Stablecoin Payments, The Trillion Dollar Opportunity

Stablecoin DeFi Working Capital: 11x Turnover and Yield-Bearing Assets | Keyrock

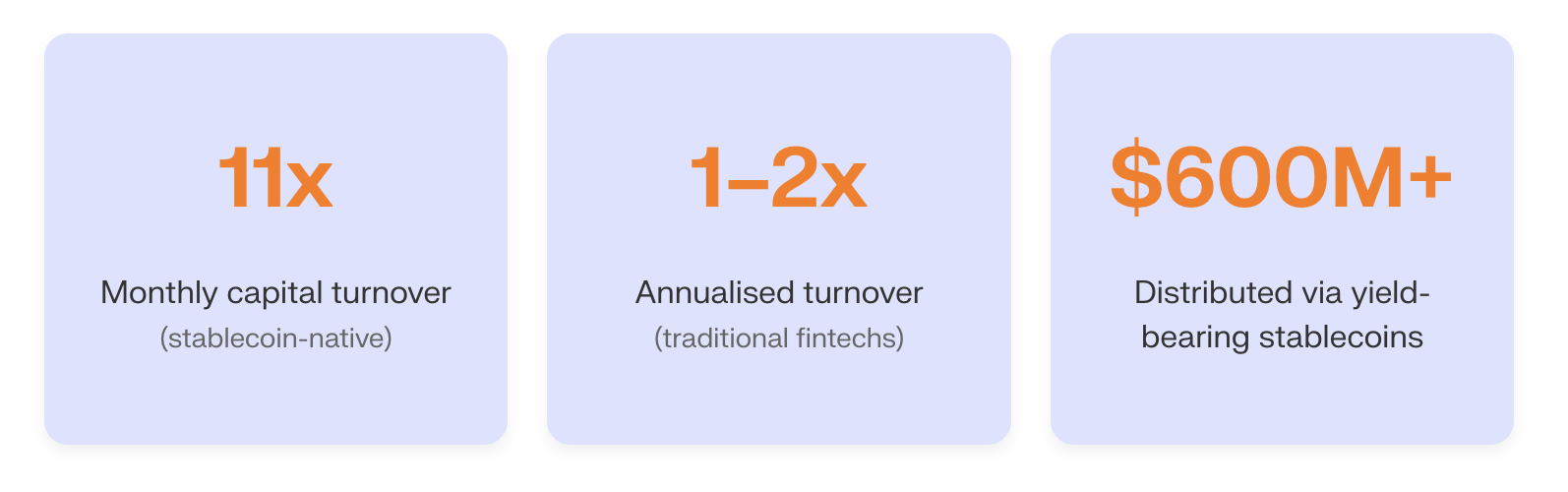

Capital sits idle for days in traditional payment systems. In stablecoin infrastructure, it cycles 11 times per month. That single metric captures the structural advantage that is reshaping how payment companies, treasuries, and financial institutions manage working capital.

This is not about faster payments. It is about fundamentally better capital economics.

The 11x advantage

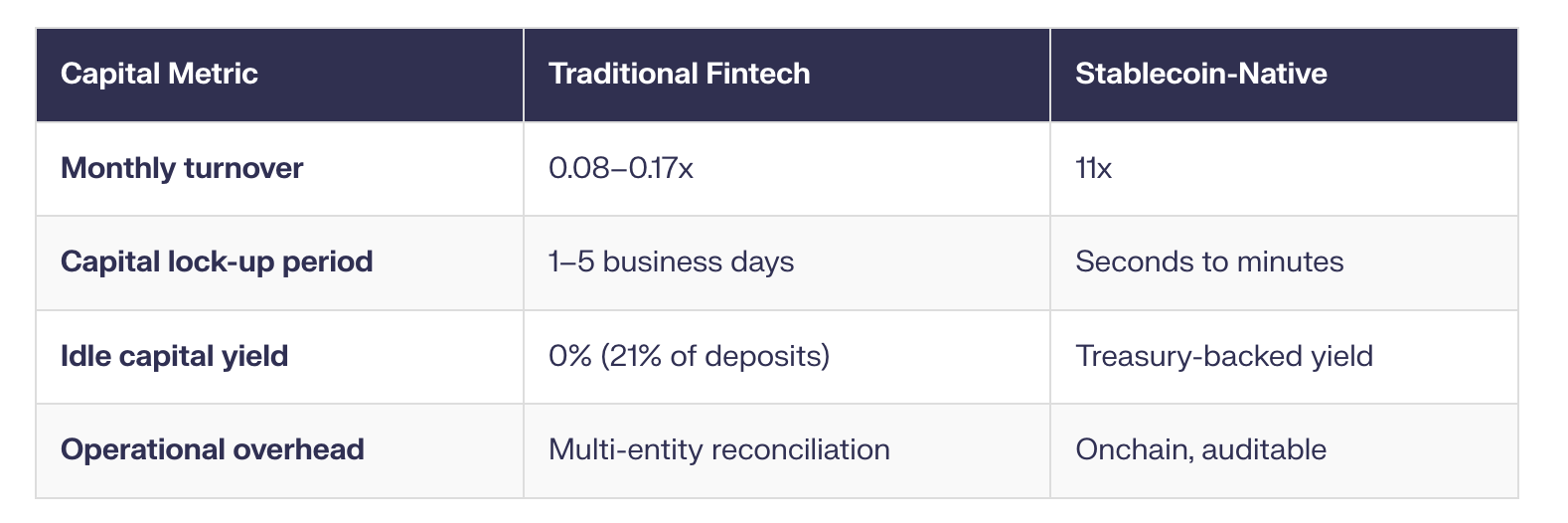

Mansa, a stablecoin-native payments company, achieves average monthly capital turnover of 11x. Traditional fintechs like Wise operate at 1–2x annualised. On an annual basis, that translates to roughly 132x versus 2x. The same pool of capital services 60 times more payment volume.

