Prediction Markets: The Next Frontier of Financial Markets

Polymarket vs Kalshi: Full Comparison of the Two Largest Prediction Markets (2026)

Two platforms dominate prediction markets. Together they capture the vast majority of global volume. But calling them competitors understates the gap between their philosophies.

Polymarket is crypto-native, decentralised, and global-first. Kalshi is regulation-first, centralised, and built for U.S. compliance from day one. Same product category. Radically different DNA.

We used real platform data from 2025 to cut through the noise. Here is what we found.

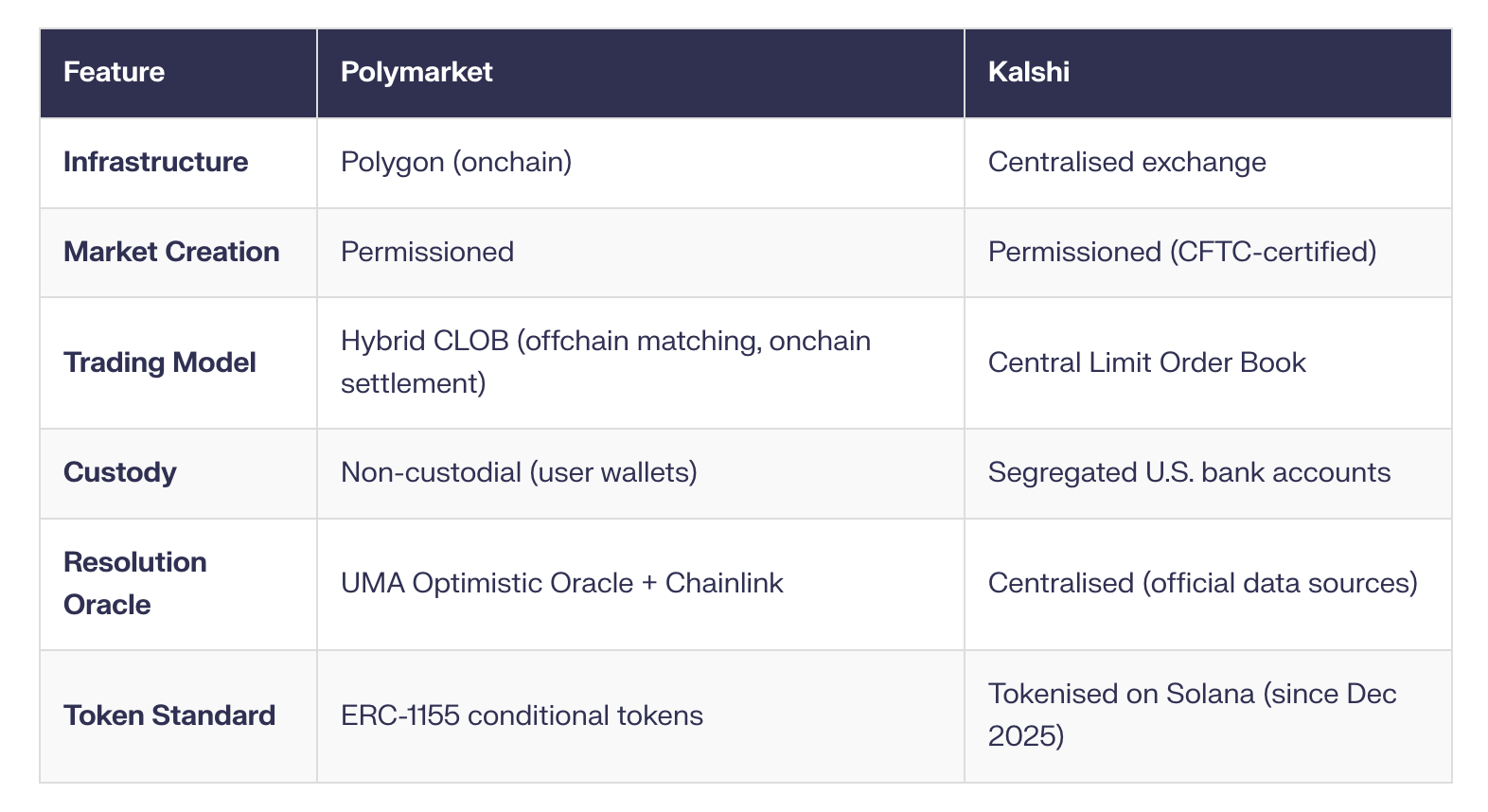

Architecture: Onchain vs. Centralised

Polymarket runs on the Gnosis Conditional Token Framework. Each Yes/No outcome becomes a fungible ERC-1155 token. It shifted from an AMM model to a CLOB in 2022 — offchain order matching for speed, onchain settlement for transparency.

