Stablecoin Payments, The Trillion Dollar Opportunity

Stablecoin Cross-Border Payments: 13x Cheaper, Capturing 12% of Global Flows | Keyrock

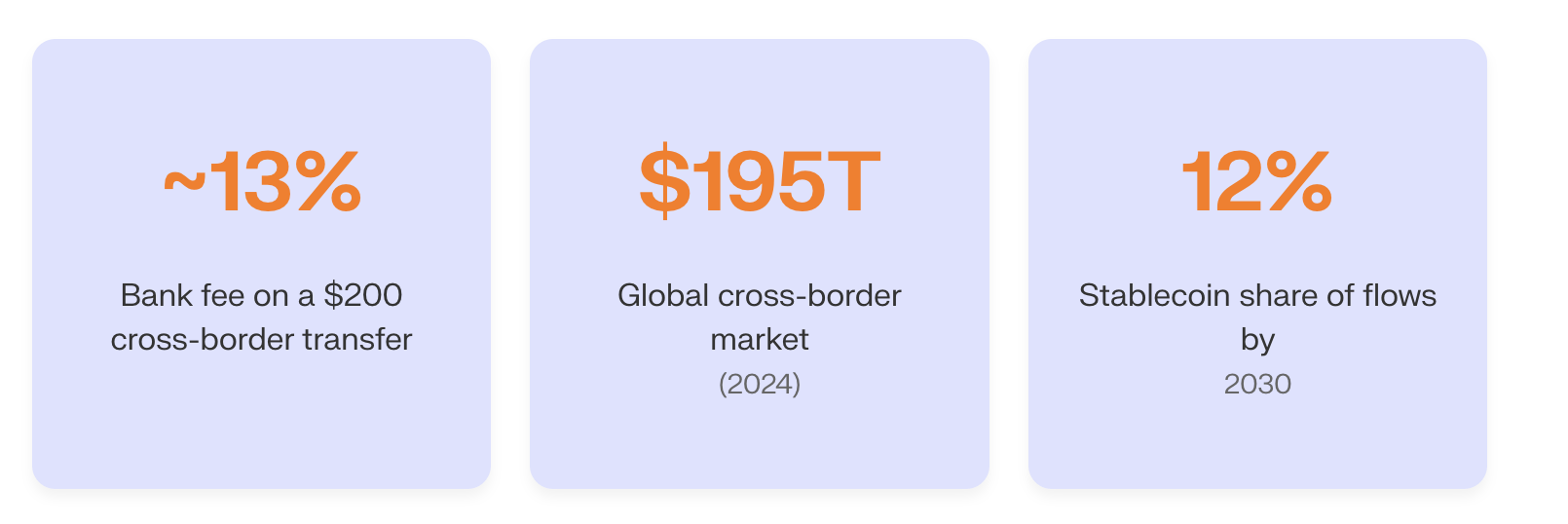

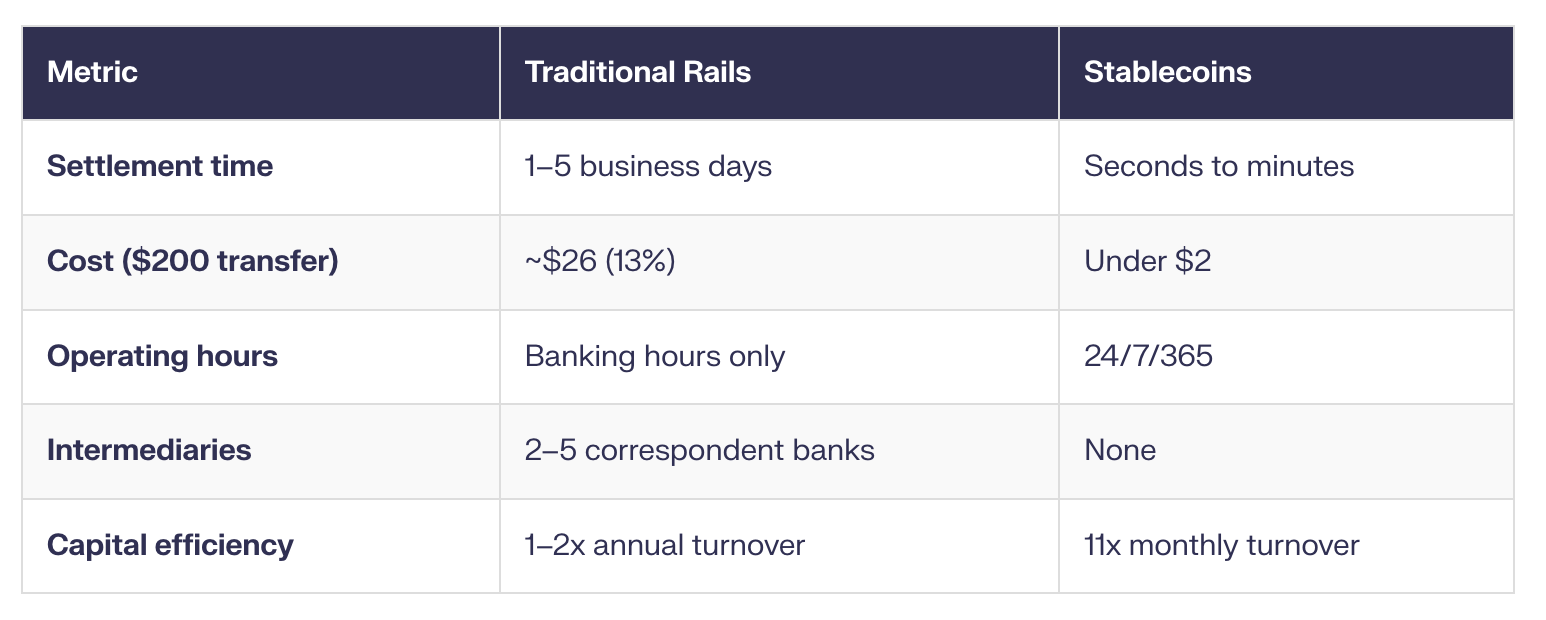

Sending $200 across a border costs roughly $26 in bank fees. That is 13% of the transfer value, disappearing into a chain of intermediaries before the money even arrives. Stablecoins eliminate those layers and settle in seconds at a fraction of the cost.

This is not a marginal improvement. It is a 13x cost reduction on the most basic financial service billions of people rely on.

The scale of the problem

The global cross-border payment market reached $195 trillion in 2024. Stablecoins currently represent less than 3% of that volume. By 2030, they are on track to capture 12% of global cross-border flows, pushing annual stablecoin payment volume above $1 trillion.

The gap between where we are and where we are heading tells you everything about the velocity of this shift.

90% of international trade is invoiced in dollars. Stablecoins provide dollar-denominated settlement to anyone with a wallet. No correspondent bank required. No waiting days for clearing. No opaque fee structures buried in the exchange rate.

How the traditional system works (and why it fails)

