Prediction Markets: The Next Frontier of Financial Markets

Prediction Market Regulation — The Legal Landscape in 2026

One court ruling redefined an entire industry. In 2024, the Kalshi decision established that event contracts are financial instruments — not gambling products. The Keyrock and Dune research report calls it “the single most important regulatory precedent in prediction market history.” Everything else in this sector’s legal framework flows from that distinction.

But one ruling does not settle the matter entirely. Prediction market regulation in 2026 exists at the intersection of federal derivatives law, state gaming statutes, judicial interpretation, executive agency discretion, and emerging international frameworks. You need to understand each layer — and the risks that remain.

The Kalshi Ruling: Why It Changed Everything

In 2024, Kalshi — the first CFTC-registered Designated Contract Market (DCM) for event contracts — won its landmark case. The core question: do political event contracts constitute “gaming” under the Commodity Exchange Act (CEA)? The CFTC had moved to block Kalshi from listing election-related contracts, arguing they fell under the CEA’s prohibition on gaming activities.

The court disagreed. Decisively.

The reasoning was devastating to the anti-prediction-market position: if election trading were classified as gambling, then weather derivatives, interest rate futures, and commodity futures would all have to be classified as gambling too. They all involve placing financial stakes on uncertain future events. The distinction between a financial derivative and a gambling product cannot rest on subject matter alone.

Why this matters practically: it shifts prediction market regulation from the gaming framework — where state gaming commissions hold authority and restrictions are severe — to the financial regulation framework, where the CFTC and SEC provide established, market-friendly oversight. For institutional participants, this is the difference between a product they can touch and one compliance will never approve.

A History of Prediction Market Regulation: From InTrade to Polymarket

Where we stand today only makes sense in context. The regulatory history is a story of repeated cycles: innovation, growth, enforcement, recalibration.

InTrade and the 2012 CFTC Enforcement

InTrade was one of the most popular prediction markets of the pre-blockchain era. Operating from Ireland, serving a global user base including significant U.S. participation. In 2012, the CFTC took enforcement action for offering commodity options trading to U.S. customers without registration. InTrade was pushed out of the U.S. market and shut down in 2013 following financial irregularities.

The message was clear: no registration, no U.S. access.

Augur and the Permissionless Alarm (2018)

When Augur launched on Ethereum as one of the first decentralised prediction market protocols, it raised immediate regulatory alarms. Not because of election contracts — but because of “death pool” markets allowing bets on whether specific individuals would die by certain dates. The permissionless nature meant anyone could create any market, and no central authority could remove them.

Augur demonstrated the tension that still defines decentralised prediction market regulation: how do you regulate a protocol that no single entity controls?

Polymarket’s CFTC Settlement and Re-Entry

Polymarket emerged as the dominant blockchain-based prediction market during the 2024 U.S. election cycle. It also faced regulatory consequences. The platform settled with the CFTC for operating without proper registration — even decentralised-architecture platforms face regulatory obligations when serving U.S. users.

Following the settlement, Polymarket re-entered the U.S. market in late 2025 through QCEX, a regulated infrastructure partner providing the compliance layer the CFTC requires. The trajectory: innovate fast, face enforcement, restructure through regulated channels. Whether this pattern is sustainable remains an open question.

The Classification Debate: Financial Instrument or Gambling Product?

Classification is the fundamental question. How a jurisdiction classifies event contracts determines which regulatory body has authority, what rules apply, and what restrictions exist.

The Kalshi ruling resolved this for the U.S. federal system. Event contracts are financial instruments regulated by the CFTC, not gaming products regulated by state commissions. But the debate is far from settled globally.

