Defining Onchain Structured Product Strategies

Structured products onchain are similar to the traditional form of structured products, in that, simply put, they’re products that package derivatives and yield strategies into defined payoff profiles. Typically, they utilise growing areas of DeFi such as options, futures or yield splits to create these structured exposures which could be covered calls, cash-secured puts, basis trades or Pendle-style fixed vs floating yield. As with their traditional counterparts, the purpose here is to provide capital allocators with the ability to take directional or volatility views, which could be betting on price stability, volatility, or steady yields, as opposed to merely taking a long or short view on price, with predefined risk and return characteristics.

In terms of where these products sit in the DeFi stack, we’re generally looking at protocols spread across two layers, those which are standalone financial instruments, such as options protocols like Aevo, Lyra and Dopex, and those that manipulate existing DeFi instruments in a ‘DeFi Lego’ style protocol, such as yield tokenisation platforms like Pendle and Spectra. Either way, these protocols typically act as ‘end products’ at the top of the DeFi stack, pulling liquidity from base layers such as DEXs and lending protocols and then wrapping them into tailored exposures. As such, the entire product depends on liquidity pools, oracles and underlying asset exposure that spans the whole of onchain assets, ranging from LSTs to RWAs and stables.

History and Evolution of Onchain Structured Product Strategies

Structured products onchain trace their roots back to the earliest experiments with options protocols in 2020. Projects like Opyn and Hegic proved, albeit with limited liquidity, that options could be created and settled natively on Ethereum. Adoption for these protocols was, however, limited by clunky interfaces, shallow liquidity, and a lack of institutional interest. These early designs were important proof-of-concepts but fell short of providing a scalable framework for structured strategies.

The real breakthrough came in 2022 with the rise of automated options vaults. Ribbon Finance (now Aevo) and Dopex pioneered vaults that packaged strategies such as covered calls and cash-secured puts into accessible, automated products. For the first time, retail investors could participate in exposures that in traditional markets were reserved for accredited clients buying structured notes from investment banks. Capital flowed into these vaults during the bull market, though bear market volatility revealed shortcomings. These centered around vaults typically selling options too cheaply, leaving depositors exposed when markets moved aggressively. This triggered an important wave of refinement in strategy design, including improved strike-selection algorithms, more conservative risk sizing, and better hedging mechanisms.

By 2024, structured products onchain had begun to mature. Pendle introduced yield tokenisation, splitting principal and yield into separate assets, which allowed investors to trade fixed versus floating yield exposures. This marked a fundamental shift in which structured products were no longer static, single-purpose instruments, but instead liquid, composable building blocks that could be rehypothecated across DeFi. Suddenly, a vault position could serve as collateral, be traded in secondary markets, or be plugged into entirely new strategies. Pendle’s model in particular gained traction in stablecoin and liquid staking markets, where secondary liquidity created a thriving market for structured yield.

DAOs began using structured vaults as treasury tools, allocating governance capital into covered call or basis trade strategies to generate delta-neutral income. At the same time, regulatory clarity attracted the first wave of institutional pilots, with banks and funds testing tokenised structured products under compliant, sometimes whitelisted, frameworks.

Today, structured products stand as one of the most polarising categories within onchain asset management. On the one hand, you have tokenised yield, which has found product-market-fit and has accumulated a wealth of AUM. On the other hand, you have an underdeveloped options and other structured products industry onchain that’s nascent and yet to establish a meaningful user base.

This article is a part of a series on Onchain Asset Management.

