Not all assets are created equal for tokenisation. We scored five classes across six factors. The gaps are revealing.

Why readiness matters more than hype

Every asset class gets a tokenisation narrative. Real estate will be fractionised. Private credit will be democratised. Art will be liquid. The problem is that narrative does not equal infrastructure readiness.

Some assets are structurally suited to onchain issuance today. Others need years of regulatory, technical, and market development before tokenisation delivers real value. Conflating the two wastes capital and delays the assets that are genuinely ready to scale.

We built this framework to cut through the noise.

The six scoring factors

Our readiness framework evaluates each asset class on six dimensions, each scored from 1 to 5. The total gives a score out of 30.

1. Standardisation

How uniform is the underlying instrument? Standardised assets like government bonds or exchange-traded equities tokenise cleanly. Bespoke instruments like private credit deals require custom structuring for each issuance.

2. Underlying liquidity

Deep traditional markets make tokenised versions more credible. A tokenised US Treasury benefits from the world’s deepest bond market. A tokenised real estate portfolio in a single jurisdiction does not carry the same weight.

3. Valuation frequency

Assets valued in real time compose better with DeFi protocols. Treasuries and exchange-traded equities price continuously. Private credit may only update quarterly. Frequent valuation enables tighter spreads and more accurate secondary market liquidity.

4. Redemption speed

How quickly can a holder redeem for the underlying value? Tokenised treasuries can settle within hours. Alternative fund redemptions may take weeks. Speed determines whether the token trades near NAV or at a persistent discount.

5. Regulatory clarity

Clear rules attract institutional capital. Asset classes with established frameworks for onchain issuance and transfer score higher. Ambiguity suppresses adoption regardless of technical readiness. The regulatory landscape is evolving rapidly, but unevenly across classes.

6. Onchain demand pull

Does the crypto-native ecosystem actively want this asset? Tokenised treasuries satisfy stablecoin idle-capital management. Commodities serve as DeFi collateral. Private credit has limited organic onchain demand today.