Kalshi built a fully centralised stack, registered as a Designated Contract Market (DCM) under U.S. derivatives law. Every trade is fully collateralised and cleared through Kalshi Klear. In December 2025, Kalshi expanded by launching tokenised event contracts on Solana — bridging centralised regulation with onchain composability.

Different roads. Both heading toward institutional-grade infrastructure.

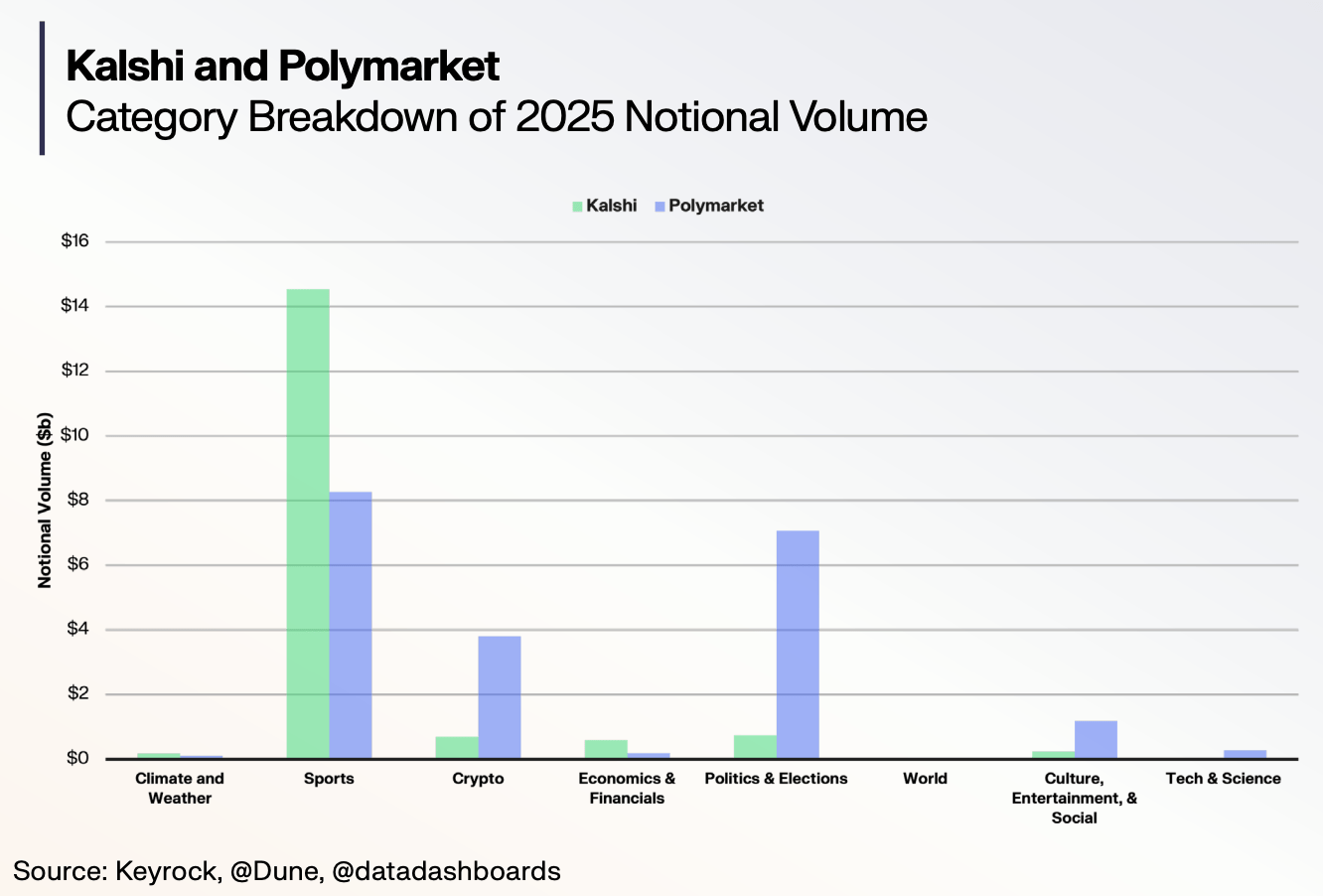

Volume and Market Share

Combined monthly notional volume regularly exceeded $13 billion in 2025. But the composition tells you who trades where — and why.`

