Tokenization

Tokenized Asset Liquidity: The Secondary Market Gap and How to Close It

You can tokenise anything. But without liquidity, a token is just a receipt you cannot sell.

The problem nobody wants to talk about

The tokenisation industry has an issuance obsession. New asset classes onchain every month. New protocols. New partnerships between traditional finance and blockchain platforms. The supply side is accelerating.

The demand side has a different story. Most tokenised assets trade in thin markets with wide spreads and limited depth. An investor who buys a tokenised bond can face a 2-5% discount when selling. For institutional allocators managing billions, that is an unacceptable cost.

This is the secondary market liquidity gap. It is the single largest constraint on the growth of the tokenised assets market.

Why traditional market making falls short

In traditional markets, market makers provide liquidity by continuously quoting bid and ask prices. They manage inventory risk, earn the spread, and keep markets functioning. The model works because traditional instruments have standardised settlement, deep reference markets, and well-understood risk profiles.

Tokenised assets break several of those assumptions. Settlement happens on blockchains with varying finality guarantees. Reference pricing may be asynchronous with the onchain market. Redemption mechanics differ by issuer. Regulatory status varies by jurisdiction.

A market maker quoting a tokenised treasury product needs to price sovereign credit risk, blockchain settlement risk, issuer-specific redemption terms, and cross-venue fragmentation. That is a fundamentally different challenge than quoting a government bond on a centralised exchange.

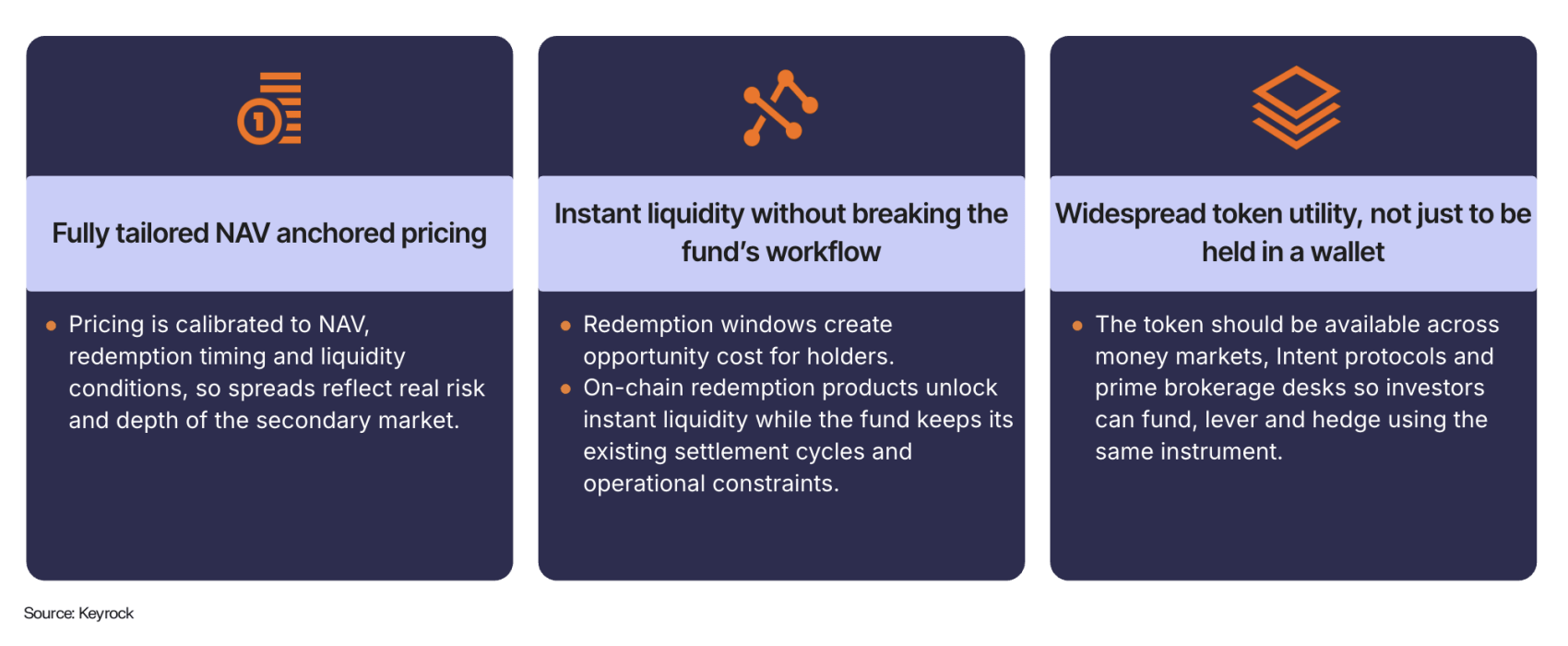

The NAV-anchored approach

Keyrock is building liquidity infrastructure that anchors token prices to verifiable net asset value. The concept is straightforward. The underlying asset has a known value. The token should trade as close to that value as possible. Any persistent gap represents friction that can be engineered away.

