The $400T Future of Tokenized Assets

Tokenization Regulation 2027: The Year Everything Converges

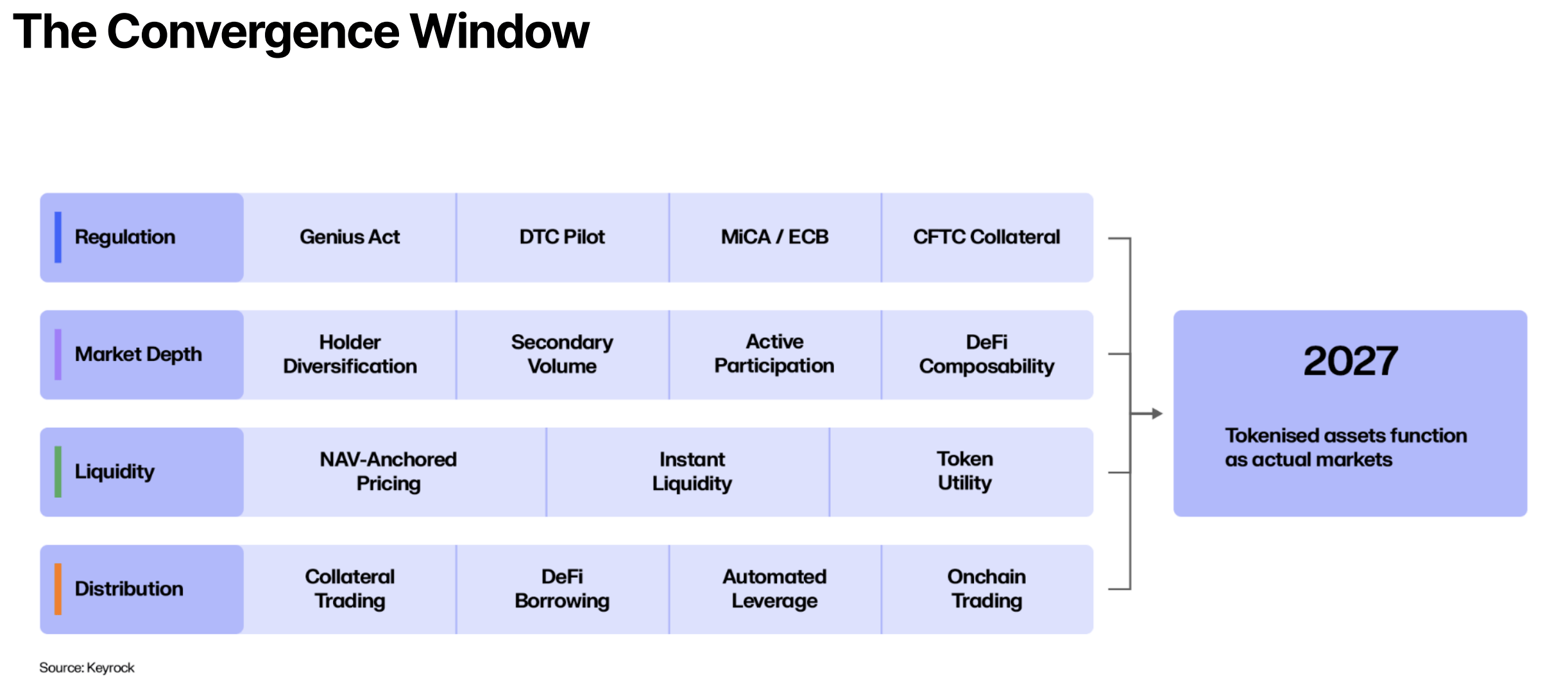

Four forces align in 2027 for the first time: regulation, market depth, liquidity infrastructure, and distribution. This is the year the market shifts from pilots to production.

Why timing matters

Tokenisation does not scale when one condition is met. It scales when multiple conditions converge. You can build the infrastructure, but without regulatory clarity, institutions stay on the sidelines. You can pass the regulation, but without liquidity infrastructure, the market stays thin.

We have analysed the maturity curves across four dimensions: regulatory frameworks, market depth, liquidity infrastructure, and distribution networks. The data points to 2027 as the first year all four reach a critical threshold simultaneously.

This is not a prediction based on optimism. It is based on observable legislative timelines, infrastructure deployment schedules, and institutional pipeline data.

