Onchain Asset Management: Designing the Future of Investment Strategies

Onchain Structured Products: Pendle, Aevo, and Yield Tokenization

Investment banks have built trillion-dollar businesses packaging yield into structured products. Fixed-rate notes. Principal-protected instruments. Leveraged exposure. Complex payoff profiles accessible only to institutional buyers with seven-figure minimums.

Now Pendle and Aevo replicate those economics onchain. Permissionless. Transparent. Available to any wallet. The structured products market is being rebuilt from first principles on programmable infrastructure.

What Onchain Structured Products Actually Are

A structured product combines multiple financial components to create a specific risk-return profile. In traditional finance, an investment bank assembles these from bonds, derivatives, and interest rate swaps. The complexity is the point — it justifies the fee.

Onchain structured products achieve the same outcomes through composable DeFi primitives:

- Yield tokenisation — splitting a yield-bearing asset into its principal component and its yield component, each tradeable independently

- Options and derivatives — creating leveraged exposure, hedging instruments, and defined-outcome products via smart contracts

- Fixed-rate construction — locking in yields by trading future yield streams at present value

- Principal protection — structuring products where the downside is bounded while upside remains open

Same financial engineering. Different rails. No intermediary extracting 2–5% for assembly.

Pendle: The Yield Tokenisation Protocol

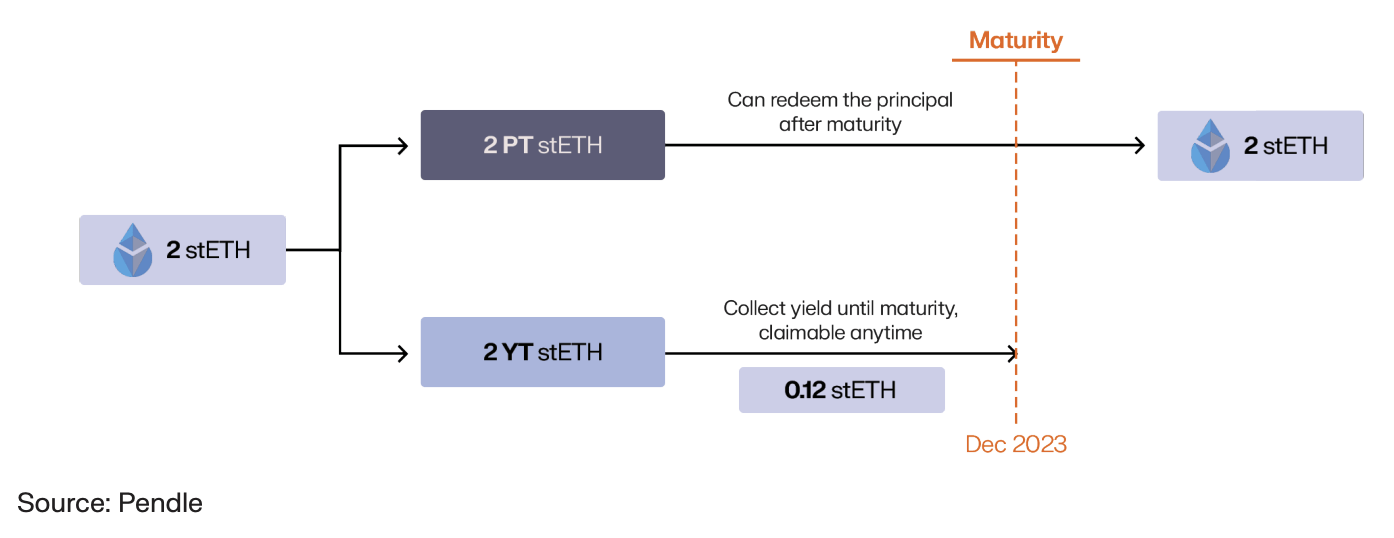

Pendle splits yield-bearing tokens into two components: Principal Tokens (PT) and Yield Tokens (YT). This separation unlocks strategies impossible with the underlying asset alone.

How it works:

- Deposit a yield-bearing asset (staked ETH, lending positions, vault shares)

- Pendle mints a PT (representing your principal at maturity) and a YT (representing all yield earned until maturity)

- Trade either component independently on Pendle’s AMM

The implications are profound:

- Buy PT — you effectively lock in a fixed yield to maturity. If current variable rates are 8% but PTs are priced to yield 6%, buying PT gives you guaranteed 6% regardless of rate movements.

- Buy YT — you take leveraged exposure to future yield. If rates rise above what the market priced in, YT holders capture the excess.

- Sell YT, hold PT — monetise future yield upfront while maintaining principal exposure. Cash flow management on steroids.

