Stablecoin Payments, The Trillion Dollar Opportunity

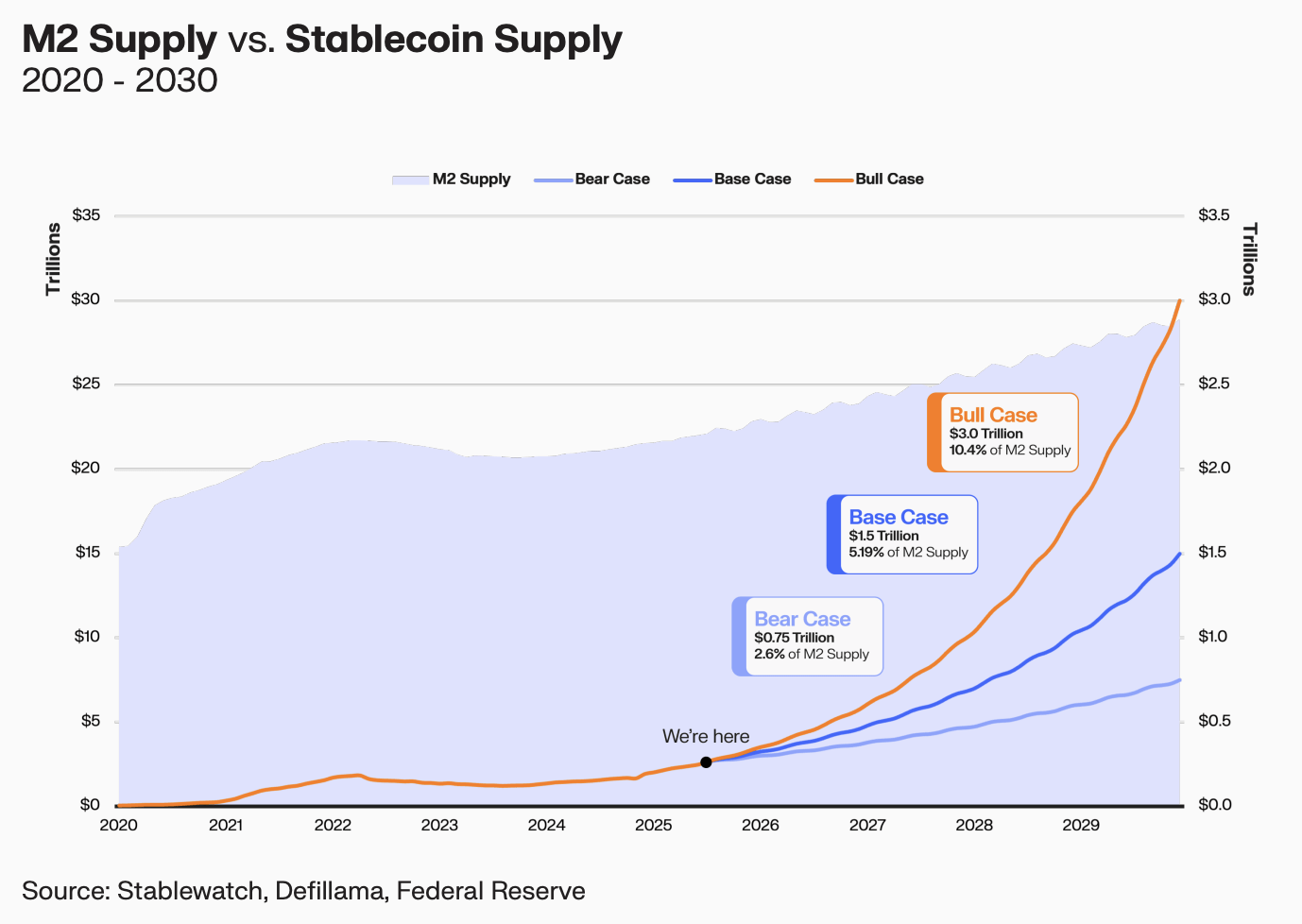

Stablecoins and the U.S. Money Supply: 10% of M2 by 2030

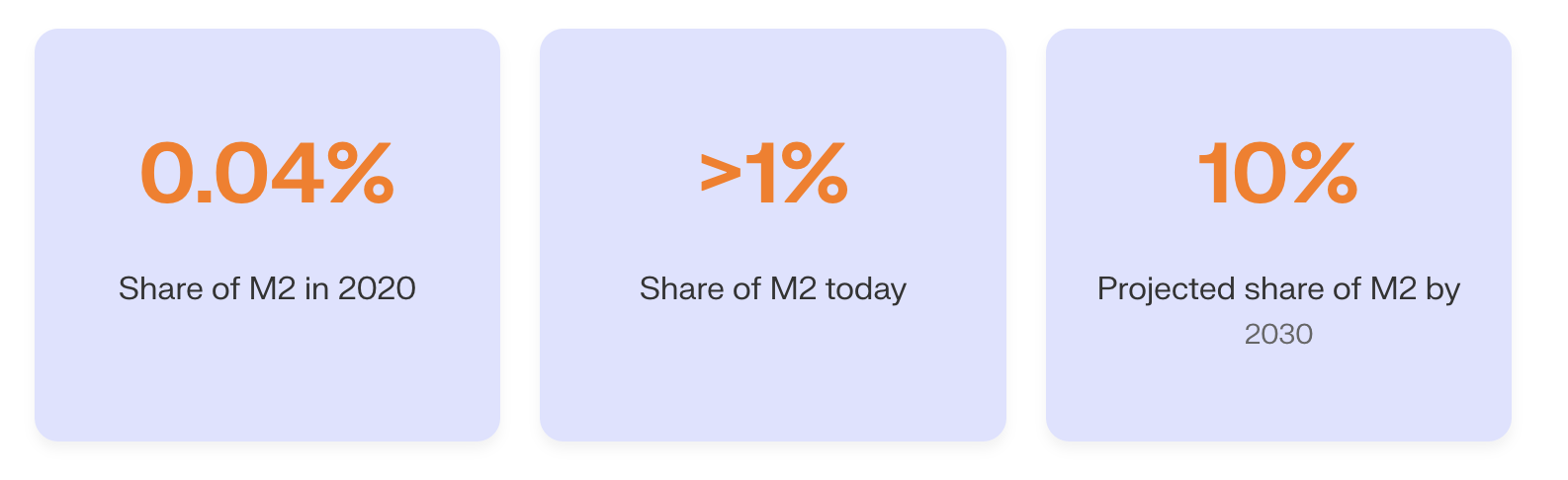

In 2020, stablecoins represented 0.04% of U.S. M2 money supply. Today, that figure exceeds 1%. By 2030, stablecoins are projected to account for 10% of the entire U.S. Money Supply.

Read those numbers again. This is not incremental growth. It is a structural transformation of the monetary system itself.

The Treasury bill connection

Stablecoins do not exist in a vacuum. Every dollar-denominated stablecoin is backed by reserves. For the major issuers, those reserves are predominantly short-dated U.S. Treasury bills.

At $2 trillion in supply, stablecoins would hold close to 25% of the Treasury bill market. That makes stablecoin issuers among the largest buyers of U.S. government debt. The implications for Treasury auctions, yields, and the broader fixed income market are profound.

25% of the Treasury bill market. When a single asset class holds a quarter of the short-term government debt market, it is no longer a peripheral player. It is a systemic participant that the Federal Reserve must account for in every policy decision.

This creates an unusual dynamic. As stablecoin supply grows, demand for Treasury bills grows with it. That supports prices and compresses yields on the shortest-duration government debt. The monetary transmission mechanism now has a new, significant channel that did not exist five years ago.

The idle deposit problem

21% of U.S. commercial deposits earn no yield. That is approximately $3.85 trillion sitting in bank accounts, generating zero return for depositors while banks lend it out for profit.

