Prediction Markets: The Next Frontier of Financial Markets

How Prediction Markets Are Pricing Token Generation Events (TGEs) in 2026

Token launches have been mispriced for years. Private round anchoring. OTC whispers. Influencer hype masquerading as valuation. None of it produces reliable price discovery. Prediction markets change that — replacing guesswork with real capital at risk, deployed across transparent forward valuation curves that update in real time.

The Keyrock and Dune research report calls it a “default external pricing oracle” for token valuations. We call it the end of closed-door TGE pricing.

Why Traditional Pre-TGE Pricing Fails

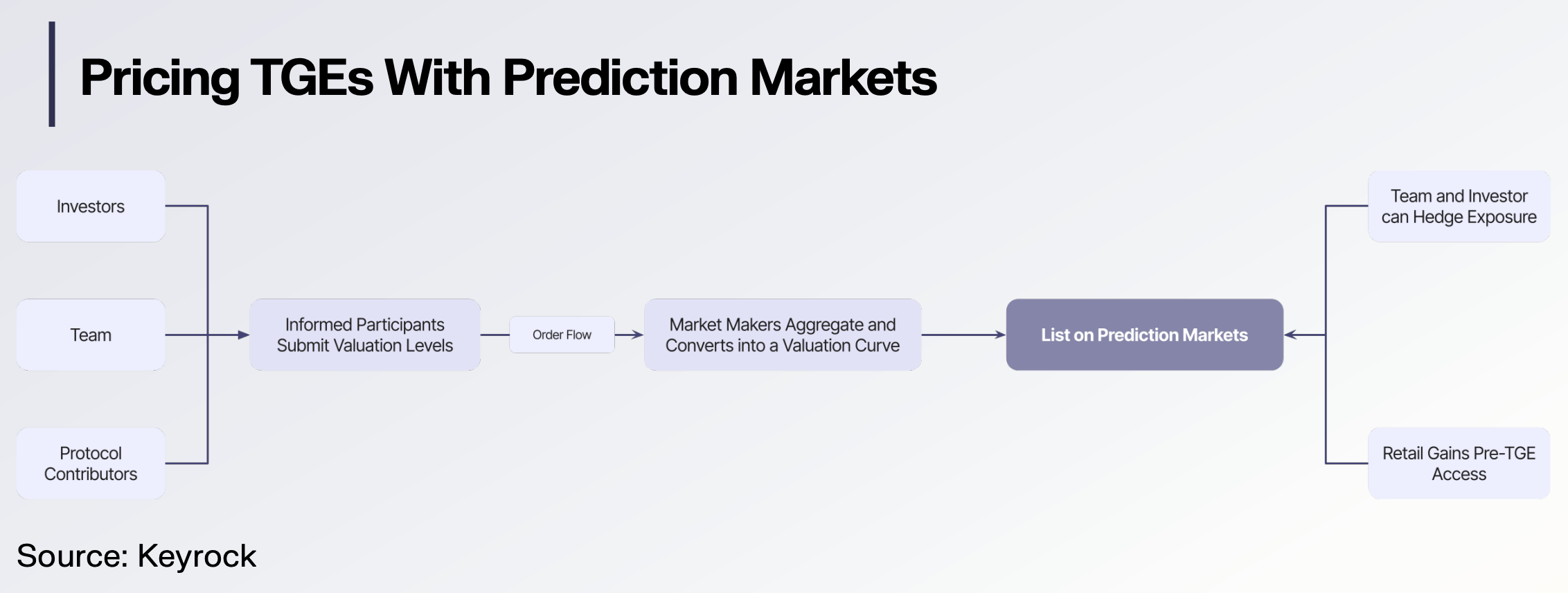

The current model is broken. It harms every participant in the ecosystem.

Early-stage investors negotiate private round prices in bilateral deals. Those valuations anchor to the previous round rather than forward-looking market conditions. The prices leak through OTC desks, where a small group of sophisticated traders mark up and mark down based on information asymmetry.

