Stablecoin Payments, The Trillion Dollar Opportunity

Stablecoin Payments: The Trillion Dollar Opportunity

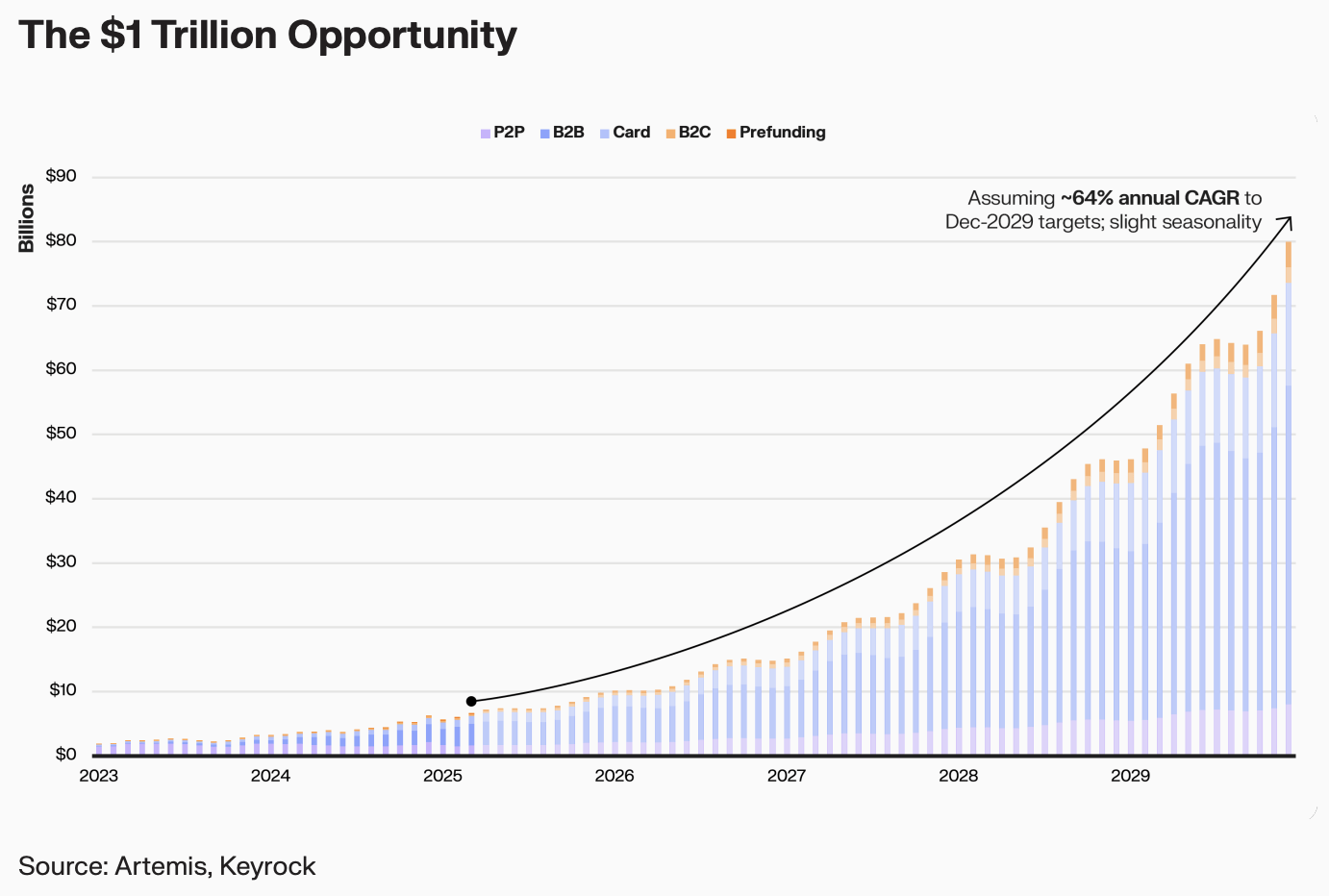

A trillion dollars in annual stablecoin payment volume by 2030. That is not a projection born from hype. It is built on data, on infrastructure already in motion, and on a financial system that has been waiting decades for this upgrade.