- Kalshi: ~85% sports by volume, with crypto, economics, and politics each around 3–4%

- Polymarket: More diversified — sports (39%), politics (34%), crypto (18%), and other categories making up the balance

`

Kalshi’s CFTC status gave it a direct line to American retail sports fans. Polymarket, initially blocked in the U.S., built a crypto-native, globally distributed base drawn to politics and macro events.

But volume alone misleads. Open interest — capital that remains committed, not just traded — reveals a different picture.

On Kalshi, politics, elections, and economics combined hold 2.5x the open interest of sports throughout 2025. On Polymarket, politics has led sports in open interest every single day of 2025 by an average of 400%.

Sports drive volume. Conviction sits elsewhere.

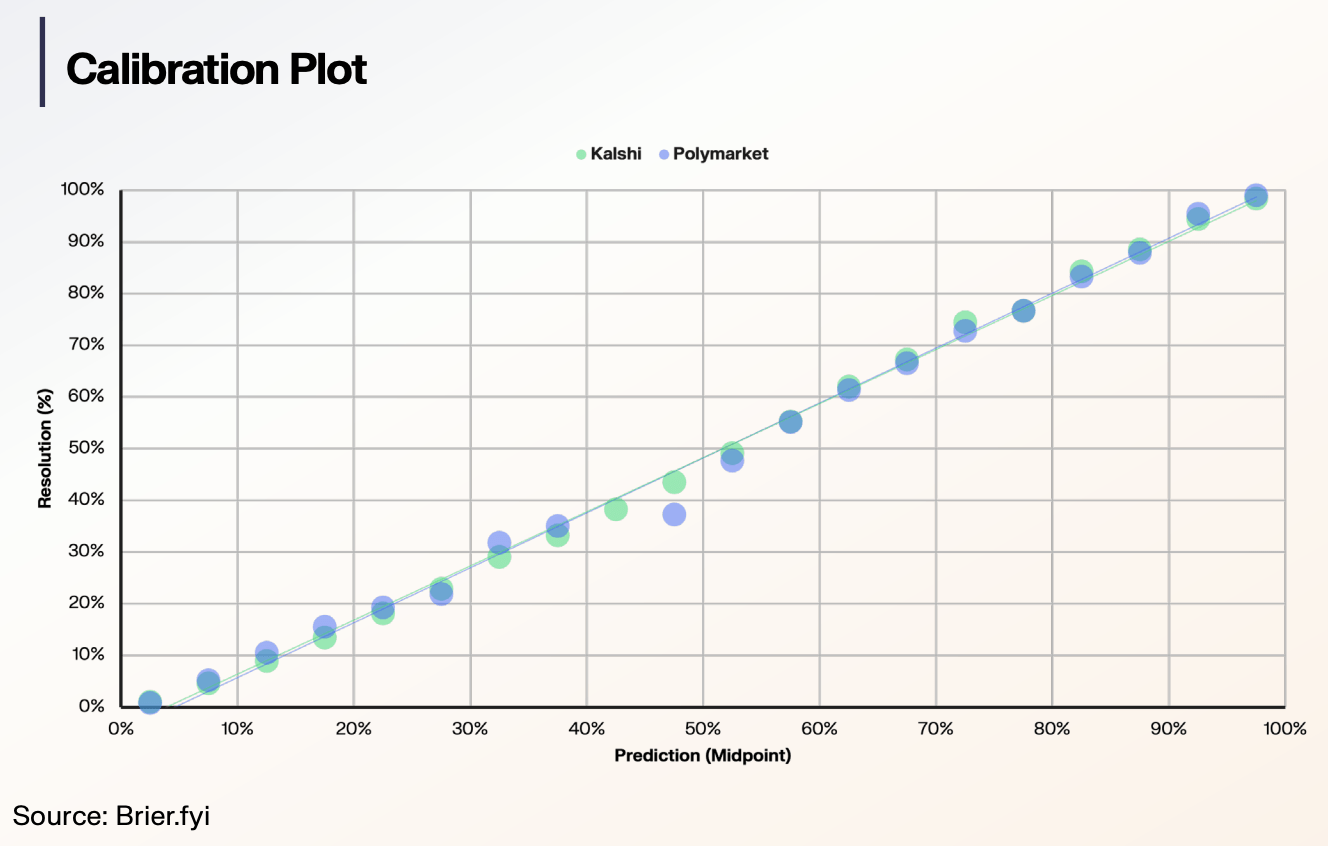

Accuracy and Calibration

Both platforms deliver strong predictive performance. Both achieve Brier scores near 0.09 across thousands of resolved contracts. The differences lie in distribution.

- Kalshi’s distribution is tighter — most markets fall well below 0.10, reflecting standardised, CFTC-certified contract design

- Polymarket’s distribution is broader — a consequence of wider market variety that introduces more variance

- On both platforms, higher traded volume consistently correlates with lower Brier scores — more liquidity, more accuracy

Kalshi’s forecasting error remains near zero in the final days before resolution. Even 200 days out, Kalshi’s forecasts outperform expert surveys, weather models, and sports betting markets.

Fees

Polymarket launched in the U.S. with a 0.01% fee on taker orders. Maker orders are free and earn LP rewards — over $12 million paid out to liquidity providers to date.

Kalshi’s fees vary by contract price. For long-shot bets, Kalshi can be slightly more expensive. For outcomes with implied probability above 30%, Kalshi provides better value once all costs are accounted for.

Both platforms crush sportsbooks on value. Across 5,000+ identical markets, Kalshi and Polymarket offer 77% better odds on average than traditional sportsbooks. The exchange model wins — convincingly.

Regulation

This is where the platforms diverge most sharply.`

- Kalshi spent years building compliant infrastructure before launching a single product. It is a CFTC-registered Designated Contract Market. In 2024, a landmark court ruling on Kalshi’s case affirmed that political event contracts are legitimate financial instruments, not gambling — the most important regulatory precedent in prediction market history.