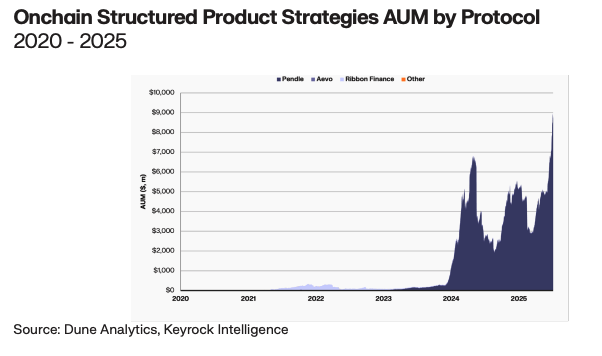

Pendle Dominance: The AUM Growth of Onchain Structured Product Strategies

Onchain structured products AUM is slightly varied from the other strategies we’ve been assessing, in that it’s been accelerating since 2024, as opposed to standalone resurgence in 2025, and it’s dominated by one player. The overwhelming driver of this growth has been Pendle, which has effectively cornered the market by standardising the mechanics of principal and yield token splits. This simplicity, combined with liquid secondary markets and integrations with yield-bearing assets like Ethena’s sUSDe, has created a feedback loop that continues to draw capital.

By contrast, protocols that tried to build around options vaults or derivatives, such as Ribbon Finance and Aevo, have struggled to sustain traction. Their products have faced liquidity fragmentation, high implied volatility, and user fatigue with strategies that failed to consistently outperform. The result is an imbalance in which the concentration underscores both the strength of Pendle’s model and the difficulty of scaling more complex onchain options strategies, a gap that remains an open question for the future evolution of this segment.

Comparing Onchain Structured Product Strategies to Traditional Finance Counterparts

Onchain structured products are designed to provide more complex financial products that go beyond simple lending or staking, by constructing yield or payoff profiles, often combining options, swaps, or fixed maturities into packaged vault strategies. The primary purpose of these onchain instruments is to enhance yield, hedge exposure, or create customised risk-return profiles in a way that is accessible and automated for onchain users. These strategies can take the form of covered call vaults, principal-protected note structures, or tokenised payoff tokens that split fixed and variable yield streams.

Onchain structured products earn yield through the tokenisation of future yield streams or by selling crypto option premia, e.g., splitting principal and yield tokens on Pendle or rolling covered call vaults. What’s important to note about their traditional finance counterparts is that structured products generally mean different things to different people depending on their focus within the industry. That said, structured products generally harvest yield from option-writing strategies on equities, while structured notes package derivatives into fixed coupons or payoff profiles sold via banks. This is the framing we will use within this report.

To identify appropriate comparators, we looked across traditional finance structured yield products. Potential peers include option-income exchange-traded funds (OIFs), structured notes offered by investment banks (SNs) and principal-protected products (PPPs). Each of these instruments shares the same underlying mandate as onchain structured products, but they differ in execution.

| Potential Comparator | Comparative Relevance | Comparative Shortcomings | Overall Suitability |

| Option-Income ETFs (OIFs) | Both use derivatives to generate additional yield on top of a core asset. Return drivers are similar in that they’re option premia. | ETFs operate on listed equities with regulated custodians, while onchain vaults run fully automated option sales in crypto markets. | Primary comparator |

| Structured Notes offered by IBs (SNs) | They package derivatives into payoff profiles (e.g., yield-enhanced notes, principal-protected). | Typically bespoke, issued via dealers, and illiquid. Onchain vaults are permissionless, liquid, and composable. | Secondary comparator |

| Principal-Protected Products (PPPs) | Similar to principal-protected structured vaults emerging onchain, combining a safe yield with optional upside exposure. | Traditional products use bonds and options in offchain markets. Onchain versions replicate via stable lending and tokenised options. | Less reasonable comparator |

For onchain structured products, the primary comparator is OIFs, as both strategies share a common goal of systematically enhancing yield through option premium collection. Examples of OIFs include covered call ETFs and similar wrappers, which represent mature, liquid traditional financial products. Onchain structured vaults such as Pendle operate in much the same way, in that they package derivative exposures into investable tokens. The parallels are rooted in the economic function of yield enhancement, cash flow mechanics driven by option premiums, and relative liquidity in secondary trading, albeit in scope with relative to on and offchain depth of liquidity. The key divergence, however, is in the underlying asset base. ETFs are built on equities, while onchain vaults derive their returns from derivative products on digital assets, primarily stablecoins and liquid staked assets.

