Onchain Asset Management: Designing the Future of Investment Strategies

Onchain Credit Strategies: Institutional Lending via Maple, Gondi

Credit is the backbone of traditional finance. Trillions in corporate loans, trade finance, and structured lending flow through banks, broker-dealers, and private credit funds. Now that backbone is being rebuilt onchain.

Protocols like Maple and Gondi power a new generation of credit strategies where underwriting, origination, and servicing happen on transparent, composable infrastructure. The capital is institutional. The returns are competitive. The architecture is fundamentally different.

How Onchain Credit Works

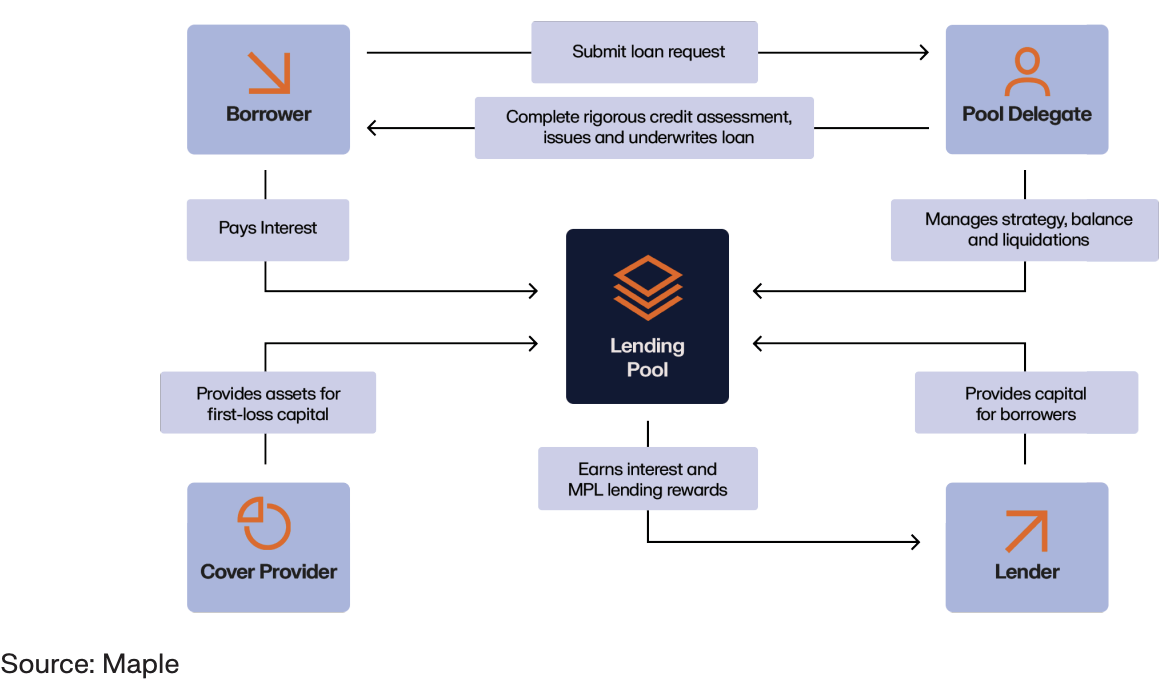

Onchain credit strategies connect lenders directly with vetted borrowers through smart contract-governed pools. The model strips out intermediaries that traditional lending chains require:

- Pool creation — a credit manager (like Maple or Gondi) establishes a lending pool with defined parameters: eligible borrowers, interest rates, collateral requirements, duration

- Capital deployment — lenders deposit stablecoins or other assets into the pool. Smart contracts manage the allocation.

- Underwriting — borrower assessment combines onchain reputation (historical behaviour, protocol activity) with off-chain due diligence by the pool manager

- Servicing — interest accrues automatically. Repayments are tracked onchain. Default triggers are codified in the contract.

No bank relationship manager. No weeks of documentation. No opaque committee decisions. Borrowers access capital faster. Lenders see exactly where their money sits.

The Players: Maple and Gondi

Maple Finance

Maple operates as a marketplace for institutional credit. Pool delegates — experienced credit professionals — curate lending pools, assess borrowers, and manage risk. The protocol handles the infrastructure: capital aggregation, interest distribution, and transparent reporting.

As Joe Flanagan of Maple puts it, the protocol bridges the gap between institutional-grade underwriting and the efficiency of blockchain-native infrastructure. Borrowers range from crypto-native market makers to traditional corporates seeking faster capital access.

Maple sits among the top three protocols in onchain asset management, alongside Morpho and Pendle. Together they represent 31% of all onchain AUM.

Gondi

Gondi focuses on secured lending. Borrowers post collateral — typically NFTs or other onchain assets — and lenders earn yield backed by tangible security. The model resembles asset-based lending in traditional finance, but with instant origination and transparent collateral monitoring.