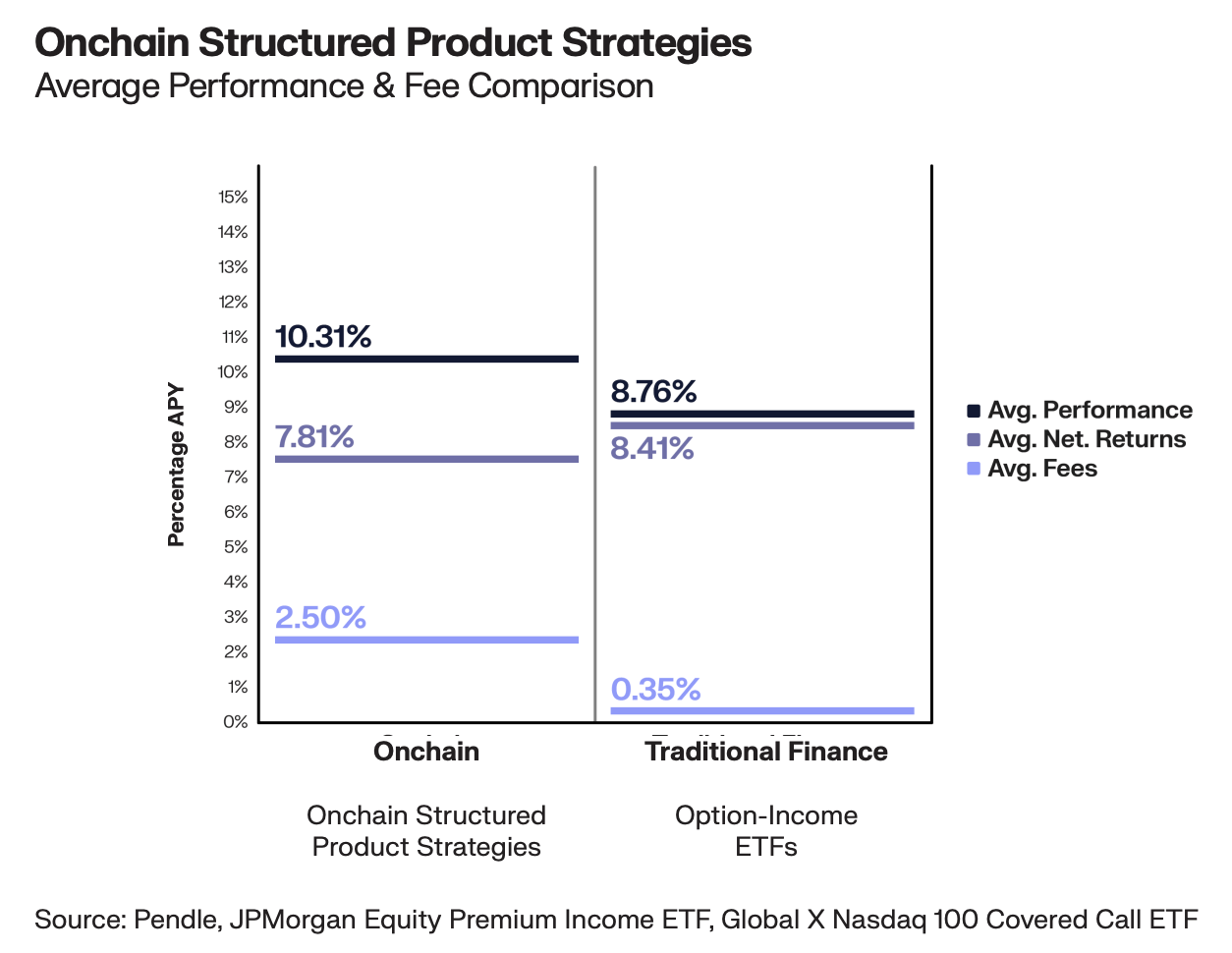

Pendle ranks among the top three protocols in onchain asset management alongside Morpho and Maple. The three together account for 31% of the $35 billion in total AUM. That concentration reflects product-market fit: yield tokenisation solves a real problem for real allocators.

Aevo: Onchain Options and Derivatives

Aevo builds the options and structured derivatives layer. Where Pendle tokenises yield, Aevo enables complex payoff profiles through option strategies, perpetuals, and custom structures.

The platform allows traders to:

- Buy and sell options on crypto assets with defined risk parameters

- Construct covered calls, protective puts, and spreads

- Access pre-packaged structured products with specific risk-return profiles

- Trade with onchain settlement and transparent pricing

Traditional structured notes from investment banks carry embedded fees of 2–5% that investors rarely see. Aevo’s transparent pricing exposes the full cost structure. When you can see every component’s mark-to-market in real time, overpriced products cannot survive

Use Cases: Who Needs Structured Products Onchain

Structured products serve specific allocator needs that simple yield or directional exposure cannot:

Fixed-Rate Seekers

Treasury managers and institutions that need predictable returns. Variable DeFi yields fluctuate — sometimes violently. Buying Pendle PTs locks in a rate. Budget certainty. No surprises.

Yield Speculators

Traders who believe rates will rise buy Pendle YTs for leveraged exposure. If staking yields jump from 4% to 8%, YT holders capture multiples of that increase relative to their capital deployed.