A secondary comparator is SNs, which more closely capture the bespoke payoff element of many of the onchain products offered today. Whereas OIFs focus on a systematic overlay, SNs in traditional finance often combine fixed income instruments with derivative overlays to deliver principal protection or leveraged upside. Onchain equivalents, particularly Pendle’s Principal Tokens, function similarly by splitting and packaging yield streams into custom payoff profiles. The differences, though, are that SNs are dealer-distributed, illiquid, and largely opaque, while onchain tokens are permissionless, liquid, and composable across DeFi.

OIFs provide the best benchmark for yield-driven strategies. As such, OIFs will be compared with onchain structured product strategies by leveraging weighted averages for fee and performance comparisons, in conjunction with qualitative assessment.

Benefits and Drawbacks of Onchain Structured Product Strategies

Onchain structured products generally mirror their traditional finance counterparts in form, but diverge sharply in function, offering a suite of advantages that reflect the unique properties of decentralised infrastructure. Transparency, as with other strategies, is a key advantage here. Whereas traditional structured notes typically disclose only the payoff formula, obscuring collateral allocations and counterparty risks, onchain equivalents provide real-time, block-by-block visibility into collateral, positions, and performance. This radical transparency allows allocators to scrutinise exposures in a way that is structurally impossible in traditional markets, and is an immediate value add in an asset class often criticised for its opacity.

Liquidity and composability also set onchain structured products apart. In traditional finance, most structured notes are illiquid until expiry, barring some relatively illiquid secondary markets on select products, offering investors little flexibility once a position is taken. Onchain, composability is built in, ensuring that positions can be unwound or traded dynamically, often with continuous secondary market activity. The result is a far more flexible and adaptive product, where capital is not locked into static instruments but can instead be repositioned in response to market conditions.

Programmability further enhances efficiency. Smart contracts execute payoff structures and settle options atomically, eliminating counterparty dependency and removing the layers of manual execution and reconciliation that characterise traditional bank desks. In doing so, onchain products collapse settlement cycles from days to seconds, while providing complete auditability of all positions and returns. For allocators, this ensures not only greater efficiency, but also far lower costs compared to heavily intermediated traditional structures.

Moreover, onchain, payoff tokens, in which I am referring to tokenised yield components, can be rehypothecated across a variety of DeFi protocols, such as borrowing stablecoins against them to loop further exposure into the strategy, LPing them into DEX liquidity pools, or staking them in other vaults. This composability turns onchain structured products into liquid ‘DeFi Lego’ blocks, rather than terminal instruments for static hedging or exposure. The result is one of capital efficiency, in which investors can hold and redeploy exposure simultaneously. A tangible example would be depositing sUSDe into Pendle, and receiving PT-sUSDe and YT-sUSDe. You could then sell the PT to lock in fixed yield upfront, while simultaneously LPing the YT-sUSDe in Pendle’s own AMM. This allows you to speculate on yield upside and collect trading fees and incentives from the YT pool, turning a single yield-bearing token into multiple income streams.

While structured products onchain have opened new opportunities for tokenised yield trading, there remain clear drawbacks relative to their traditional finance equivalents. One of the most significant is the issue of market depth and liquidity. Onchain options markets are still shallow compared to equity or FX options in traditional finance, limiting both the range of strikes and maturities available. The result is wider spreads, higher slippage, and constrained position sizing for onchain allocators. For institutional allocators, this creates practical barriers to deploying capital at scale, in stark contrast to traditional alternatives that benefit from deep and mature liquidity pools.

Another drawback is the narrow maturity and instrument set currently available onchain. Pendle and similar protocols focus on short-dated maturities, typically ranging from 21 to 84 days, with a relatively standardised payoff structure based on yield tokenisation. Structured notes in traditional finance can span months to years and offer a broad menu of payoffs, such as barriers, autocallables, and capital-protected notes. This difference leaves onchain products more tactical in nature, rather than strategic allocation tools for long-term portfolio construction.

Risk management infrastructure is also less developed onchain. Whereas banks issuing structured notes run full hedging desks, with balance sheet support, counterparty risk management, and compliance oversight, onchain protocols rely almost entirely on smart contracts to enforce payoffs. This is the infrastructure that underpins the efficiencies we hailed as a benefit to onchain structured products, but it also removes the layers of risk mitigation and institutional oversight that traditional allocators are accustomed to.