The EU: first mover with MiCA

The European Union established the clearest framework through MiCA. Markets in Crypto-Assets Regulation provides a comprehensive rulebook for digital asset issuance, custody, and trading. It is not perfect. But it is operational.

For tokenised assets specifically, MiCA creates a pathway for compliant issuance that institutional allocators can work within. European asset managers no longer face the question of whether tokenisation is legal. They face the more productive question of how to execute within the framework.

The EU’s head start matters. By 2027, European markets will have two years of operational experience under MiCA. That head start builds case law, operational best practices, and institutional confidence that other jurisdictions can reference.

The UK: sandbox to scale

This approach offers flexibility. Regulators learn from real deployments before codifying permanent rules. The risk is speed. Sandboxes work for experimentation. They do not scale for market-wide adoption.

The transition from sandbox to permanent framework is expected to accelerate through 2026 and into 2027. The UK has signalled intent to maintain competitiveness with the EU while preserving regulatory flexibility. For asset managers, the trajectory is toward clarity.

The US: from enforcement to legislation

The United States has undergone the most significant shift. For years, the regulatory approach was enforcement-led. Agencies used existing securities law to govern digital assets, creating uncertainty through litigation rather than clarity through legislation.

That dynamic is changing. Legislative proposals now address tokenised securities directly. The shift from “is it a security?” to “how should tokenised securities be regulated?” represents a fundamental maturation of the policy conversation.

The US timeline is the most variable. Legislative cycles are unpredictable. But the direction is unmistakable. By 2027, the legislative framework should provide sufficient clarity for major institutions to deploy capital at scale. The $400 trillion global opportunity cannot materialise without US participation.

APAC: targeted precision

These jurisdictions compete for the same pool of institutional capital. Their regulatory precision reflects this competition. Rather than broad frameworks, they offer specific rules for specific use cases. Tokenised funds in Hong Kong. Tokenised bonds in Singapore.

Japan and South Korea are moving on parallel tracks, with particular focus on stablecoin payment frameworks that intersect with tokenised asset settlement. APAC’s fragmented approach creates complexity but also creates optionality for issuers.

The convergence thesis

No single jurisdiction drives the market alone. Tokenised assets are inherently cross-border. A tokenised treasury issued in the US needs to be tradeable by an investor in Singapore, held by a custodian in Europe, and settled on a blockchain that spans all three.

2027 is the year the regulatory patchwork becomes a functional mosaic. Not harmonised. Not identical. But interoperable enough for institutional capital to flow across borders with manageable compliance costs.

The convergence is not just regulatory. Market depth builds as more assets are issued. Liquidity infrastructure matures through NAV-anchored pricing and instant-redemption mechanisms. Distribution networks expand as platforms integrate tokenised products.

When all four forces align, the transition from pilot to production happens faster than most expect. We have seen this pattern in other technology adoption cycles. The slow build. Then the rapid shift.