Yield-bearing stablecoins offer an alternative. Over $600 million has already been distributed to holders through these instruments. The value proposition is straightforward: hold a dollar-denominated digital asset that generates yield from the same Treasury bills that banks use, but passes the return directly to you.

This creates competitive pressure on traditional banking. If stablecoins offer yield on deposits that banks leave dormant, capital flows towards the better product. The banking system must respond, either by offering competitive rates or by watching deposits migrate onchain.

The mechanics of yield-bearing stablecoins

The model is elegant. Issuers invest reserves in Treasury bills and other short-duration instruments. The yield generated flows back to stablecoin holders, either through rebasing (the number of tokens increases) or through appreciation (the token price rises above $1).

For DeFi protocols and working capital managers, this transforms idle cash positions into productive assets. Capital no longer sits dormant between transactions. It earns while it waits.

What this means for Federal Reserve policy

The Fed manages monetary policy through mechanisms that assume a traditional banking structure. Banks hold reserves at the Fed. The Fed adjusts rates. Banks adjust lending. Money supply expands or contracts through the banking multiplier.

Stablecoins disrupt this chain.

When deposits move from banks to stablecoin issuers, those dollars exit the traditional banking multiplier. The issuer buys Treasuries, but does not lend against those deposits the way a bank would. The money supply dynamics shift in ways that existing models do not fully capture.

At 10% of M2, this is not a rounding error. It is a structural change that requires new frameworks for understanding monetary transmission. The Fed must account for:

Treasury demand effects. Stablecoin-driven demand for T-bills compresses short-end yields and influences the yield curve shape.

Deposit migration. Capital flowing from bank deposits to stablecoins reduces the base available for bank lending, tightening credit conditions independently of rate changes.

Velocity changes. Stablecoins move faster than bank deposits. Mansa’s 11x monthly capital turnover versus 1–2x annualised for traditional fintechs illustrates this. Higher velocity means the same supply of stablecoins can support far more economic activity.

The dollar dominance accelerator

There is an irony in the stablecoin story. A technology often framed as challenging traditional finance is actually reinforcing dollar dominance globally.

90% of international trade is invoiced in dollars. Stablecoins extend dollar access to billions who previously had limited or no ability to hold, transact, or save in USD. Emerging market populations use stablecoins as a hedge against local currency volatility, a savings vehicle, and a payment rail.

Every dollar-denominated stablecoin issued creates demand for U.S. Treasuries. That is direct demand for U.S. government debt from a global base of holders who might never open an American bank account. For the U.S. fiscal position, this is an unexpected tailwind.

“Stablecoins do not challenge dollar hegemony. They digitise it. The dollar’s dominance in global trade and finance is being encoded into programmable money that works 24/7, settling instantly across borders.

Regulatory implications

The growth trajectory demands regulatory clarity. Stablecoins sitting at 10% of M2 cannot exist in a regulatory grey area. The question is not whether regulation will come, but whether it will be designed to enable this innovation or constrain it.

Smart regulation would recognise that stablecoins backed by Treasuries are fundamentally different from bank deposits. They do not carry lending risk. They do not use the banking multiplier. They provide transparent, auditable reserves.

The regulatory framework must also address the systemic importance that comes with scale. At 25% of the T-bill market, stablecoin issuers need robust reserve management, regular attestation, and clear rules for redemption. This is where the trillion-dollar opportunity meets institutional reality.

The path from 1% to 10%

The growth from 0.04% to 1% happened without institutional participation, without regulatory frameworks, and without major bank adoption. It was driven by crypto-native demand and cross-border payment utility.

The growth from 1% to 10% will be powered by institutional adoption, regulatory clarity, and integration with traditional finance. Every major fintech becoming a stablecoin fintech accelerates this timeline. Every tokenised asset that settles in stablecoins adds to the supply.

“Every financial institution will have to support stablecoin infrastructure.”

— Devere Bryan, First Digital

The money supply is being reprogrammed. From 0.04% to 10%. The direction is set. The only variable is speed.