Onchain Structured Product Strategies Fees and Performance

For the analysis of onchain structured products, according to our comparative analysis in prior sub-sections, we will be comparing against Option-Income ETFs.

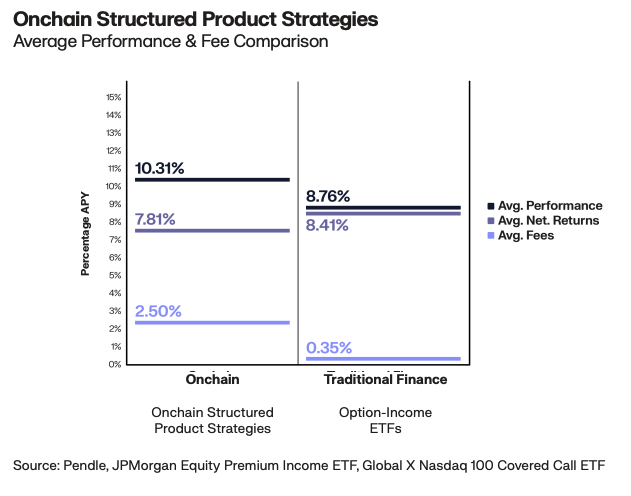

Onchain structured products delivered a weighted-average gross return of 10.31%, compared to 8.76% for their traditional peers. Within DeFi, Pendle vaults highlight both the innovation and dispersion, with the sUSDe 69-day maturity vault, managing over $736 million, posting 8.24%, while vaults such as the vkHYPE 55-days maturity vault and pUSDe 27-days maturity vault reached 13.10% and 13.32% respectively. Traditional benchmarks such as the JPMorgan Equity Premium Income ETF, which at $41 billion AUM is one of the largest option-income funds globally, generated 8.40%. Meanwhile, newer entrants like the Nasdaq-100 High Income ETF returned 12.19% on $4.7 billion, showing that traditional finance can also capture elevated yields during periods of high equity volatility. The comparison underscores the advantage onchain products have in dynamically harvesting short-dated volatility premia across assets, while traditional finance products scale to tens of billions with more muted but stable outcomes.

The most visible trade-off for onchain structured products comes from fees. DeFi vaults averaged 2.50%, compared to just 0.35% for the traditional benchmarks. The higher cost reflects the complexity of structuring, rolling expiries, and managing liquidity pools onchain, whereas option-income ETFs benefit from economies of scale and efficient execution pipelines. In effect, DeFi allocators are paying a premium for composability, transparency, and flexibility, while ETFs deliver a similar economic function at far lower cost.

Once fees are accounted for, the balance shifts slightly, with onchain structured products netting 7.81%, while traditional funds returned 8.41%. This suggests that, at present, traditional finance products offer a more competitive balance of yield and cost efficiency. However, onchain strategies remain differentiated by structural features, with real-time transparency into collateral and performance, permissionless access, and composability. Investors can rehypothecate PTs and YTs across DeFi, using them as collateral, trading them in AMMs, or layering additional yield strategies, something unimaginable with static, dealer-issued notes or ETFs.

Looking forward, as DeFi options markets deepen and protocols refine liquidity design, we expect gross yields to remain attractive relative to TradFi benchmarks. The question is whether fee compression and scale can close the net gap. For allocators, this remains a frontier category, in that it is structurally riskier and smaller in scale than ETFs, but uniquely enabled by the programmability of DeFi.