Hedgers

Protocols holding large yield-bearing positions can sell YTs to lock in current rates, protecting against rate compression. DAOs use this to stabilise treasury revenue.

Income Harvesters

Selling covered calls via Aevo on existing crypto holdings generates additional income. The structured payoff — capped upside in exchange for premium — mirrors exactly what institutions do in traditional markets.

Performance and Capital Flows

Structured products represent a growing but smaller category within the $35 billion onchain ecosystem. Their share is expanding as:

- More yield-bearing assets become available for tokenisation

- Institutional allocators seek fixed-rate exposure onchain

- Composability with other DeFi protocols creates new structuring opportunities

- The maturation of options markets enables more complex payoff profiles

Capital concentration patterns hold here too. Whales and dolphins supply the majority of liquidity in structured product markets. The complexity of these instruments naturally attracts more sophisticated allocators who understand the mechanics and can price the embedded optionality.

Composability: The Multiplier Effect

Structured products do not exist in isolation. They compose with every other DeFi primitive.

Pendle PTs can serve as collateral in lending markets like Morpho. Aevo positions can be used as margin for other trades. Vault shares from automated yield strategies flow into Pendle for yield splitting. Each integration creates new structuring possibilities that did not previously exist.

This composability is the moat. Traditional structured products are siloed. Each bank’s products live in isolation. Onchain structured products plug into a global, permissionless financial stack where every component interoperates by default.

The result: a combinatorial explosion of possible structures. Every new protocol, every new yield-bearing token, every new collateral type multiplies the design space available to structurers.

Comparison with Traditional Structured Notes

Traditional structured notes — the investment bank products sold to private wealth clients — share the same economic logic but differ on every operational dimension:

- Minimum investment — traditional: $100,000–$1,000,000. Onchain: no minimum.

- Transparency — traditional: embedded fees hidden in the term sheet. Onchain: every component priced live on a public AMM.

- Liquidity — traditional: hold to maturity or sell back to the issuing bank at their price. Onchain: trade on secondary markets at any time.

- Customisation — traditional: choose from the bank’s menu. Onchain: compose any combination of primitives permissionlessly.

- Counterparty risk — traditional: you rely on the bank’s creditworthiness. Onchain: smart contract execution with no counterparty.

The structural comparison is consistent across every dimension: lower cost, greater transparency, better liquidity, broader access.

Risks Specific to Structured Products

Complexity amplifies certain risks:

- Smart contract risk compounds — structured products stack multiple protocols. A vulnerability in any layer affects the whole structure.

- Pricing risk — AMM-based pricing for PTs and YTs depends on market depth. In thin markets, prices can deviate significantly from fair value.

- Maturity risk — PTs have defined maturities. If you need to exit early, secondary market liquidity determines your realised price.

- Complexity risk — the permissionless nature means anyone can create structures. Not all structures are economically sound.

These risks are manageable for informed allocators. But they underscore why whales and dolphins dominate: understanding structured products requires financial sophistication that the composable building blocks alone do not teach.

What Comes Next

The structured products frontier expands with every new yield-bearing asset that arrives onchain. As tokenised treasuries, bonds, and real-world assets grow, each becomes raw material for yield tokenisation via Pendle or structured payoffs via Aevo.

The $64 billion forecast for end-2026 includes significant growth in structured products. The catalyst: institutional capital seeking fixed-rate exposure and defined-outcome products that traditional DeFi yields alone cannot provide.

We are watching investment banking’s product manufacturing capability get rebuilt — permissionlessly — onchain.

Frequently Asked Questions

What are onchain structured products?

Onchain structured products combine DeFi primitives to create specific risk-return profiles. They include yield tokenisation (splitting yield-bearing assets into principal and yield components), options strategies, fixed-rate instruments, and leveraged exposure. Protocols like Pendle and Aevo enable permissionless creation and trading of these products without intermediaries.

How does Pendle yield tokenisation work?

Pendle splits yield-bearing tokens into Principal Tokens (PT) and Yield Tokens (YT). PTs represent principal redeemable at maturity, effectively offering fixed-rate exposure. YTs represent all yield earned until maturity, offering leveraged exposure to rate movements. Both trade independently on Pendle’s AMM, enabling fixed-rate locking, yield speculation, and cash flow management.

Are onchain structured products safe?

They carry compounded smart contract risk (multiple protocol layers), pricing risk (AMM liquidity-dependent), maturity risk (early exit depends on secondary markets), and complexity risk (permissionless creation means not all structures are sound). However, all risks are transparent and auditable onchain. Institutional allocators dominate these markets, indicating sophisticated risk assessment.

How do onchain structured products compare to traditional structured notes?

Onchain structured products offer no minimums (vs $100K-$1M traditional), transparent pricing (vs hidden bank fees of 2-5%), secondary market liquidity (vs hold-to-maturity), permissionless customisation (vs bank menus), and no counterparty risk (vs bank credit dependence). Same economic logic, fundamentally different operational architecture.