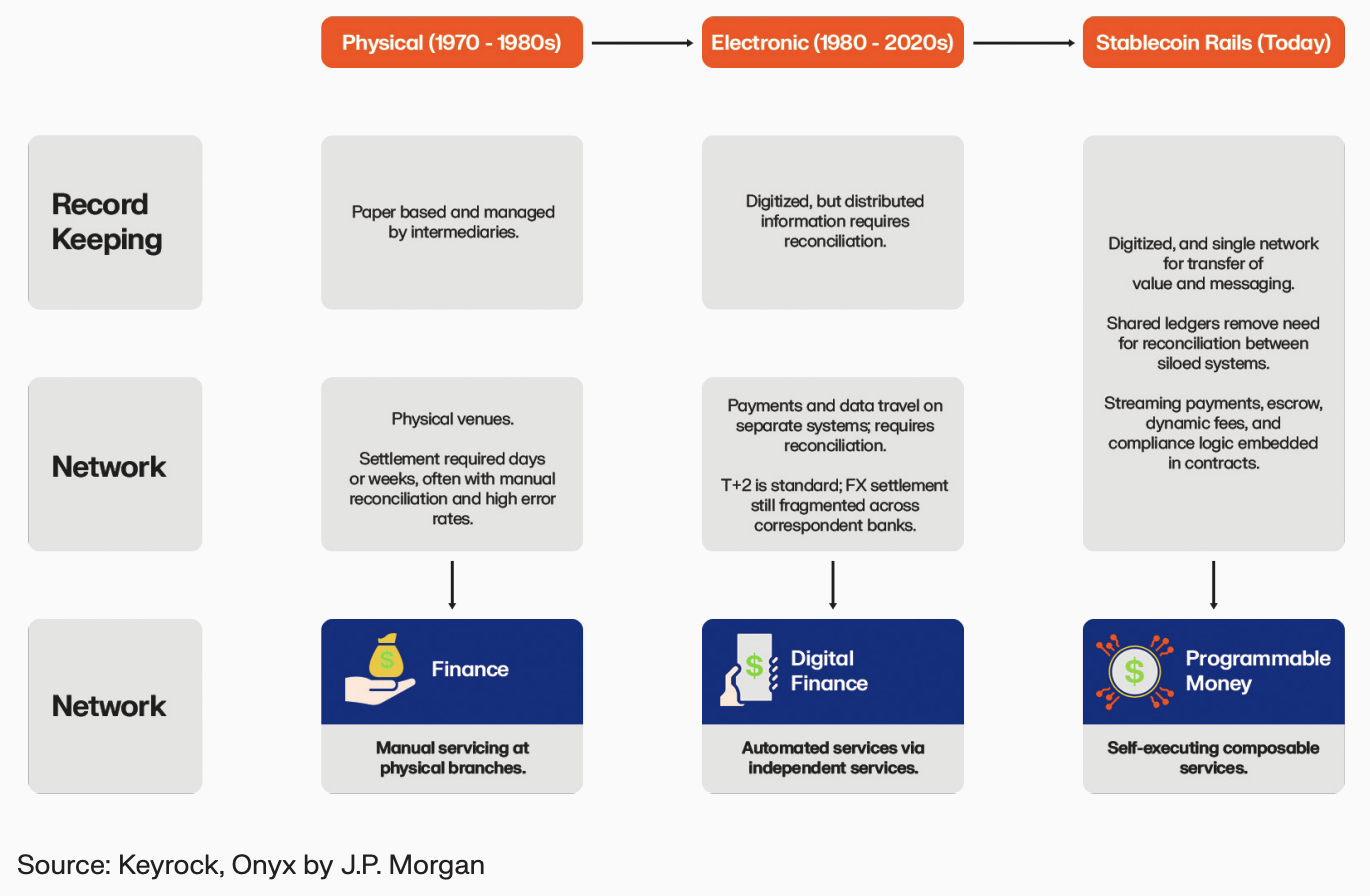

A cross-border payment in the legacy system passes through multiple correspondent banks. Each one takes a fee. Each one adds time. The sender initiates on Monday. The recipient might see the funds on Wednesday. Sometimes Thursday.

SWIFT, launched in 1977 to replace telex, transmits payment instructions between banks. It does not move money. The actual settlement happens through a chain of intermediary accounts, each with its own compliance checks, cut-off times, and reconciliation processes.

For small-value transfers, the economics are punishing. A migrant worker sending money home loses a significant portion to fees that subsidise a system designed for institutional volumes.

What stablecoins change

Stablecoins collapse the correspondent banking chain into a single onchain transaction. Sender to receiver. Seconds, not days. The cost structure is fundamentally different because the intermediaries are code, not institutions.

Capital efficiency: the overlooked advantage

Cost and speed dominate the conversation. But the capital efficiency gains may be even more consequential for businesses.

Mansa, a stablecoin-native payments company, achieves average monthly capital turnover of 11x. Traditional fintechs like Wise operate at 1–2x annualised. That difference is staggering. It means the same pool of capital can service 11 times more payment volume every month.

“11x monthly capital turnover. Stablecoin infrastructure does not just move money faster for end users. It fundamentally changes how payment companies deploy and recycle their working capital, creating a structural advantage that compounds over time.

For payment operators, this translates directly into lower capital requirements, higher throughput, and better unit economics. The efficiency gains flow through the entire value chain, benefiting everyone from the operator to the end user.

For payment operators, this translates directly into lower capital requirements, higher throughput, and better unit economics. The efficiency gains flow through the entire value chain, benefiting everyone from the operator to the end user.