Allocator Profiles to Onchain Structured Product Strategies

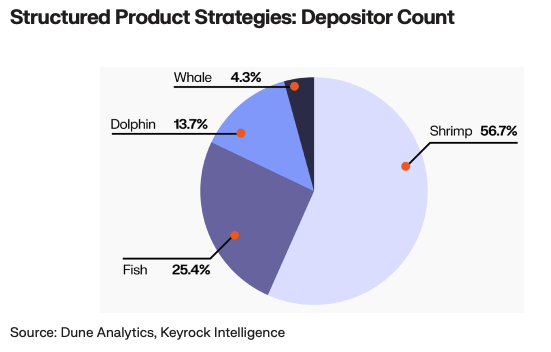

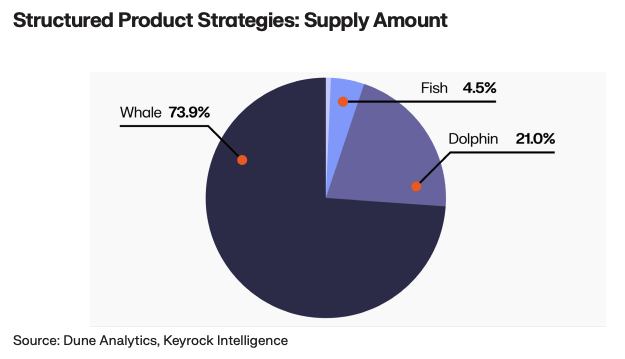

While in transitional finance these types of products are typically considered advanced, and thus are gatekept to professional investors, in DeFi these products are accessible to all in a permissionless format. In line with this, there is a more sophisticated education system designed for retail investors, which has led to a greater cohort of retail investors leveraging the sophisticated products to enhance returns. This is evident in the depositor count, which shows a skew towards smaller depositors, referred to as Shrimp, who’ve deposited under $10k per transaction, at 57% of address count.

As with all strategies analysed, however, we see that when looking through the lens of capital deployed, there’s a heavy skew towards larger allocators, with Whales, those deploying over $1 million per transaction, accounting for 74% of AUM. DAO treasuries and other large pools of capital will typically utilise structured products to construct delta-neutral products, more aligned with their capital preservation strategies.

Catalysts for Onchain Structured Product Strategies Growth

Structured products have benefitted from a wave of innovation over the past two years that has transformed them from experimental products to serious yield instruments. The most important catalyst has been the maturation of yield tokenisation, led by Pendle.

Looking forward, the payoff tokens mentioned previously, that can be rehypothecated across DeFi, staked as collateral, or layered into other vaults, are something that is impossible in traditional markets where payoff profiles are siloed within broker-dealer balance sheets. This ability to unbundle and recombine yield streams is already creating entirely new classes of strategies, and allocators are beginning to recognise the structural advantage. We believe the continued growth of composability avenues will drive growth in this strategy, with trust of onchain protocols and education being the bottlenecks that need to be addressed to fully unlock it’s potential.

Another driver is the growth of core components of structure products, LSTs, RWAs and stablecoins. Vaults that stack staking yield with options income, for example, create ‘yield-on-yield’ products that blend base-layer returns with derivative overlays. For allocators, these hybrid structures offer both a higher return ceiling and diversification of risk sources, without requiring constant rebalancing. This has proven particularly attractive to DAOs managing treasuries and to institutions seeking enhanced cash management tools that remain onchain.

Regulation is also moving in the right direction. The EU’s DLT Pilot Regime and Singapore’s Project Guardian both explicitly cover tokenised derivatives, providing a clearer legal pathway for structured payoffs to be created and traded onchain. In the U.S., the withdrawal of restrictive SEC staff statements has paved the way for broker-dealers to interact with tokenised options and structured notes under defined compliance frameworks. These developments reduce the perception gap that has long held institutions back, reframing structured products as increasingly legitimate.

Finally, the signalling effect of institutional involvement cannot be overstated. Market makers and Traditional Finance desks are beginning to backstop liquidity for Aevo and Katana vaults, committing balance sheet resources that reduce fragility and make allocators more confident in both execution and exit. Liquidity bootstrapping and secondary-market depth transform structured vaults from boutique products into scalable portfolio components. For institutions accustomed to opaque OTC structures with limited liquidity, the transparency and tradability of onchain alternatives is a compelling upgrade.

Together, these catalysts suggest that structured products are poised to move from the periphery of onchain experimentation into the core of institutional asset management.

