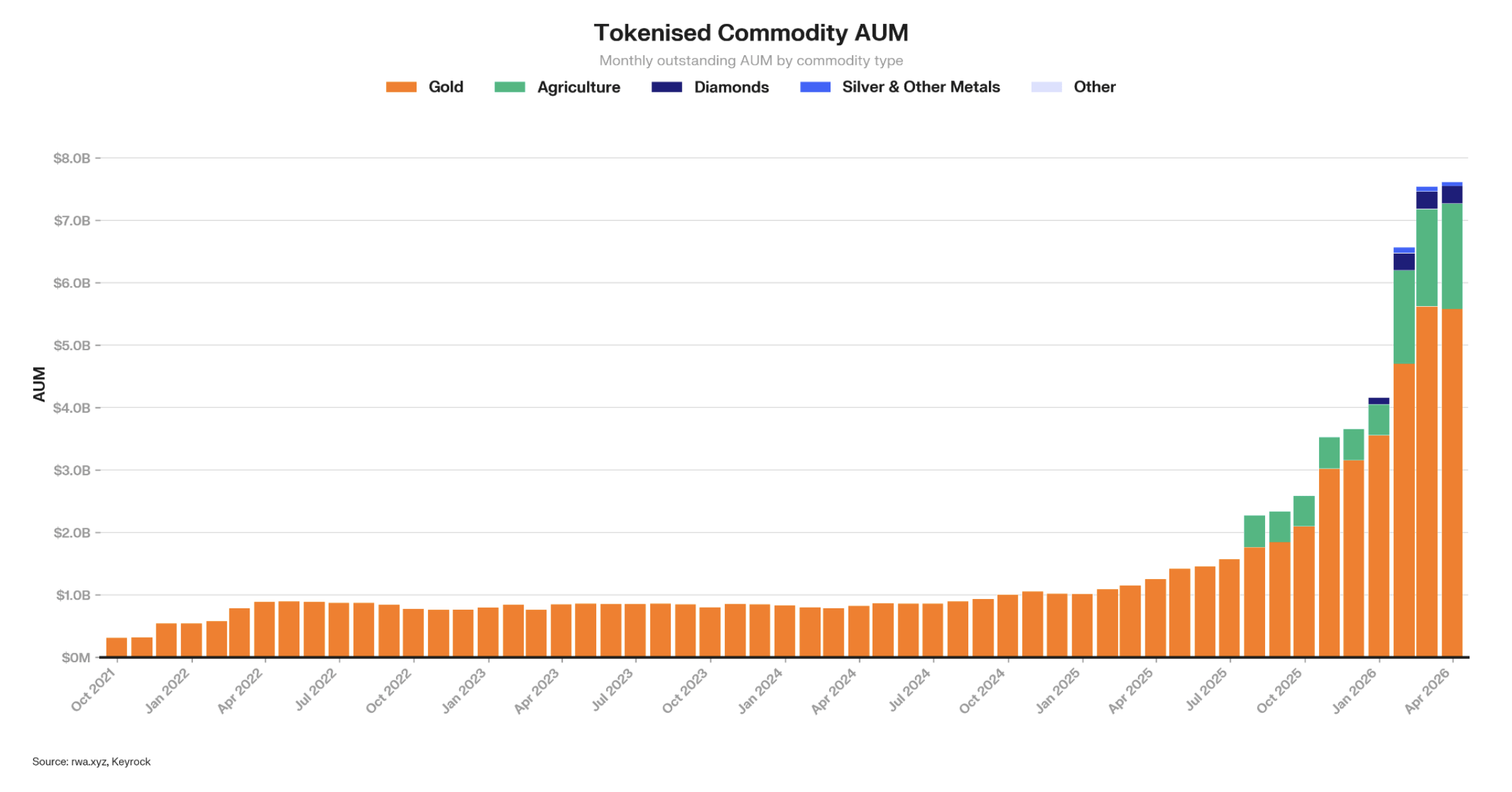

Gold leads for obvious reasons

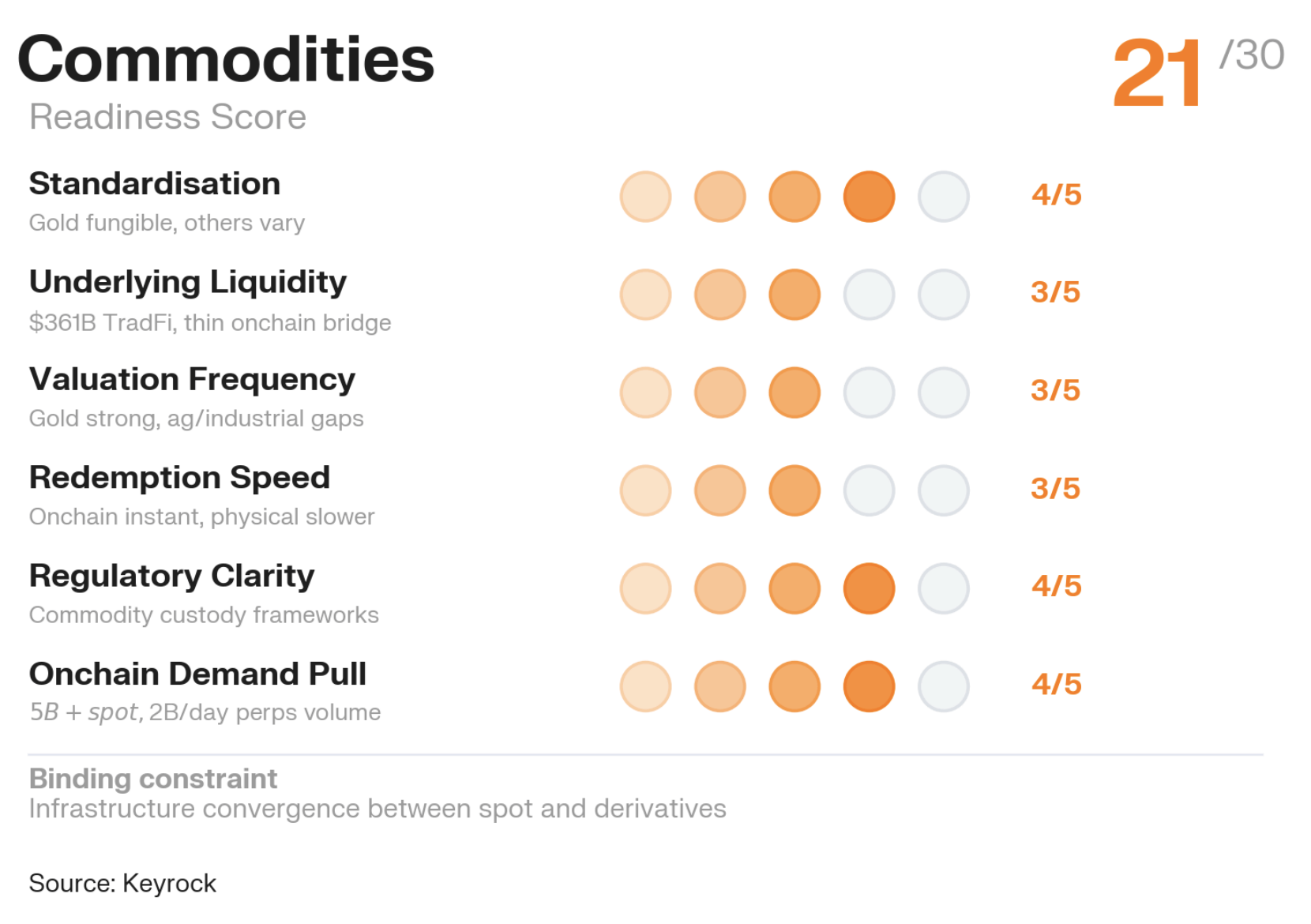

The readiness score in context

Our RWA readiness framework scores commodities at 21 out of 30. Third among the five asset classes we evaluated, behind treasuries (27) and equities (22).