NAV-anchored pricing pulls market making away from pure order-book dynamics and toward fundamental value. When a tokenised treasury trades at 99.5% of its NAV, the pricing engine narrows the bid. When it trades at 100.3%, it narrows the ask. The result is a market that gravitates toward fair value by design.

This approach works because the underlying assets have known, verifiable values. Treasuries reprice continuously. Equities have reference markets. Commodities have deep benchmark pricing. The NAV anchor converts that information into tighter onchain spreads.

Instant-redemption vault infrastructure

Price anchoring alone is not sufficient. Investors need a guaranteed exit path. If the secondary market thins out, they need the option to redeem the underlying asset without waiting for a counterparty.

Instant-redemption vaults provide that guarantee. They hold reserves of the underlying asset and stand ready to accept token redemptions at or near NAV. The vault acts as a backstop buyer. Not the primary source of liquidity, but the guarantee that liquidity always exists.

This changes the risk calculus for allocators. The question shifts from “can I sell this token?” to “at what premium or discount to NAV will I sell?” When the worst case is redemption at a small haircut rather than an illiquid position, institutional comfort rises dramatically.

The concentration problem and its liquidity implications

In four of five tokenised asset classes, over 89% of value sits with the top 5% of wallets. High concentration creates liquidity risk. When a small number of holders control most of the supply, any single exit can move the market significantly.

This is the paradox of early institutional adoption. The same large allocators who validate the asset class also create fragile markets through their outsized positions. The solution is to expand the holder base. Broader distribution reduces the impact of any single seller.

Equities and alternative funds show early signs of progress. Average trade sizes of $566 and $2,100 respectively indicate retail participation. As these segments grow, the holder base diversifies and secondary market resilience improves. The great tokenisation shift depends on this broadening.

What the derivatives layer reveals

RWA perpetuals grew 40x in six months to $67 billion monthly volume. That growth happened partly because the derivatives market does not face the same liquidity constraints as spot markets. Perpetuals are synthetic. They do not require custody or settlement of the underlying.

But derivatives and spot markets are connected. Healthy derivatives markets create price discovery that informs spot liquidity provision. Arbitrage between perp prices and spot NAV tightens spreads in both venues. The derivatives boom is building infrastructure that the spot market will benefit from.

10% of all onchain derivatives volume is now tied to RWAs. That flow generates data, builds familiarity, and trains a generation of market participants to think about real-world assets onchain.

The 2027 liquidity inflection

We identify 2027 as the year when regulation, market depth, liquidity infrastructure, and distribution mature together. This convergence is particularly significant for secondary markets.

Regulatory clarity brings institutional capital off the sidelines. More participants mean deeper order books. Deeper order books mean tighter spreads. Tighter spreads attract more participants. The positive feedback loop activates once a critical mass of conditions align.

We are building for that moment. NAV-anchored pricing and instant-redemption vaults are not point solutions. They are infrastructure designed to scale with the market as it grows from $27 billion to $400 billion and beyond.

Frequently asked questions

What is the liquidity gap in tokenised assets?

The disconnect between primary issuance and the lack of deep, reliable secondary markets. Most tokenised assets have thin order books, wide spreads, and limited price discovery, making it difficult for investors to exit at fair value.

How is Keyrock solving the tokenised asset liquidity problem?

Through NAV-anchored pricing that ties token prices to verifiable net asset value, and instant-redemption vault infrastructure that provides guaranteed exit liquidity. Together, these systems reduce spreads and ensure continuous market access.

Why is secondary market liquidity critical for tokenised asset growth?

Institutional allocators will not commit meaningful capital to assets they cannot sell at fair value. Secondary market liquidity is the prerequisite for the market to grow from $27 billion toward its projected $400 billion by 2030.