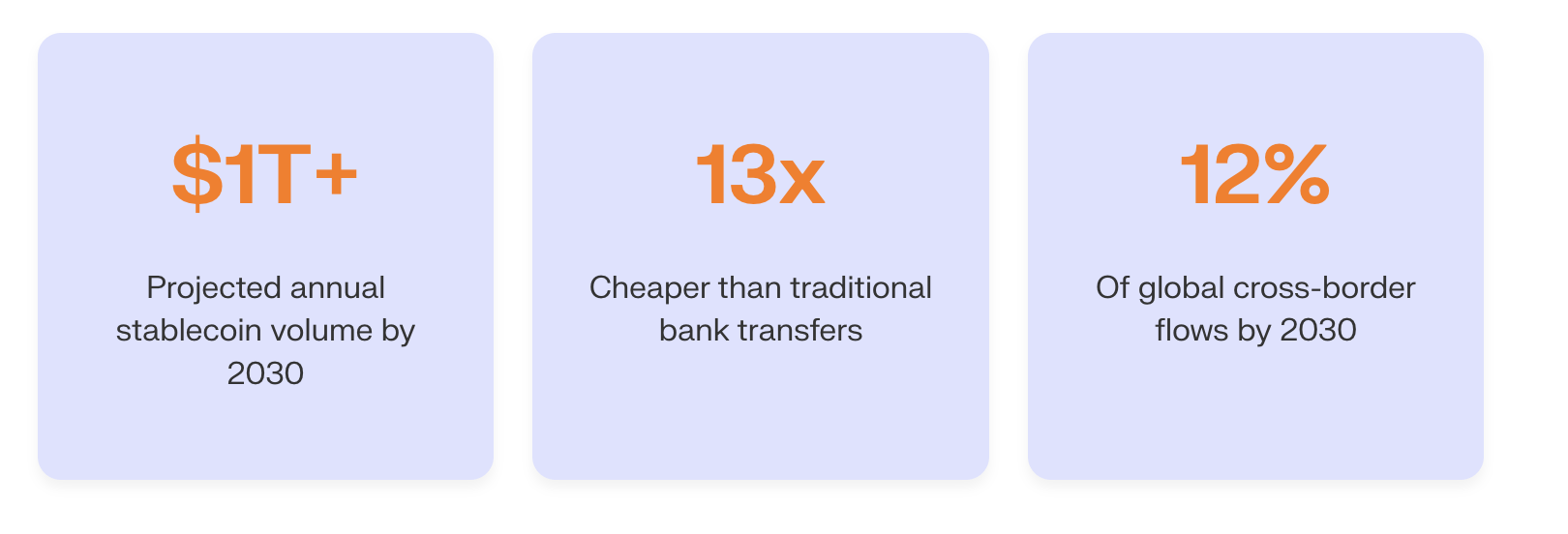

Today, stablecoins represent less than 3% of the $195 trillion global cross-border payment market. Within five years, they are on track to capture 12% of those flows. The speed of this shift is unprecedented. From 0.04% of U.S. M2 money supply in 2020 to over 1% today, stablecoins have already proven their trajectory.

The problem we have been tolerating

Banks charge roughly 13% to send $200 across a border. That fee structure has barely moved in decades. For the 85% of the global population living in emerging markets, these costs are not a minor inconvenience. They are a barrier to economic participation.