Meanwhile, retail participants — the eventual holders and users — have zero access to pre-launch price discovery. They show up on day one and accept whatever opening price they get. Set by listing partners, early LPs, or the team itself. The disconnect between insider pricing and public launch pricing has been a consistent source of controversy: inflated FDVs that crash post-TGE, tokens opening far below private round levels.

Social sentiment makes it worse. When the only public signals before a TGE are influencer endorsements and Discord activity, the “price” is not a price. It is a narrative. Prediction markets inject financial accountability by requiring traders to commit capital to specific valuation outcomes.

How Prediction Markets TGE Pricing Works

The mechanics are structured and precise. Event contracts reference a token’s FDV at TGE or TGE + 30 days. Rather than a single yes/no question, the market creates a grid of strikes — escalating valuation thresholds that together form a probability distribution.

A typical grid:

- “FDV >= $250M” — Trading at $0.80 implies an 80% probability the token launches at or above $250M FDV

- “FDV >= $500M” — Trading at $0.55 implies a 55% probability of reaching this level

- “FDV >= $750M” — Trading at $0.25 implies a 25% probability

- “FDV >= $1B” — Trading at $0.10 implies a 10% probability of a billion-dollar launch

Together, these contracts form a forward valuation curve. A probabilistic map of where the market believes the token will land. As new information emerges — partnerships, regulatory clarity, competitor launches, macro shifts — prices adjust in real time. A living estimate, infinitely more informative than a static private round price.

Market Makers Structure the Line

Market makers aggregate indications from institutional and retail participants. They assess depth at each strike level. They convert the output into a structured pricing line. This is not casual. According to our research, seven to eight figures of notional are typically required before the line is locked and considered reliable.

The market maker earns a packaging fee for sourcing, structuring, and validating. The prediction market platform earns a listing fee for hosting the fully seeded market. Both are incentivised to produce clean, well-structured markets — because the quality of the pricing line determines institutional participation.

Multi-Strike Markets Surface Granular Expectations

A traditional OTC market produces a single indicative price. Say, “$75M FDV” from a few bilateral conversations. But what does that actually mean? Is it the consensus? The floor? The ceiling?

A prediction market grid answers with precision.

If the $50M contract trades at $0.60, the $75M contract at $0.30, and the $100M contract at $0.10 — you now have a probability distribution, not a point price. The market says: 60% chance of at least $50M, 30% chance of $75M, 10% chance of $100M. That carries radically more information for decision-making than any single OTC quote.

For project teams: invaluable for setting tokenomics, scheduling unlock schedules, calibrating marketing expectations. For investors: transparent benchmarks to evaluate whether a private round allocation is correctly priced relative to public market expectations. This is “market-driven tokenomics” — token design informed by transparent public pricing rather than internal negotiation.

Hedging TGE Exposure Without Touching the Cap Table

Early backers face concentrated exposure to a single event. Seed investors. Strategic partners. Team members with token allocations. If the token launches below entry price, the thesis is impaired. If it launches well above, they face pressure to sell immediately — creating downward force.

Prediction markets offer a way to hedge without modifying a single cap table entry.

An early backer who participated at a $300M FDV equivalent can sell “FDV >= $500M” contracts to lock in partial gains if the launch exceeds expectations. Or buy “FDV >= $200M” contracts as insurance against a disappointing launch. Cash-settled. No tokens change hands. No lock-up provisions violated.

Today, the only alternative is bilateral OTC forward contracts — illiquid, counterparty-dependent, and available only to a small group of sophisticated players. Prediction markets democratise this access entirely.

Retail Gets Pre-TGE Exposure

The democratisation extends to retail. Through cash-settled contracts, anyone can gain synthetic exposure to a token’s TGE performance. A retail trader who believes a major protocol will launch above $1B FDV can express that view — without needing a private round allocation, an OTC desk relationship, or any insider access.

This matters. The entire history of crypto token launches has been defined by asymmetric access: insiders get cheap tokens, retail pays market price on day one. Prediction markets do not eliminate this dynamic entirely. But they create a public pricing layer that gives retail participants information parity at minimum — and economic exposure to pre-TGE outcomes on equal terms at best.