Where Maple serves unsecured or partially secured institutional credit, Gondi occupies the secured niche. Different risk profile. Different return characteristics. Both powered by the same programmable infrastructure.

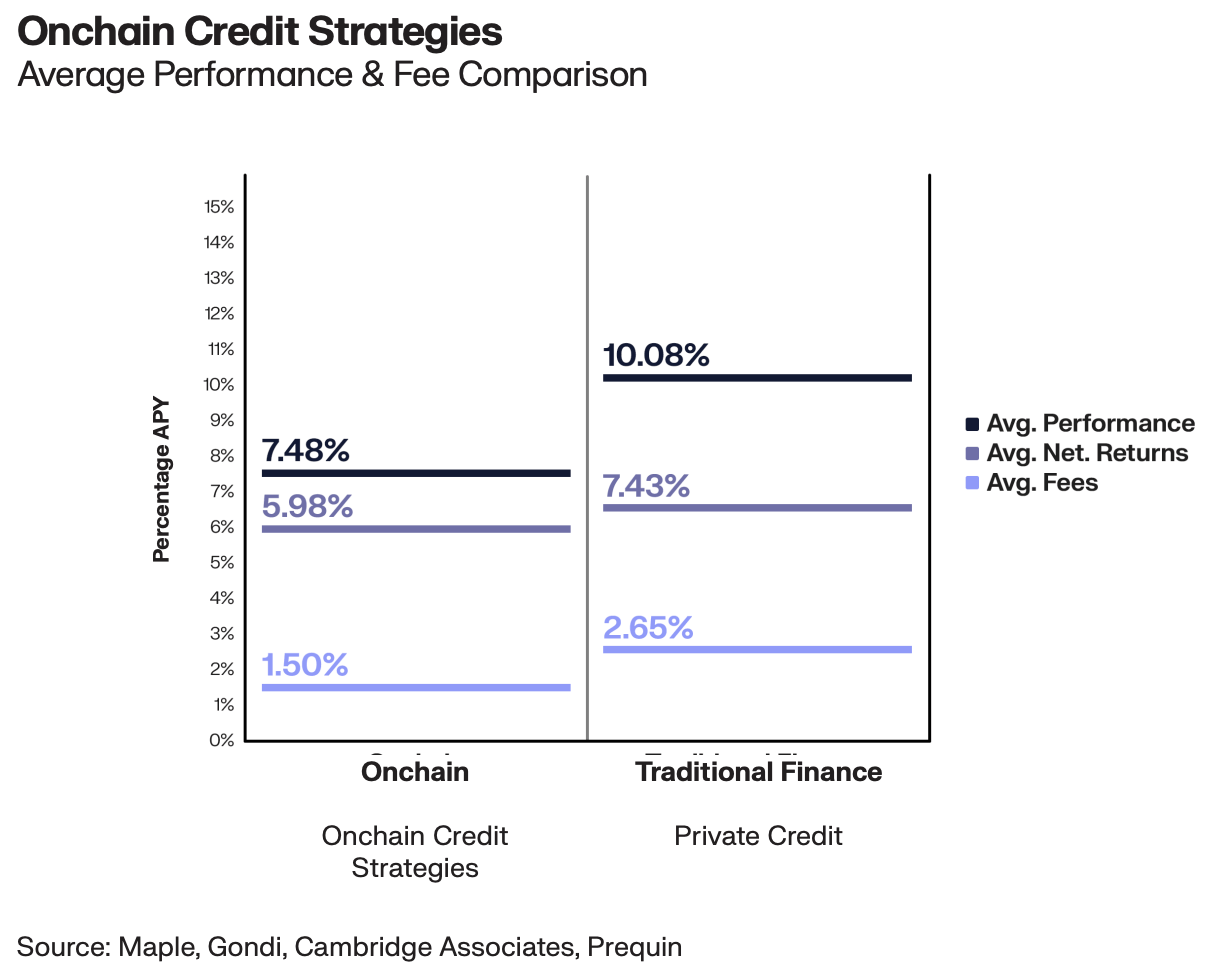

Performance: Competitive but Trailing Slightly

Onchain credit strategies deliver returns to lenders. But the data shows they lag slightly behind automated yield vaults after fees.

Why the gap?

- Human overhead — credit strategies require active underwriting, which introduces cost that automated strategies avoid

- Default risk — even with rigorous assessment, some loans default. The net yield to lenders absorbs these losses.

- Duration mismatch — credit pools lock capital for defined terms. This reduces the capital efficiency that vaults achieve through continuous reallocation.

- Fee structure — pool delegates earn management and performance fees for their underwriting work, compressing net returns to depositors

The slight underperformance versus automated yield vaults (which outperform TradFi by 186 bps) does not mean credit strategies fail. It means they serve a different purpose. Credit earns yield from real economic activity — actual businesses borrowing for actual operations. That carries intrinsic value beyond raw basis points.