Structured Products on Pendle

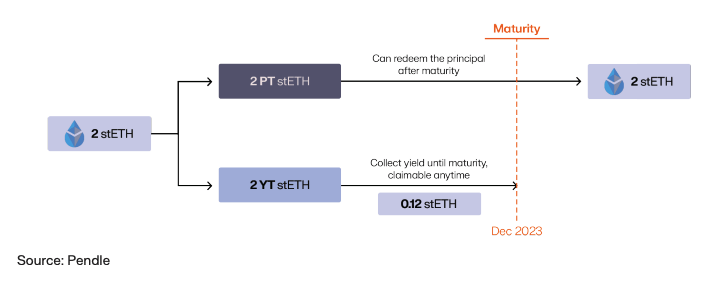

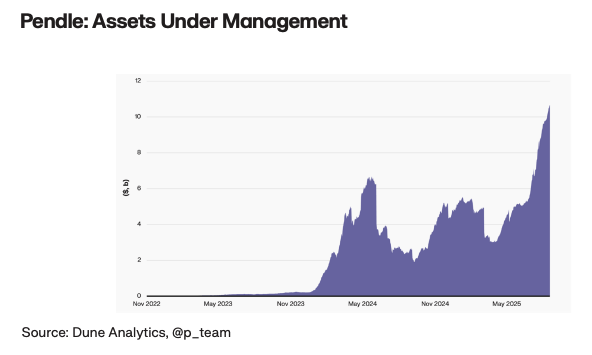

Pendle is the largest onchain structured products protocol, and has seen extraordinary growth, both in AUM, as well as across the assets and networks they facilitate. The premise is simple, it enables users to trade tokenised future yield by splitting a yield bearing onchain asset into two components, the Principal Token (PT), which represents the underlying asset, and the Yield Token (YT), which represents the future yield generated on the principal.

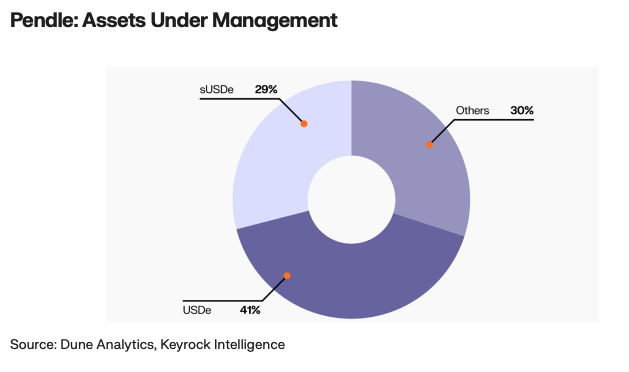

The mechanism for this onchain product is fairly simple, and given that Ethena, the yield-bearing synthetic dollar protocol, accounts for 70% of pendle’s $10.8 billion AUM, we’ll use Ethena’s sUSDe to explain it. The user deposits a unit of sUSDe into the Pendle protocol, specifying a network, which could be Ethereum, HyperEVM or Berachain, and a duration for which they want to split their yield-bearing token into PT and YT derivatives. The current duration options range from 21 to 84 days. Pendle then splits this sUSDe deposit into PT and YT derivatives, which are then returned to the user, both liquid and tradable on secondary markets as standalone assets.

The two tokens trade in slightly different ways, with varying purposes depending on the market participants. Let’s assume both assets are sold by the original depositor to lock in both the value of their underlying sUSDe, plus the yield they would have gained from staking it for the specified duration.

The PT will typically trade at a slight discount to the face value of the underlying asset, the price paid by the original depositor for the convenience of collecting their capital up-front. Therefore, if held to maturity, the purchaser of the PT will gain predictable, fixed yield, akin to a zero-coupon bond. If non-dollar pegged assets are deposited to Pendle, the PT also takes on the underlying asset price risk.

The YT is where the more complex trading strategies come in, by purchasing the yield at a specified rate from the original depositor, the purchaser is making a bet that the yield will be higher than the defined purchase yield, with a target to pocket the spread. This allows for speculation or hedging on future yield rates, similar to fixed income derivatives.