- Polymarket initially operated in a regulatory grey zone, settled with the CFTC in 2022, and re-entered the U.S. in late 2025 through its acquisition of QCEX, a regulated exchange and clearinghouse.

Both are now in the regulated arena. They got there by very different paths.

Ecosystem and Partnerships

Polymarket scaled distribution aggressively in 2025: Google Finance and Yahoo Finance integration, UFC partnership for in-arena odds, X (Twitter) integration with real-time odds, MetaMask in-wallet trading, and a Builders Programme that has produced specialised interfaces generating over $150 million in routed volume.

Kalshi built partnerships with the NHL, CNN, CNBC, and Robinhood (FCM integration reaching tens of millions of retail users), plus Jupiter Exchange on Solana. Kalshi has expanded to 140+ countries and positions itself as a global liquidity layer for prediction markets.

Which Should You Choose?

Choose Polymarket if you want crypto-native, non-custodial trading; you are drawn to politics, crypto, and macro events; you value onchain transparency and DeFi composability.

Choose Kalshi if you want a fully regulated U.S. exchange with CFTC oversight; you prefer funds in segregated bank accounts; you trade primarily sports or economic indicators; you value standardised, certified contracts.

Many serious traders use both. Different markets, different liquidity pools, sometimes different odds on the same event. There is no reason to pick just one.

Frequently Asked Questions

Can I use both Polymarket and Kalshi?

Yes. Many traders use both platforms since they offer different market categories, liquidity pools, and sometimes different odds on the same event. Kalshi requires KYC as a regulated exchange. Polymarket requires KYC for U.S. users following its re-entry.

Which platform has more accurate predictions?

Both achieve Brier scores around 0.09. Kalshi’s standardised contracts produce tighter error distributions, while Polymarket’s broader market variety introduces higher variance. Accuracy improves with liquidity on both platforms.

Are prediction markets on these platforms the same as gambling?

No. A 2024 federal court ruling explicitly affirmed that event contracts are not “gaming” under the Commodity Exchange Act. Both platforms operate as exchanges matching buyers and sellers — not as a house taking the opposite side of your position.