Who Lends and Who Borrows

The capital supply pattern mirrors the broader onchain ecosystem. Whales and dolphins — wallets exceeding $100,000 and $1 million respectively — provide 70–99% of lending capital. These are not retail users chasing yield. They are sophisticated allocators who understand credit risk and price it accordingly.

Borrowers span a range:

- Crypto market makers — need short-term working capital to fund trading operations

- DeFi protocols — borrow for treasury management and operational expenses

- Traditional corporates — increasingly exploring onchain credit for faster access and lower origination costs

- Real-world asset originators — borrow against tokenised receivables, invoices, or other assets

The borrower base is diversifying. As tokenised real-world assets grow, the collateral base for onchain credit expands correspondingly. More collateral types mean more lending opportunities.

Advantages Over Traditional Private Credit

Traditional private credit — a $1.7 trillion market — runs on relationships, legal agreements, and opaque pricing. Onchain credit maintains the core function while rebuilding the infrastructure:

- Origination speed — days rather than weeks or months

- Transparency — lenders see the full loan book, not just a summary

- Secondary liquidity — lending positions can potentially be traded, unlike traditional private credit which locks capital for years

- Global access — borrowers and lenders connect without geographic restrictions or banking relationships

- Automated servicing — interest payments, covenant monitoring, and default triggers execute automatically

The overhead savings from automation and disintermediation do not yet fully flow to lenders — pool delegates capture a portion. But as the market matures and competition intensifies among delegates, net yields to lenders should compress upward.

Risk Management Onchain

Credit risk does not disappear because lending moves onchain. It becomes more visible.

Onchain credit protocols employ multiple layers of risk management:

- Pool-level diversification — spreading capital across multiple borrowers limits single-name exposure

- Collateral monitoring — real-time tracking of collateral values with automatic margin calls

- Reserve funds — pools maintain first-loss capital that absorbs defaults before lender deposits are affected

- Reputation systems — borrower history is onchain and permanent. Default once, and every future pool sees it.

Maple’s restructuring after losses in 2022 demonstrates the system’s self-correcting nature. Protocols that mismanage risk lose capital to competitors. The market disciplines faster than regulators can.

The Institutional Bridge

Onchain credit is perhaps the most natural convergence point between DeFi and traditional finance. Credit professionals understand underwriting. They understand risk assessment. The onchain component is infrastructure, not ideology.

For traditional credit professionals, Maple and Gondi represent familiar economics on superior rails. Same analytical frameworks. Same borrower assessment. Faster execution. Better transparency. Lower friction.

The tokenisation shift makes this convergence inevitable. As more real-world assets exist onchain, the collateral base for onchain credit grows exponentially. And as stablecoin payments become standard for business operations, the demand for stablecoin-denominated credit follows naturally.

Growth Outlook

Within the broader $35 billion onchain asset management ecosystem, credit strategies represent a growing but still smaller share compared to automated vaults. The base case projects total onchain AUM reaching $64 billion by end-2026.

Credit’s share should expand as:

- Tokenised collateral types multiply

- Regulatory frameworks for onchain lending clarify

- Traditional credit professionals migrate to onchain infrastructure

- Cross-border lending becomes frictionless through stablecoin settlement

The $1.7 trillion traditional private credit market is the addressable opportunity. Onchain credit does not need to replace it. Capturing even a fraction represents tens of billions in new lending activity.

Frequently Asked Questions

What are onchain credit strategies?

Onchain credit strategies are institutional lending protocols where lenders deposit capital into smart contract-governed pools and earn yield from borrower interest payments. Pool managers handle underwriting and borrower assessment. Protocols like Maple and Gondi power this market, connecting institutional lenders with vetted borrowers on transparent, programmable infrastructure.

How do Maple and Gondi differ?

Maple operates as a marketplace for institutional credit with pool delegates who curate lending strategies and assess borrowers, serving primarily unsecured or partially secured institutional loans. Gondi focuses on secured lending where borrowers post onchain collateral. Different risk profiles and return characteristics, but both use blockchain-native infrastructure.

Do onchain credit strategies outperform traditional lending?

Onchain credit strategies deliver competitive yields but lag slightly behind automated yield vaults after fees. The gap comes from human underwriting costs, default absorption, and duration constraints. However, they offer faster origination, greater transparency, and potentially more liquid positions compared to traditional private credit funds.

Who provides capital to onchain lending pools?

Institutional and high-net-worth allocators dominate. Whales (wallets over $1 million) and dolphins (wallets over $100,000) supply 70–99% of lending capital across onchain credit pools. These are sophisticated allocators who understand and price credit risk, not retail yield-seekers.