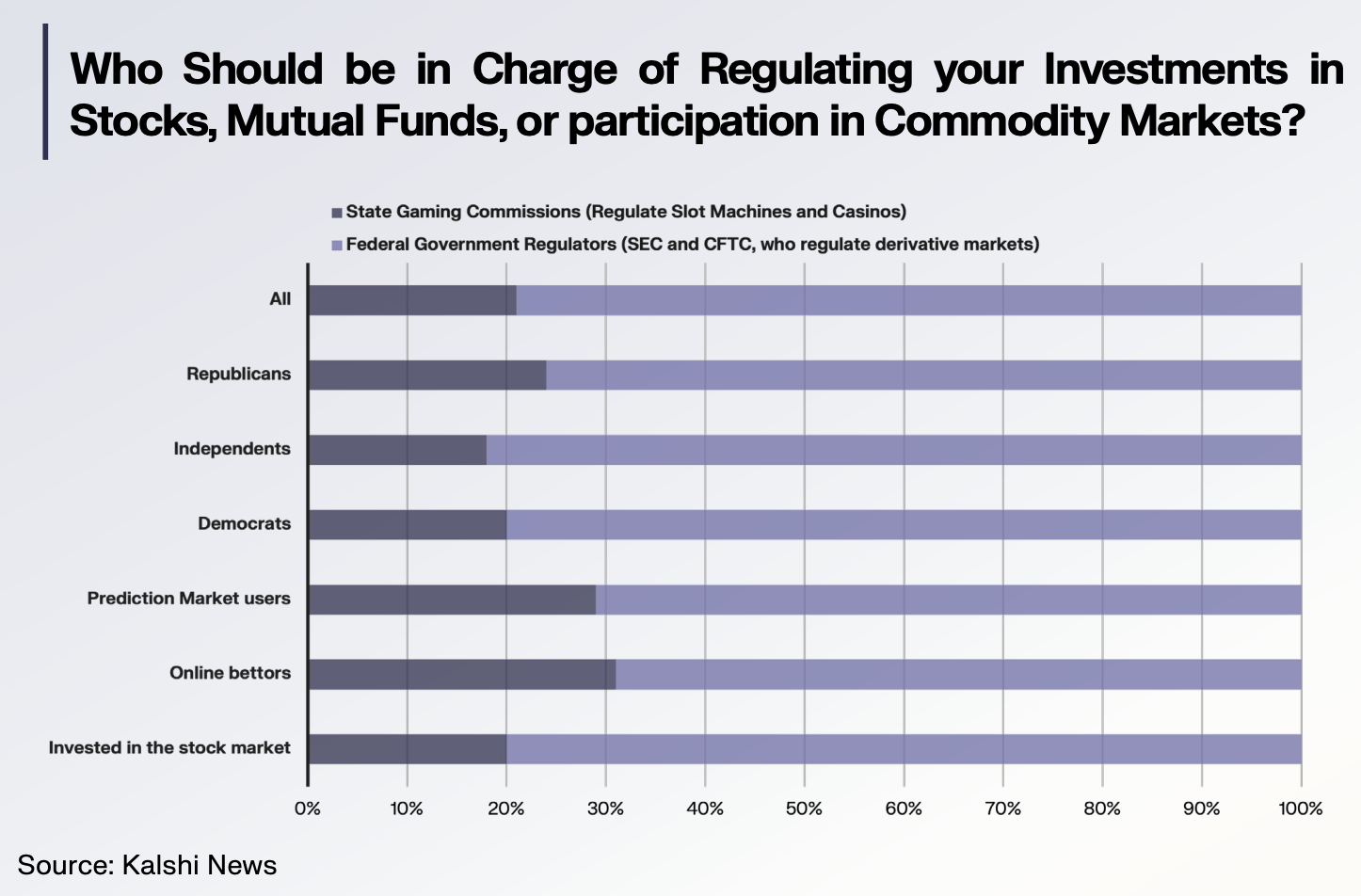

Public opinion data supports the financial instrument classification. When survey respondents are asked about stocks and commodity markets, they consistently choose SEC/CFTC oversight over state gaming commissions. People intuitively distinguish financial products from gambling. This intuition extends to prediction markets — trading a contract on an election outcome or GDP number feels structurally different from placing a bet at a casino, even if the mathematical mechanics share surface similarities.

The trust dimension adds another layer. Only 31% of U.S. adults trust news media, according to recent surveys. Prediction markets fill this deficit by providing financially-backed probability estimates that carry more credibility than editorial opinions or poll averages. Classifying them as gambling — and restricting access accordingly — would eliminate one of the few information sources the public increasingly trusts.

Three Branches, Three Risks

Even with the Kalshi precedent in place, risks remain from all three branches of U.S. government. Duncan Hennes of KPMG outlined this framework in the Keyrock research:

Executive Risk: CFTC Discretion

The CFTC retains executive authority to prohibit specific categories of event contracts. The Kalshi ruling constrains the agency’s ability to block political contracts, but it could still move against other categories — most notably, sports-related event contracts that overlap with traditional sports betting. The boundary between a “sports event contract” and a “sports bet” remains undefined. How the CFTC draws that line will shape the market’s next major expansion or restriction.

Judicial Risk: State and Tribal Claims

States and tribal gaming authorities may challenge the federal classification. Their argument: event contracts constitute gaming under state law, regardless of the CFTC’s position. This creates jurisdictional conflict — a product that is a regulated financial instrument federally could simultaneously be an illegal gambling product under state law. Resolution will likely require additional court rulings or federal preemption. Both are slow, uncertain processes.

