Stablecoin Payments, The Trillion Dollar Opportunity

Stablecoin vs SWIFT: Legacy Rails Meet Programmable Money

SWIFT transmits instructions. It does not move money. That distinction, often overlooked, is the fault line on which the entire legacy payments system sits. Stablecoins do both in a single transaction, settling value in seconds rather than days.

Understanding why we built the system we have reveals exactly why we need to replace it.

A brief history of financial plumbing

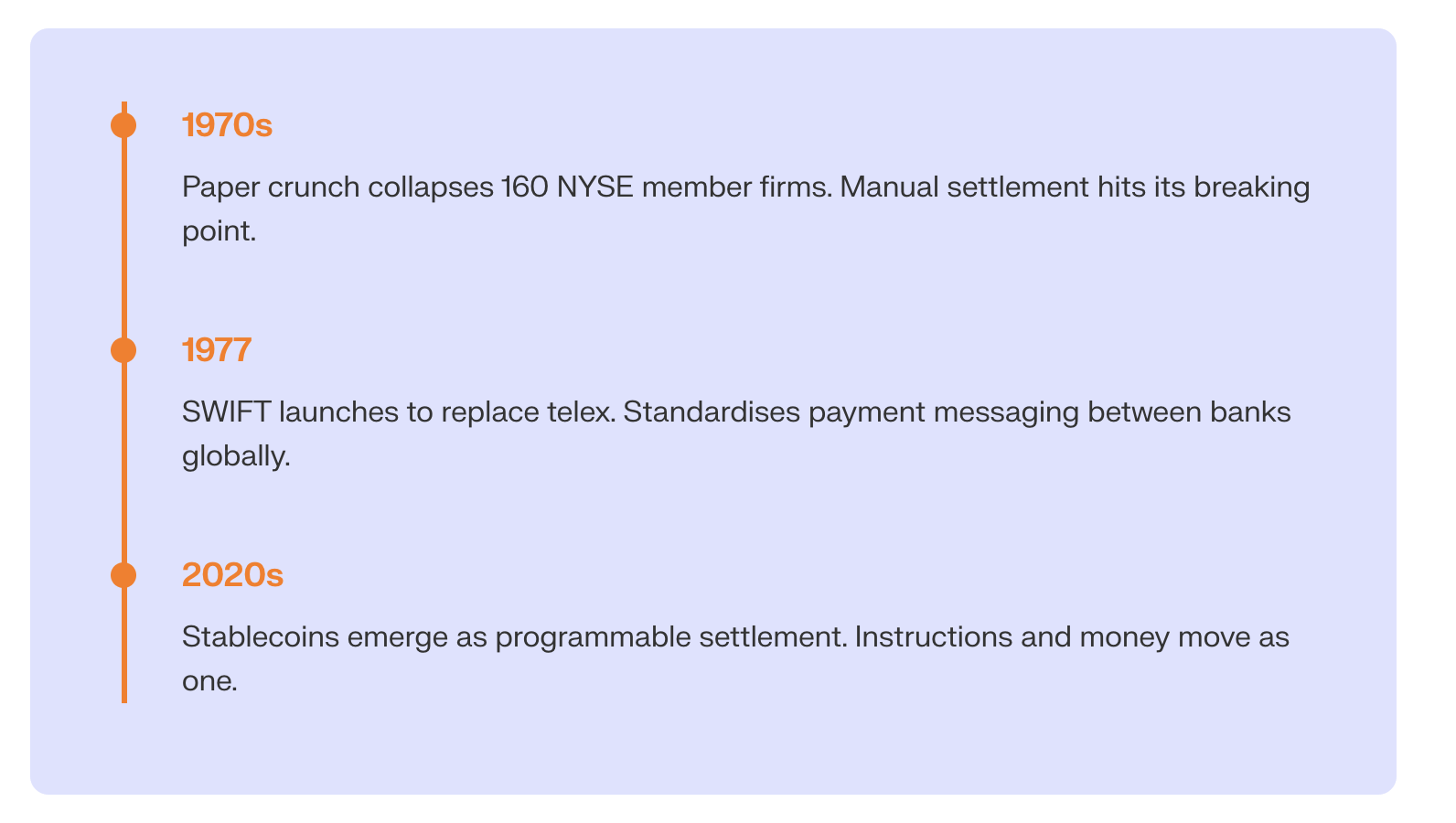

The 1970s paper crunch on Wall Street was a crisis of infrastructure. Trade volumes overwhelmed the manual settlement system. Paper certificates could not move fast enough. The result: 160 NYSE member firms collapsed under the weight of unprocessed paperwork.