Commodities score highly on underlying liquidity and onchain demand pull. The 147% turnover rate is the most emphatic demand signal of any tokenised asset class. The underlying commodity markets are among the deepest in the world.

Where commodities lose points is redemption mechanics and regulatory clarity. Converting a tokenised gold position back to physical gold involves logistical complexity that treasuries do not face. Regulatory frameworks for commodity tokens vary significantly across jurisdictions.

Despite these constraints, the raw demand pull is extraordinary. When an asset class turns over 147% of AUM monthly, the market is telling you something about product-market fit.

Beyond gold: the expanding commodity universe

Gold established the model. The next wave expands to silver, oil, and agricultural commodities. Each brings different dynamics. Silver adds industrial demand alongside monetary demand. Oil introduces energy market exposure. Agricultural commodities connect food supply chains to onchain finance.

The challenge for each new commodity is the same: build a tokenised instrument with reliable NAV pricing, efficient redemption, and integration into DeFi protocols. Gold proved it works. Expanding the universe is an engineering problem, not a conceptual one.

As the commodity universe expands, so does its utility as a diversified collateral base. A DeFi protocol that accepts gold, silver, and oil as collateral offers borrowers more flexibility and the protocol itself benefits from asset diversification.

The derivatives amplifier

RWA perpetuals grew 40x in six months to $67 billion monthly volume. Commodities are a significant component of that growth. Commodity perpetuals allow traders to gain leveraged exposure to gold, silver, and oil prices without holding the underlying tokenised asset.

The spot-to-derivatives relationship in commodities is particularly strong. Active spot markets with high turnover generate the price data and trading patterns that derivatives markets need. The 147% monthly turnover creates a rich data environment for derivative pricing.

Arbitrage between tokenised commodity spot prices and perpetual contract prices tightens spreads in both markets. As more commodities tokenise, the derivatives layer expands proportionally. Each new spot instrument generates a derivative opportunity.

The onchain asset management implications

For portfolio managers building onchain strategies, tokenised commodities serve a dual function. They provide commodity exposure for diversification. They simultaneously generate yield through collateral deployment. Holding tokenised gold is not idle. The gold works.

This dual function changes how allocators think about commodity positions. In traditional finance, a gold allocation is a defensive hedge. It does not generate income. Onchain, the same gold position can be collateralised to fund yield strategies while maintaining the hedge.

The $400 trillion global market includes roughly $15 trillion in commodity assets. Even a small fraction moving onchain creates a massive collateral pool for DeFi. The 147% turnover rate shows the demand already exists. The constraint is supply.

What comes next

Tokenised commodities have found product-market fit in a way that few other tokenised asset classes have matched. The collateral use case is proven. The turnover data is definitive. The infrastructure works.

The next phase is about scale. More commodity types onchain. Deeper integration with DeFi lending protocols. Better redemption mechanics that narrow the gap between tokenised and physical settlement. Regulatory frameworks that provide clarity for institutional participation.

147% monthly turnover is the market’s verdict. Tokenised commodities are not a theoretical use case. They are an active, thriving market that powers a significant portion of DeFi infrastructure.

Frequently asked questions

Why do tokenised commodities have such high turnover?

They turn over 147% of AUM monthly, driven by use as collateral in DeFi protocols. Unlike buy-and-hold assets, tokenised commodities circulate actively through lending, borrowing, and collateralisation cycles.

How are tokenised commodities used as DeFi collateral?

Holders deposit tokenised commodities like gold into lending protocols to borrow stablecoins or other assets. This allows them to maintain commodity exposure while accessing liquidity. The collateral cycle drives the high turnover rate.

What is the readiness score for tokenised commodities?

21 out of 30 on Keyrock’s RWA readiness framework. Strong on underlying liquidity and onchain demand pull. Weaker on redemption mechanics and regulatory clarity compared to treasuries at 27 out of 30.

Which commodities are most commonly tokenised?

Gold dominates, with products like PAXG and XAUT representing the majority of onchain commodity value. Gold’s deep underlying market and store-of-value characteristics make it the natural first commodity to tokenise at scale.