Legislative Risk: Congressional Amendment

Congress retains the power to amend the Commodity Exchange Act itself. If political pressure builds — from the gaming industry viewing prediction markets as competitive threats, or advocacy groups concerned about election-related trading — lawmakers could explicitly reclassify event contracts or impose new restrictions. This is the most unpredictable risk because it depends on political dynamics, not legal interpretation.

The Global Dimension: Permissionless Markets and Foreign Regulators

The regulatory question extends well beyond the United States. As Stefan George observed, the long-term vision involves permissionless global access — markets anyone, anywhere can participate in, without geographic restrictions or centralised gatekeepers. Blockchain makes this technically feasible. Legally, it is another matter entirely.

The next phase involves state governments establishing frameworks, foreign regulators classifying event contracts within their jurisdictions. European regulators, Asian financial authorities, emerging market governments — each will reach their own conclusions. The result could be a fragmented landscape where a contract legal in one jurisdiction is prohibited in another.

The central question: do prediction markets become fully globally accessible — operating like foreign exchange markets that transcend national boundaries? Or do they fragment into jurisdiction-specific silos with different rules, different contracts, different access? Technology will not decide this. Regulation will.

Kalshi's Regulatory Advantage as a Designated Contract Market

Kalshi’s DCM registration gives it structural regulatory advantages that have shaped the competitive landscape. As a DCM, Kalshi operates under the same legal framework as the Chicago Mercantile Exchange. Segregated customer accounts. Regulatory reporting. Market surveillance. CFTC examination authority. All of which provide the institutional confidence that banks, asset managers, and corporate treasuries need before they can participate.

The DCM framework also creates a regulatory moat. Obtaining registration is a multi-year, capital-intensive process. This produces a two-tier market: regulated DCMs like Kalshi that can serve institutional and retail U.S. customers, and offshore or decentralised platforms that must navigate the grey zone or partner with regulated entities — as Polymarket did with QCEX.

What Comes Next for Prediction Market Regulation

The trajectory points toward gradual normalisation. But significant uncertainty remains at each step. Key developments to watch:

- Sports contract determination: Whether the CFTC permits or prohibits sports-related event contracts will define the next major expansion — or restriction — of the market.

- State-level action: Individual states may regulate or restrict access, creating patchwork compliance requirements similar to the current sports betting landscape.

- International frameworks: As prediction markets grow globally, foreign regulators will establish classification and oversight models, creating opportunities for regulatory arbitrage or cross-border fragmentation.

- Congressional attention: If volumes and public visibility continue to grow, Congressional hearings and potential legislative action become increasingly likely.

- Institutional adoption: As more institutional participants enter through regulated channels, the political constituency for maintaining the framework grows — making restrictive action less likely over time.

Prediction market regulation in 2026 is a work in progress. The foundation has been laid — the Kalshi ruling, the DCM framework, the Polymarket re-entry through QCEX. The superstructure remains under construction. Whether regulators, courts, and legislators continue to treat prediction markets as financial innovation — or push them back into the gaming classification that the 2024 ruling rejected — determines this sector’s trajectory for the decade ahead.

Frequently Asked Questions

Are prediction markets legal in the US?

Yes, with caveats. Kalshi operates as a CFTC-registered Designated Contract Market (DCM), making it fully legal for U.S. users. The 2024 court ruling established that political event contracts are not “gaming” under the Commodity Exchange Act. Polymarket re-entered the U.S. market in late 2025 through regulated infrastructure (QCEX) following a CFTC settlement. However, regulatory risks remain from state gaming authorities, CFTC discretion over specific contract categories, and potential Congressional action.

How does the CFTC regulate prediction markets?

The CFTC regulates prediction markets as event contracts under the Commodity Exchange Act. Platforms must register as Designated Contract Markets (DCMs) to legally list event contracts for U.S. customers. The CFTC has enforcement authority over unregistered platforms, as demonstrated by actions against InTrade (2012) and Polymarket. The agency retains discretion to prohibit specific contract categories and conducts market surveillance of registered exchanges.

Is Polymarket legal?

Polymarket settled with the CFTC for operating without registration and re-entered the U.S. market in late 2025 through QCEX, a regulated infrastructure partner. The platform continues to operate globally. Its legal status reflects the evolving regulatory landscape: initially non-compliant, then subject to enforcement, now operating through regulated channels. Verify current availability and compliance status in your jurisdiction.

What was the Kalshi court ruling about?

The 2024 Kalshi ruling is considered the single most important regulatory precedent in prediction market history. The court held that political event contracts — specifically, contracts on election outcomes — are not “gaming” under the Commodity Exchange Act. The key reasoning: if election trading were gambling, then weather derivatives, interest rate futures, and commodity futures would also be gambling, since they all involve financial stakes on uncertain future events. This precedent places prediction markets firmly within the financial regulation framework under CFTC jurisdiction.