That crisis forced modernisation. Electronic settlement systems emerged. And in 1977, SWIFT launched as a standardised messaging network to replace telex machines for inter-bank communication.

SWIFT solved the communication problem. Banks could now send standardised payment instructions across borders reliably. But the money itself still travelled through the same chain of correspondent banks, nostro and vostro accounts, and multi-day clearing processes.

We digitised the message. We left the money analogue.

How SWIFT actually works

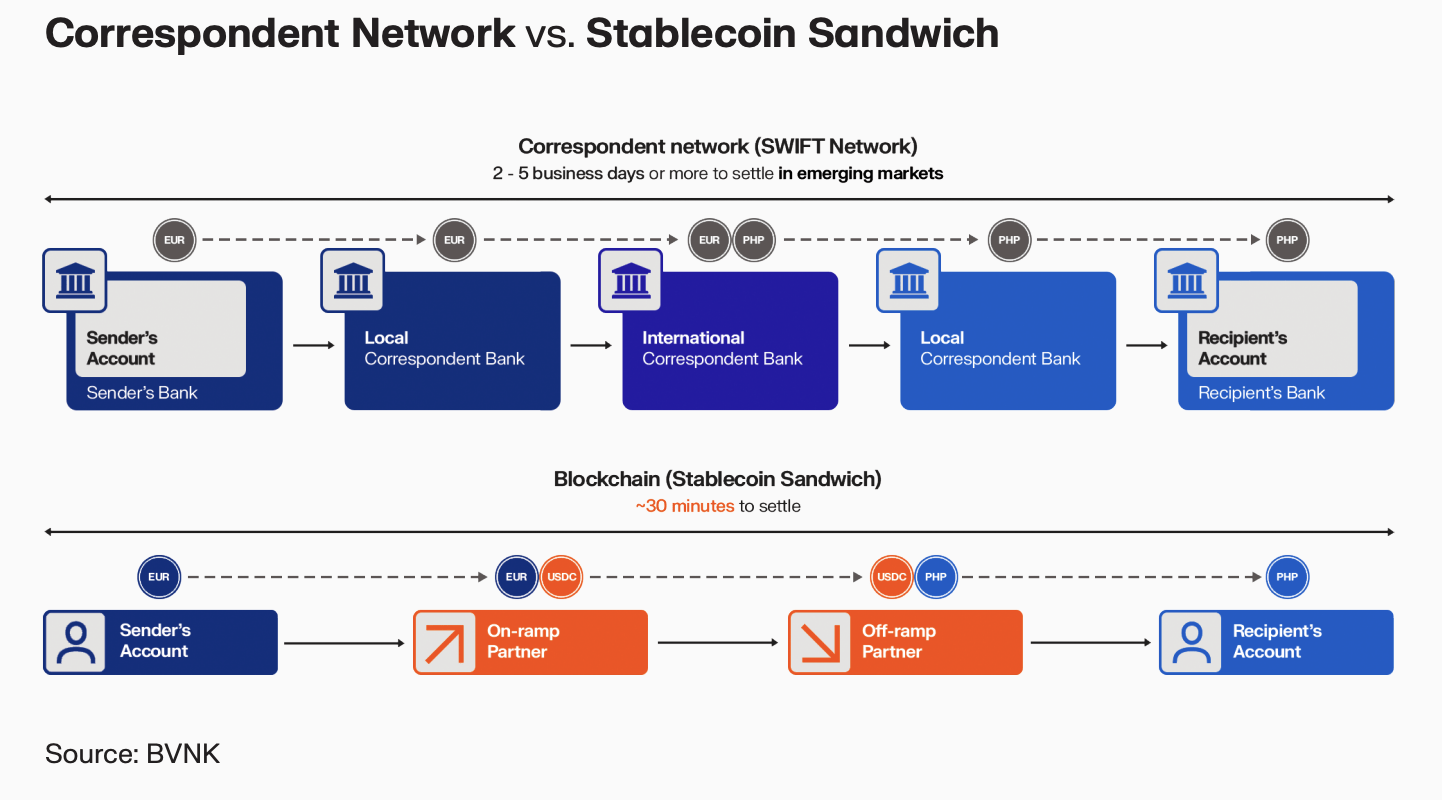

When you send an international payment through your bank, SWIFT carries the message. “Bank A wants to send $1,000 to Bank B.” That message travels instantly. But the actual settlement requires Bank A to have a relationship with Bank B, either directly or through one or more intermediary correspondent banks.

Each intermediary holds pre-funded accounts. Each takes a cut. Each adds compliance checks, reconciliation steps, and processing time. A single payment might touch three or four institutions before reaching its destination.

The FX market processes $7.5 trillion daily through these rails, yet still settles on a T+2 basis. Two full business days of counterparty risk, locked-up capital, and operational uncertainty.

SWIFT connects 11,000+ institutions across 200+ countries. Its network is vast. But network reach and settlement efficiency are two different things. You can have the most sophisticated postal service in the world. It still cannot compete with email.

What programmable money changes

Stablecoins merge the instruction and the settlement into one atomic operation. There is no gap between “Bank A wants to send” and “Bank B receives.” The money moves when the instruction executes.

No correspondent banks. No nostro accounts. No T+2 settlement window.

This is programmable money in its purest form. The payment carries its own settlement logic. Smart contracts can enforce conditions, split payments, convert currencies, and confirm delivery. All in a single transaction.

Settlement finality

SWIFT provides message confirmation. Stablecoins provide settlement finality. The difference matters profoundly for risk management. With SWIFT, you know the instruction was sent. With stablecoins, you know the money has arrived.

For the $7.5 trillion daily FX market, this eliminates Herstatt risk. The atomic nature of onchain settlement means payment-versus-payment is enforced by code, not by trust in counterparties.

Always-on infrastructure