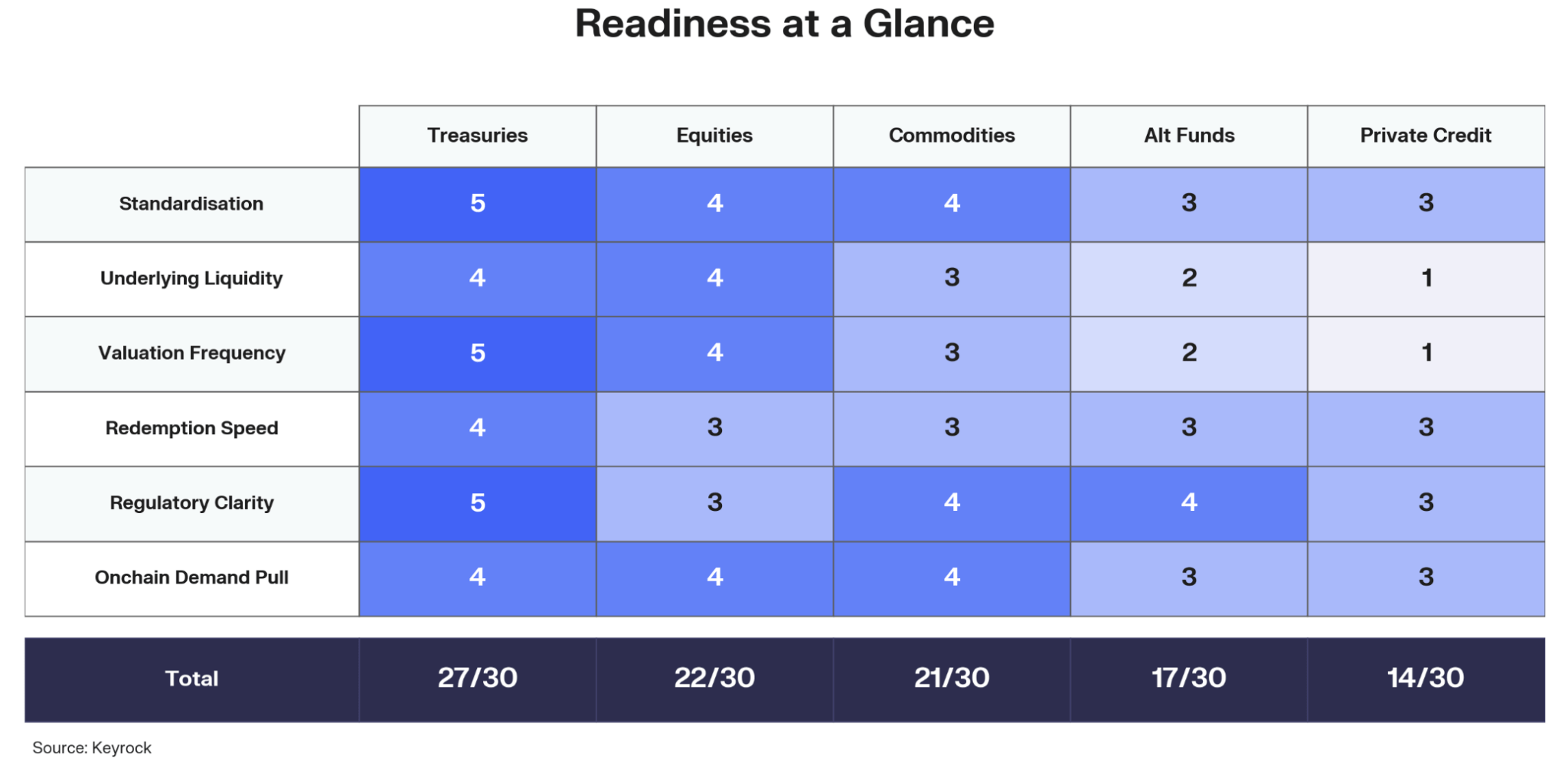

What regulation means for readiness scores

Regulatory clarity is one of six factors in our RWA readiness framework. Today, it is the factor with the widest variance across asset classes. Treasuries benefit from relatively clear treatment as government debt instruments. Private credit operates in regulatory grey zones across most jurisdictions.

As regulation matures, readiness scores across all asset classes will shift upward. The magnitude of the shift depends on how comprehensively each jurisdiction addresses different asset types. Broad frameworks lift all scores. Narrow frameworks benefit specific classes.

Treasuries currently lead at 27 out of 30. Equities follow at 22. Commodities at 21. Alternative funds at 17. Private credit at 14. By 2028, we expect the gap between the highest and lowest scores to narrow significantly as regulatory clarity improves for lagging classes.

Two worldviews collide

Both perspectives hold truth. The regulatory frameworks emerging in 2026 and 2027 reflect a synthesis. Existing investor protection principles applied through new technical mechanisms. Traditional compliance requirements met through onchain verification.

The collision is productive. It is producing frameworks that are more thoughtful than either side would create alone. That is what convergence looks like in practice.

Frequently asked questions

Why is 2027 the key year for tokenisation regulation?

It is projected as the first year when regulation, market depth, liquidity infrastructure, and distribution networks mature simultaneously across major jurisdictions. This convergence enables the move from pilots to production-scale adoption.

How does regulation affect tokenised asset adoption?

Regulatory clarity is one of six factors in the RWA readiness framework. Clear rules enable institutional capital deployment, cross-border distribution, and integration with existing financial infrastructure. Ambiguity keeps capital sidelined.

Which regions are leading tokenisation regulation?

The EU leads with MiCA. The UK advances sandbox programmes. The US is shifting from enforcement-led to legislation-led approaches. Singapore and Hong Kong lead APAC with targeted frameworks.

What regulatory factors score in the RWA readiness framework?

Regulatory clarity evaluates whether an asset class has established legal frameworks for onchain issuance, transfer, and custody across key jurisdictions. It is one of six scoring dimensions alongside standardisation, liquidity, valuation frequency, redemption speed, and onchain demand pull.