The mechanics behind this are straightforward. In traditional systems, capital sent through a cross-border payment corridor is locked in the settlement pipeline for one to five business days. During that window, the capital cannot be reused. It sits in correspondent bank accounts, waiting for confirmations to cascade through the chain.

Stablecoins settle in seconds. The moment a transaction confirms, the capital is available for the next payment. This instant recycling is what powers the 11x monthly turnover.

Why capital efficiency matters more than cost

The stablecoin narrative often leads with cost savings. Banks charge 13% on a $200 transfer. Stablecoins do it 13x cheaper. That comparison is powerful but incomplete.

For payment operators, capital efficiency is the deeper advantage. Lower capital requirements mean lower barriers to entry. Higher turnover means higher revenue per dollar of capital deployed. Better unit economics mean the ability to serve corridors that are unprofitable under traditional models.

This is the structural reason why every major fintech will become a stablecoin fintech. The capital economics are too compelling to ignore. A competitor operating at 11x turnover can undercut pricing, serve more customers, and generate higher returns on equity simultaneously.

The $3.85 trillion idle deposit problem

21% of U.S. commercial deposits earn no yield. That is approximately $3.85 trillion sitting in bank accounts, generating zero return for depositors. Banks use these deposits to fund lending, but the depositors themselves see none of the income.

This is a structural subsidy from depositors to banks. It has persisted because depositors had no alternative that combined the convenience of a bank account with competitive yield.

Yield-bearing stablecoins change that equation.

How yield-bearing stablecoins work

The model is precise. Issuers collect deposits and invest the reserves in short-dated U.S. Treasury bills and equivalent instruments. The yield generated flows back to stablecoin holders through one of two mechanisms.

Rebasing. The number of tokens in your wallet increases proportionally to the yield earned. If you hold 1,000 tokens and the daily yield is 0.01%, you wake up with 1,000.1 tokens. Your balance grows automatically.

Appreciation. The token price rises above $1 to reflect accumulated yield. If you hold 1,000 tokens at $1.00 and yield accrues, each token might be worth $1.005. Your balance stays the same, but the value increases.

“Over $600 million already distributed. Yield-bearing stablecoins are not a concept. They are a functioning product class with hundreds of millions in proven distributions to holders globally.

For treasury managers, this transforms how idle cash is handled. Instead of sweeping excess cash into overnight repos or money market funds at end of day, stablecoin-denominated treasury positions earn yield continuously, 24/7, with instant liquidity.

DeFi as payment infrastructure

DeFi protocols are often discussed in the context of trading and lending. Their role as payment infrastructure is underappreciated.

Decentralised exchanges provide onchain FX liquidity. Lending protocols enable capital-efficient pre-funding. Yield aggregators optimise returns on idle balances. Together, these protocols form a composable financial stack that payment companies can integrate modularly.

Mansa’s 11x turnover is powered by this stack. DeFi liquidity allows the company to source and deploy capital dynamically, matching supply to payment demand in real time rather than pre-positioning capital across correspondent bank accounts days in advance.

Composability as competitive advantage

Traditional payment infrastructure is monolithic. Each provider builds its own stack, negotiates its own correspondent banking relationships, and manages its own compliance layer. Switching costs are high. Innovation is slow.

DeFi is composable. Payment companies can plug into shared liquidity pools, swap between yield-bearing and non-yield-bearing stablecoins, and route payments through the most efficient available path. All programmatically. All in real time.

This composability is why stablecoin-native payment companies can launch faster, scale cheaper, and serve corridors that traditional providers cannot justify. The fixed cost base is fundamentally lower when you are composing rather than building.

Treasury management reimagined

Corporate treasuries face a perpetual tension between liquidity and yield. Cash needed for operations earns nothing. Cash invested for yield is not immediately available. Traditional instruments force a choice.

Yield-bearing stablecoins dissolve that tension. A corporate treasurer can hold operational reserves in a token that earns Treasury-bill-equivalent yield and is instantly redeemable for payments. No lockup periods. No redemption delays. No trade-off between liquidity and return.

At $2 trillion in stablecoin supply, the treasury management use case alone could account for hundreds of billions in demand. The institutional appetite for liquid, yield-bearing, dollar-denominated assets is enormous.

The convergence with tokenised assets

Working capital management does not exist in isolation. It connects to the broader tokenised asset ecosystem. Tokenised bonds, money market funds, and commercial paper are emerging as onchain instruments that treasuries can access directly.

Stablecoins serve as the settlement layer for these instruments. When a treasury purchases a tokenised bond, the payment is in stablecoins. When the bond matures, the redemption is in stablecoins. The entire lifecycle is onchain, composable, and instant.

This is the great tokenisation shift applied to working capital. The tools that began as crypto-native DeFi protocols are becoming institutional-grade financial infrastructure.

What this means for financial institutions

“Every financial institution will have to support stablecoin infrastructure.”

— Devere Bryan, First Digital

The 11x capital turnover advantage is not limited to crypto-native startups. Any financial institution that adopts stablecoin rails for its payment operations gains access to the same efficiency. The infrastructure is open. The protocols are permissionless. The yield is available to anyone who holds the tokens.

The firms that integrate stablecoin-based working capital management now will build structural advantages that compound over time. Those that treat this as a distant future will find the future arrived while they were still evaluating.

11x monthly turnover. $600 million in yield distributed. $3.85 trillion in idle deposits waiting for a better option. The numbers are not speculative. They are current.