From Internal Negotiation to Market-Driven Tokenomics

When a project team can observe in real time how the market prices their token at various FDV levels, they receive feedback that was previously unavailable before launch day.

If the market prices a high probability at $250M but near-zero at $1B, the team knows that aiming for a billion-dollar launch valuation will likely result in a post-TGE crash. If the distribution clusters tightly around $500M, they can confidently set initial liquidity and listing parameters around that range.

Let external capital dictate valuation ranges rather than internal models and venture investor expectations. That is market-driven tokenomics in practice.

As Nass Diba of Worm noted, the untapped opportunities in prediction markets extend far beyond finance into culture, attention, and decision-making. TGE pricing is one immediate, high-value application — but it represents a broader template for using prediction markets to surface collective intelligence wherever stakes are high and information is fragmented.

The Business Model: How Platforms and Market Makers Earn

The economics create a sustainable model for every participant in the value chain:

- Market makers earn a packaging fee for sourcing indications, validating pricing quality, and structuring the multi-strike grid. Reputation depends on producing reliable, well-calibrated pricing lines — aligning their incentives with market accuracy.

- Prediction market platforms earn a listing fee for hosting the fully seeded market. A well-structured TGE market attracts institutional flow, boosts volume, and positions the platform as critical infrastructure for token launches.

- Project teams benefit from transparent price discovery, reduced information asymmetry, and the ability to calibrate launch parameters based on real market signals.

- Traders — institutional and retail — gain access to a new asset class of event-driven contracts with clear resolution criteria and bounded payoff structures.

What Comes Next: TGE Pricing as Default Infrastructure

The trajectory points toward a future where no major token launch occurs without a corresponding prediction market. Just as road shows and book-building became standard for IPOs, multi-strike FDV markets could become default pre-launch infrastructure for tokens.

The pieces are in place. Prediction market platforms handle seven- and eight-figure notional volumes. Market makers have developed the structuring expertise. Regulatory clarity — particularly the 2024 Kalshi ruling establishing that event contracts are not gaming — provides the legal framework for institutional participation.

What remains is adoption. Projects choosing prediction markets over private OTC channels. Investors demanding transparent pre-launch price discovery. Retail communities recognising that prediction market prices carry more signal than social media hype.

The shift from “what does the team say this token is worth?” to “what does the market say?” — that is the defining transition. And it is already underway.

Frequently Asked Questions

How do prediction markets price token launches?

Through structured event contracts at multiple FDV strike levels — for example, contracts at $250M, $500M, $750M, and $1B. Each contract’s trading price reflects the market’s implied probability that the token will reach that valuation at TGE or TGE + 30 days. Market makers aggregate indications and structure a pricing line, typically requiring seven to eight figures of notional before it is locked.

Can you hedge pre-TGE risk with prediction markets?

Yes. Early backers, team members, and strategic investors can hedge their TGE exposure by trading cash-settled prediction market contracts at various FDV levels. This allows insiders to manage risk without selling tokens, modifying cap table entries, or violating lock-up provisions. It is a structurally different — and far more accessible — approach than bilateral OTC forward contracts.

What is a TGE valuation line?

A TGE valuation line is a forward pricing curve constructed by market makers from aggregated trading indications across multiple FDV strike points. It represents the market’s collective expectation for a token’s valuation at launch. The line is considered locked once sufficient notional volume — typically seven to eight figures — has been committed, ensuring the pricing reflects genuine capital commitment.

How do prediction markets replace OTC for token pricing?

Traditional pre-TGE pricing depends on opaque OTC deals between a small number of sophisticated participants. Prediction markets replace this with transparent, exchange-traded contracts at multiple valuation thresholds. Anyone can participate, all prices are publicly visible, and the resulting probability distribution carries far more information than a single bilateral OTC price. This shifts token pricing from a closed, relationship-driven process to an open, market-driven one.