The emerging market opportunity

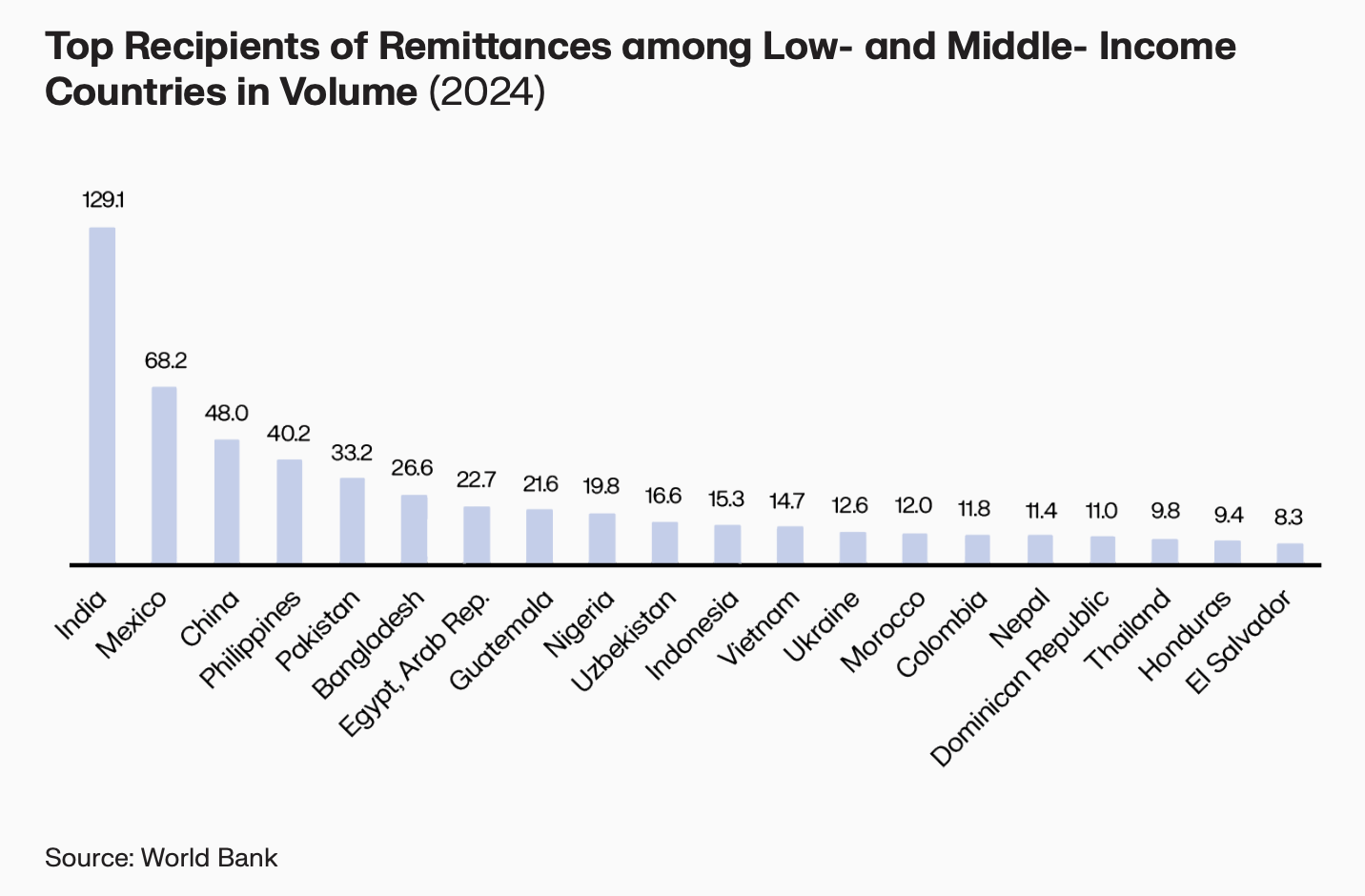

Emerging markets are where stablecoin cross-border payments will make the sharpest impact. These regions, home to 85% of the global population, are chronically underserved by traditional banking infrastructure.

Dollar access is the key unlock. In economies with volatile local currencies, the ability to hold, send, and receive dollar-denominated stablecoins without a U.S. bank account is transformative. It is financial inclusion powered by code rather than branch networks.

Cross-border corridors between emerging markets are particularly underserved. A payment from Nigeria to Kenya through traditional channels can involve multiple currency conversions, each with its own spread. Stablecoins simplify this to a single-hop transfer.

The institutional convergence

This is not only a retail story. Institutional adoption is accelerating.

“Every financial institution will have to support stablecoin infrastructure.”

— Devere Bryan, First DigitalPay

When every major fintech becomes a stablecoin fintech, the cross-border payment landscape transforms completely. The infrastructure that powers DeFi working capital and onchain FX settlement will underpin the next generation of global commerce.

The question for financial institutions is no longer whether to adopt stablecoin infrastructure. It is how quickly they can build it before competitors do.

Where this is heading

12% of global cross-border flows by 2030 is the current trajectory. But trajectories can accelerate. As regulatory clarity improves and institutional infrastructure matures, the adoption curve could steepen significantly.

The great tokenisation shift is already underway. Stablecoins are the entry point, but the destination is a fully programmable financial system where cross-border settlement is instant, cheap, and transparent by default.

We have been tolerating a 13% tax on financial inclusion for decades. That era is ending.