Stablecoin Payments, The Trillion Dollar Opportunity

Stablecoins in Emerging Markets: Bridging the Infrastructure Divide for 85% of the World

85% of the global population lives in emerging markets. These are economies with the highest demand for dollar access, the steepest cross-border fees, and the weakest traditional banking infrastructure. Stablecoins were built for this exact gap.

Not designed for it in theory. Built for it in practice.

The infrastructure desert

Traditional banking infrastructure follows wealth. Correspondent banking networks are densest between New York, London, Frankfurt, and Tokyo. Between Lagos and Nairobi, coverage thins dramatically. Between Dhaka and Manila, it is sparse.

The result: populations with the greatest need for financial services pay the highest prices to access them. Banks charge roughly 13% to send $200 across a border. In emerging market corridors, the cost is often higher because the correspondent banking chain is longer.

Mobile money platforms have partially addressed domestic payment needs in markets like Kenya and the Philippines. But cross-border remains broken. A worker in Dubai sending money to a family in Bangladesh faces multiple currency conversions, each with its own spread, and processing times measured in days.

This is not a technology limitation. It is an architecture limitation. The system was not designed to serve these corridors efficiently.

Dollar access as financial infrastructure

90% of international trade is invoiced in dollars. In emerging markets, dollar access is not a convenience. It is a necessity.

Businesses importing goods need dollars to pay suppliers. Exporters receive dollars and need to convert them locally. Families receiving remittances from abroad receive dollars. In each case, the traditional system imposes friction: bank accounts with minimum balances, FX spreads that favour the institution, and processing delays that create real economic cost.

Stablecoins democratise dollar access. A merchant in Accra can hold USDC with nothing more than a mobile phone. A factory owner in Ho Chi Minh City can pay a supplier in Shenzhen in seconds. No correspondent bank. No minimum balance. No three-day wait.

This is bottom-up dollarisation, driven not by central bank policy but by individual economic choices. People in emerging markets are choosing dollar-denominated stablecoins because they solve real problems that local currency and traditional banking cannot.

The remittance corridor

Global remittance flows to low- and middle-income countries exceed $600 billion annually. The fees extracted by the traditional system represent a direct tax on some of the world’s most vulnerable populations.

Stablecoins compress this cost by up to 13x. A $200 transfer that costs $26 through a bank costs under $2 with stablecoins. For a family receiving $200 monthly, that is nearly $300 saved per year. In economies where annual per capita income is measured in hundreds of dollars, that saving is transformative.

Speed matters too. When a family needs money for an emergency medical expense, a three-day settlement window is not an inconvenience. It is a crisis. Stablecoin settlement in seconds changes the economics and the human impact of cross-border money movement.