The readiness scores

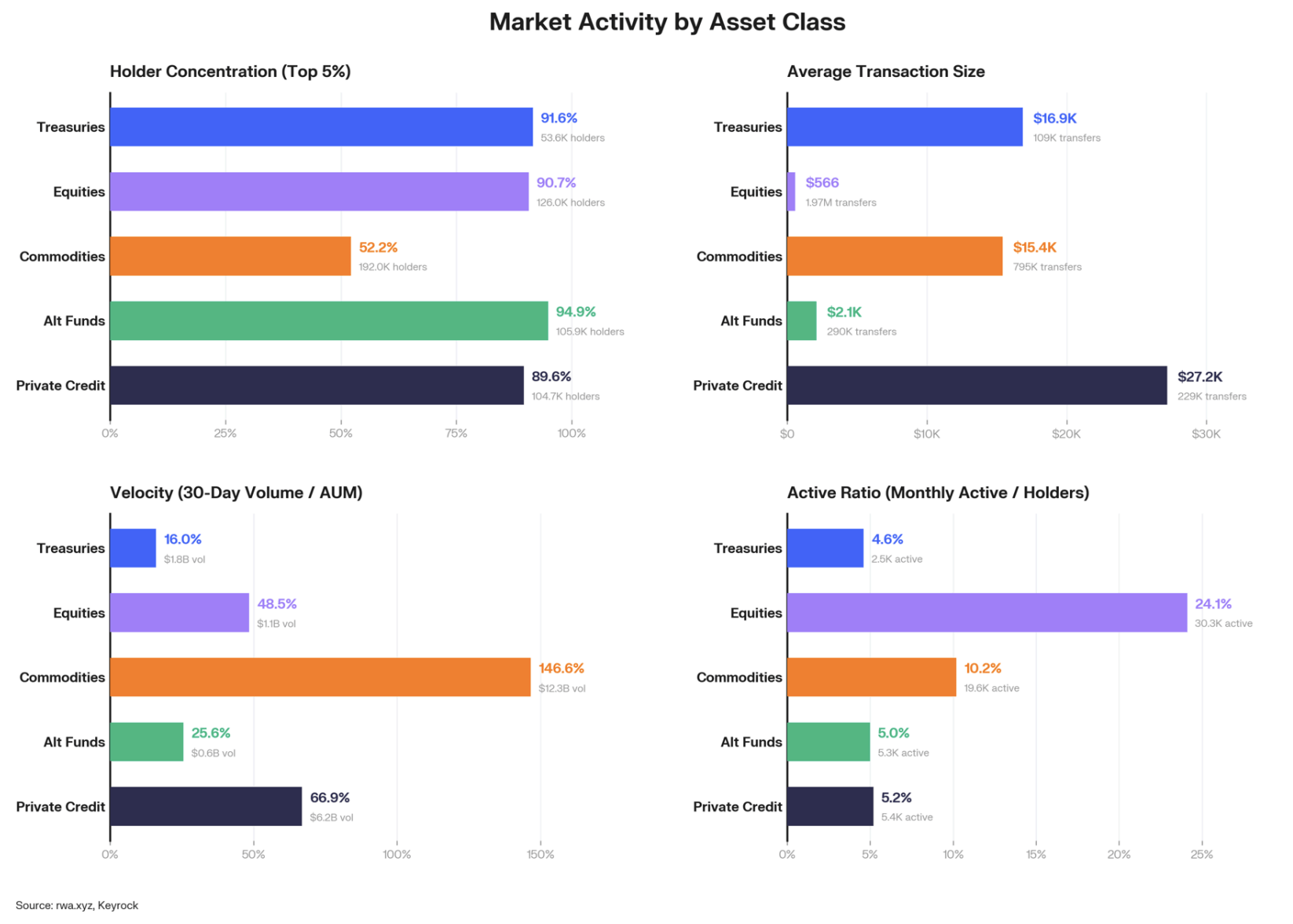

Equities follow at 22. Strong standardisation and liquidity, but regulatory complexity around securities law and cross-border distribution creates friction. The retail skew is notable. Average trade sizes of $566 suggest accessibility is already working.

Commodities score 21, powered by extraordinary onchain demand. They turn over 147% of AUM each month, driven by DeFi collateral use. The underlying markets are deep and standardised. Redemption mechanics and regulatory pathways remain the constraints.

Alternative funds sit at 17. Slower redemption cycles, lower valuation frequency, and more complex structures weigh on the score. But retail participation is emerging. Average trade sizes of $2,100 indicate smaller allocators are finding access points.

Private credit trails at 14. Every factor works against speed. Bespoke deals, infrequent valuations, slow redemptions, unclear regulation, and limited onchain demand create a long path to scale.

Concentration patterns confirm the scores

Wallet distribution data reinforces the framework. In four of five asset classes, over 89% of value sits with the top 5% of wallets. Institutional players are testing and validating the highest-readiness assets first.

This is rational behaviour. Institutions allocate where infrastructure is proven, liquidity is deep, and regulatory risk is manageable. The readiness scores map almost perfectly to observed institutional concentration.

The exception is the retail layer in equities and alt funds. These classes show meaningful participation from smaller wallets, suggesting the accessibility thesis is already proving out at the lower end of the market.

Sequencing the $400 trillion opportunity

The $400 trillion global asset market will not tokenise all at once. Readiness scores give you a sequencing map.

Phase one is already underway. Treasuries and high-grade bonds onchain, serving as yield and collateral infrastructure. Phase two brings equities and commodities as regulatory frameworks mature and distribution networks expand. Phase three unlocks alternative funds and private credit as valuation infrastructure and redemption mechanics improve.

Each phase builds on the last. Treasuries create the yield floor. Equities bring market depth. Commodities add collateral utility. The stack compounds.

What shifts the scores

Readiness is not static. Regulatory clarity can jump when a single jurisdiction publishes a comprehensive framework. Onchain demand pull can spike when a major DeFi protocol integrates a new asset class. Redemption speed improves with infrastructure investment.

We see 2027 as the inflection year. Regulation, market depth, liquidity infrastructure, and distribution mature together for the first time. When that convergence happens, readiness scores across all classes will shift upward. The question is not whether. It is how fast.

The framework is designed to be updated as conditions evolve. Static analysis fails in a dynamic market. We track these six factors continuously.

Frequently asked questions

What is the RWA tokenisation readiness framework?

Keyrock’s framework evaluates five asset classes across six scoring factors: standardisation, underlying liquidity, valuation frequency, redemption speed, regulatory clarity, and onchain demand pull. Each asset class receives a score out of 30.

Which tokenised asset class has the highest readiness score?

Tokenised treasuries lead at 27 out of 30. Equities follow at 22, commodities at 21, alternative funds at 17, and private credit at 14.

What factors determine whether an asset class is ready for tokenisation?

Six factors drive readiness: standardisation, underlying liquidity depth, valuation frequency, redemption speed, regulatory clarity, and onchain demand pull from DeFi and crypto-native participants.

Why does private credit score lowest for tokenisation readiness?

Private credit instruments lack standardisation, have infrequent valuations, slow redemption cycles, limited regulatory frameworks for onchain issuance, and low organic onchain demand compared to treasuries or commodities.