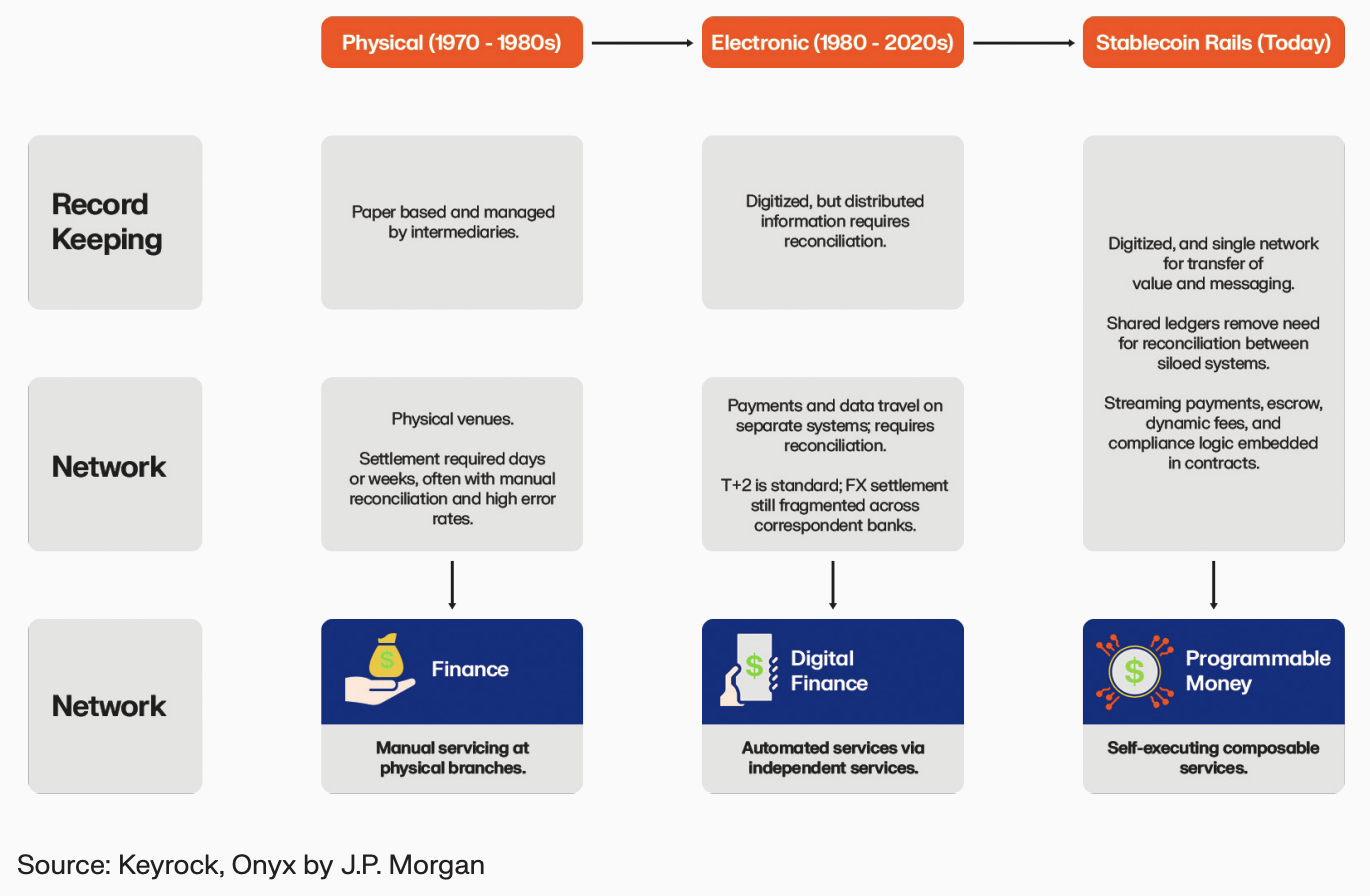

The infrastructure behind these payments was never designed for the modern world. SWIFT launched in 1977 to replace telex machines. It transmits instructions. It does not move money. The foreign exchange market processes $7.5 trillion daily, yet still settles on a T+2 basis.

We are running a digital economy on analogue rails.

Why stablecoins change the equation

Stablecoins collapse the layers. Where a traditional cross-border payment passes through correspondent banks, clearing houses, and settlement networks over days, a stablecoin transfer settles in seconds. Same value. Fraction of the cost.

This is not theoretical. Mansa, a stablecoin-native payments company, achieves an average monthly capital turnover of 11x. Compare that to the 1–2x annualised turnover at traditional fintechs like Wise. The capital efficiency gains are transformative

90% of international trade is invoiced in dollars. Stablecoins make dollar-denominated settlement available to anyone with an internet connection, removing the dependency on correspondent banking networks that have historically locked out billions.

The implications run deep. Onchain FX enables instant, atomic payment-versus-payment settlement. No more counterparty risk from T+2 delays. No more trapped capital waiting for confirmation. The $7.5 trillion daily FX market is ripe for this transformation.

The macro picture: stablecoins and money supply

Stablecoins are projected to account for 10% of U.S. Money Supply by 2030. That number demands attention.

At $2 trillion in supply, stablecoins would hold close to 25% of the Treasury bill market. This is no longer a crypto sideshow. It is a force that directly shapes Federal Reserve policy. The relationship between stablecoins and sovereign monetary tools is becoming inseparable.

Meanwhile, 21% of U.S. commercial deposits earn no yield, representing roughly $3.85 trillion in idle capital. Over $600 million has already been distributed through yield-bearing stablecoins, offering a clear alternative for capital that traditional banks leave dormant.

Every fintech becomes a stablecoin fintech

This is the direction of travel. Not a question of if, but when.

“Every financial institution will have to support stablecoin infrastructure.”

— Devere Bryan, First Digital

The logic is straightforward. If your competitor settles payments instantly at near-zero cost, your T+2 settlement window becomes a liability. If their users earn yield on deposits while yours sit idle, the value proposition speaks for itself.

Stablecoins do not replace financial institutions. They force them to evolve. The firms that build stablecoin infrastructure now will define the next era of financial services. Those that wait will find themselves building on top of someone else’s rails.

Bridging digital and traditional finance

“We want to be the bridge between digital and traditional financial systems.”

— Kevin de Patoul, Keyrock

The opportunity is not purely digital. It sits at the intersection. Tokenised real-world assets are projected to reach $400 trillion. The infrastructure powering stablecoin payments is the same infrastructure that enables tokenised bonds, equities, and commodities to settle onchain.

This convergence is the real story. Stablecoins are the gateway. They prove that programmable money works at scale. Once that is established, the question becomes: what else can we move onchain?

The answer, increasingly, is everything.

What comes next

The cross-border payment corridor is where stablecoins will make their most visible impact first. Emerging markets, home to 85% of the world’s population, stand to gain the most from this infrastructure shift.

But the transformation extends beyond payments. It touches working capital management, FX hedging, treasury operations, and the very structure of how money moves through the global economy.

One trillion dollars in annual volume is just the beginning.