SWIFT operates during banking hours. Settlements depend on cut-off times, time zones, and business day calendars. A payment initiated on Friday afternoon might not settle until Tuesday.

Stablecoins settle 24/7/365. No weekends. No holidays. No cut-off times. This alone transforms working capital management for businesses operating across time zones.

The cost structure

Banks charge roughly 13% to send $200 across a border through the SWIFT-connected correspondent banking system. That fee covers the cost of maintaining pre-funded accounts globally, compliance teams at each intermediary, and the operational overhead of multi-step reconciliation.

Stablecoins collapse this cost structure. Transaction fees on modern blockchains run from fractions of a cent to a few dollars, regardless of transfer size. The 13x cost advantage is structural, not promotional.

Mansa demonstrates what this means in practice: 11x monthly capital turnover versus 1–2x annualised for traditional payment fintechs. The cost savings compound through the entire operational model.

Why SWIFT will not disappear overnight

SWIFT has deep institutional entrenchment. Regulatory frameworks, compliance processes, and banking relationships are all built around it. That creates inertia.

But inertia is not a strategy. The same could have been said about telex in 1976.

The transition will likely follow a familiar pattern: stablecoins will dominate corridors where SWIFT is weakest first. Emerging market corridors with limited correspondent banking coverage. Small-value transfers where fees are proportionally devastating. Real-time commerce that cannot wait for T+2.

Then the use cases will expand. Institutional adoption will follow retail. And the infrastructure will mature to the point where the question shifts from “can we use stablecoins?” to “why would we use anything else?”

Building the bridge

“We want to be the bridge between digital and traditional financial systems.”

— Kevin de Patoul, Keyrock

The future is not binary. It is hybrid. For a period, SWIFT and stablecoins will coexist. Smart institutions are already building infrastructure that connects both worlds, enabling seamless movement between traditional and onchain rails.

This convergence is part of the broader tokenisation shift reshaping financial markets. Stablecoins are the first wave. Tokenised real-world assets are the next.

The 1970s paper crunch taught us that infrastructure must evolve with volume. SWIFT was that evolution. Stablecoins are the next.

History does not wait for incumbents to feel ready.