“In Traditional Finance, structured products are pre-packaged investments that combine bonds and derivatives to create a tailored payoff, say capital protection plus some equity upside.

Onchain, the logic is the same, but the packaging is done via smart contracts instead of banks or fund managers. For instance, a yield-bearing asset can be split into a “principal” portion and a “yield” portion, allowing them to be traded separately. That is essentially what Pendle enables.

These components can also be combined with options or used as collateral in money markets like Aave. This level of composability is unique to DeFi, where products can be mixed and integrated permissionlessly, unlike Traditional Finance where complex strategies are often limited to a small group of investors.” – DT, CEO at Pendle

What’s particularly special about Pendle isn’t the financial instruments that it creates, given we’ve seen these exist in traditional finance for decades, but rather the fact that Pendle has rebuilt these financial products in a way that’s open, programmable, and accessible to anyone, not just private banking clients.

Clearly, composability is a breakthrough here for onchain structured products, again in a way that is limited in traditional finance. With the ability to redeploy both PT and YT assets into DeFi, be that as collateral in Aave, or bundled into automated vaults, the onchain design results in significantly higher capital efficiency.

What’s interesting with structured products onchain is that there are some distinct similarities between customer base both onchain and offchain, as highlighted during our interview with Pendle, “while any user can technically build structured products, we’ve seen a pivot towards sophisticated players acting as curators for retail investors – akin to how it works in traditional markets.”

If we look to the future, and how structured products, with a particular focus here on Pendle, could shape onchain asset management, one key element to highlight is that PTs are strong contenders to be a driving ‘entry ramp’ for Traditional Finance allocators. Given PTs mimic zero-coupon bonds and offer predictable returns, these are derivatives traditional allocators are familiar with, that bare less risk and prior technical knowledge than alternative onchain products, “fixed yield instruments are likely to be the natural entry point for traditional allocators, given their familiarity with bond-like payoffs and their lower risk profile compared to variable yield.”

DT Lee, CEO of Pendle took this a step further, stating that, “composability remains an unexplored vertical. Hybrid onchain and offchain models could enable liquidity to move seamlessly between DeFi protocols and traditional institutions, positioning structured products as the bridge between the two systems.” In this future it’s possible that we see onchain yields decoupled from their underlying assets and ported between the two financial ecosystems, creating a new route to grow the onchain pie of capital.

Structured Products on Aevo (fka Ribbon Finance)

Aevo, formerly known as Ribbon Finance, is a decentralised options exchange, running on a custom EVM rollup. Alongside this, Aevo offers a variety of structured product strategies, as well as some non-structured product features such as a perpetual exchange. Note, for this report we’ll only focus on Aevo’s structured product offerings.

At their core, Aevo’s structured product offerings package options strategies into automated vaults, enabling users to access premia-based yield without the need to actively manage derivatives positions themselves.

Aevo’s covered call vaults allow depositors to earn yield by selling upside exposure on an underlying asset such as ETH. These vaults systematically write call options on the Aevo protocol, and distribute the premium as yield, mirroring the mechanics of popular options-income ETFs in traditional markets. Alongside these, Aevo also offers put-selling vaults, which generate return by underwriting downside risk through cash-secured puts, offering investors exposure to option premia in exchange for collateralising the vault with stablecoins or ETH.

In addition, Aevo has launched a basis trade vault, which captures spreads between spot and perpetual markets. By running a delta-neutral position, that is long spot against short perpetuals, the vault harvests funding rate premia that emerge from imbalances in perp markets.

While the products offered by Aevo are innovative and represent an exciting corner of onchain asset management, their adoption to date has been minimal. Growth has plateaued in part due to a lack of demand for the underlying options onchain, resulting from a bootstrapping issue in which onchain there are limited strikes and maturities, pushing demand offchain. This is evident both in the volume of Aevo’s onchain options, with BTC and ETH in the low hundreds of thousands of dollars a day, and in the underlying strategies AUM, with covered-call and selling-put strategies sitting at only a few million dollars a piece.