Capital efficiency in emerging market payments

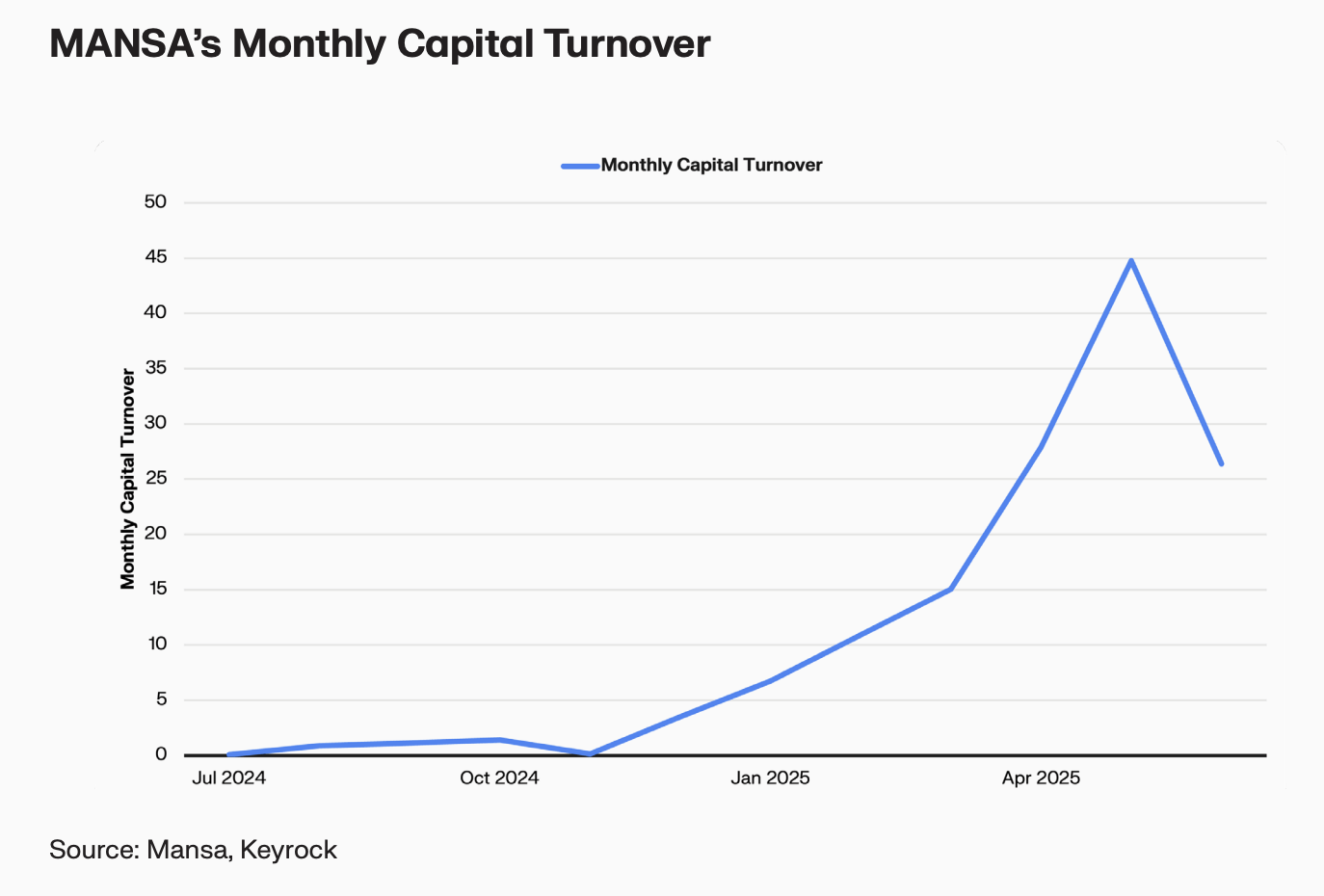

The supply side of emerging market payments is equally transformed. Mansa, a stablecoin-native payments company focused on underserved corridors, achieves average monthly capital turnover of 11x. Traditional fintechs like Wise operate at 1–2x annualised.

That 11x figure is not a marginal improvement. It means the same capital base services more than 60 times the payment volume annually compared to traditional competitors. For payment operators in emerging markets, where capital is scarce and expensive, this efficiency gain determines viability.

Stablecoin rails allow operators to recycle capital within hours rather than days. A payment from London to Lagos settles. The capital is immediately available for the next transaction. No waiting for correspondent bank confirmations. No capital trapped in the settlement pipeline.

Savings and store of value

In countries with inflation running at double digits, holding local currency is a losing proposition. Historically, the alternatives have been limited: physical dollars (scarce, risky to store), gold (illiquid), or property (inaccessible to most).

Dollar-denominated stablecoins add a new option. They offer the stability of the dollar with the accessibility of a mobile wallet. No bank account required. No minimum balance. Available to anyone with internet access.

Yield-bearing stablecoins take this further. Instead of simply preserving value, holders can earn yield on their dollar savings. Over $600 million has already been distributed through these instruments. For emerging market populations with limited access to investment products, this represents a meaningful expansion of financial opportunity.

Trade finance and business payments

Cross-border B2B payments in emerging markets are even more friction-laden than consumer transfers. A business importing goods from China to Nigeria navigates multiple currency conversions, letters of credit, and settlement delays that tie up working capital for weeks.

Stablecoins simplify this to a direct transfer. Dollar-denominated. Instant settlement. Transparent pricing. The onchain FX infrastructure that enables atomic settlement between currency pairs removes the opacity that has historically plagued emerging market trade corridors.

For small and medium enterprises, this is the difference between trading internationally and being locked out of global supply chains. The traditional system’s capital requirements and fee structures favour large corporates. Stablecoins level the field.

The regulatory landscape

Emerging market regulators face a delicate balance. Stablecoins offer clear benefits: financial inclusion, lower costs, and increased access to dollar liquidity. But they also raise concerns about capital flight, monetary sovereignty, and the bypass of local banking systems.

Progressive jurisdictions are finding the middle ground. Regulatory sandboxes, licensing frameworks for stablecoin operators, and integration with existing mobile money infrastructure are emerging as models. The markets that get this balance right will attract capital and innovation. Those that restrict will watch their populations adopt stablecoins regardless, through less regulated channels.

The bridge between worlds

“We want to be the bridge between digital and traditional financial systems.”

— Kevin de Patoul, Keyrock

For emerging markets, this bridge is not aspirational. It is existential. The gap between traditional financial infrastructure and the needs of 85% of the world’s population represents both the greatest challenge and the greatest opportunity in global finance.

Stablecoins are on track to capture 12% of global cross-border flows by 2030. Emerging markets will drive a disproportionate share of that adoption because the alternative, a 13% tax on every transfer, is simply not sustainable.

The tokenisation of financial infrastructure is not just a developed market story. It is a global one. And for 85% of the world, it starts with stablecoins.