Onchain Asset Management: Designing the Future of Investment Strategies

Onchain Asset Management: $35B AUM, 118% Growth in 2025

$35 billion in assets under management. 118% growth in a single year. Onchain asset management is no longer an experiment at the margins of finance. It is a structural shift in how capital gets allocated, managed, and compounded.

We have watched this space evolve from a handful of yield aggregators into a full-spectrum investment ecosystem. Automated vaults, discretionary strategies, credit markets, structured products. Each category now attracts institutional-grade capital at institutional-grade scale.

Three protocols alone account for nearly a third of it all.

The $35 Billion Landscape: Where Capital Lives Onchain

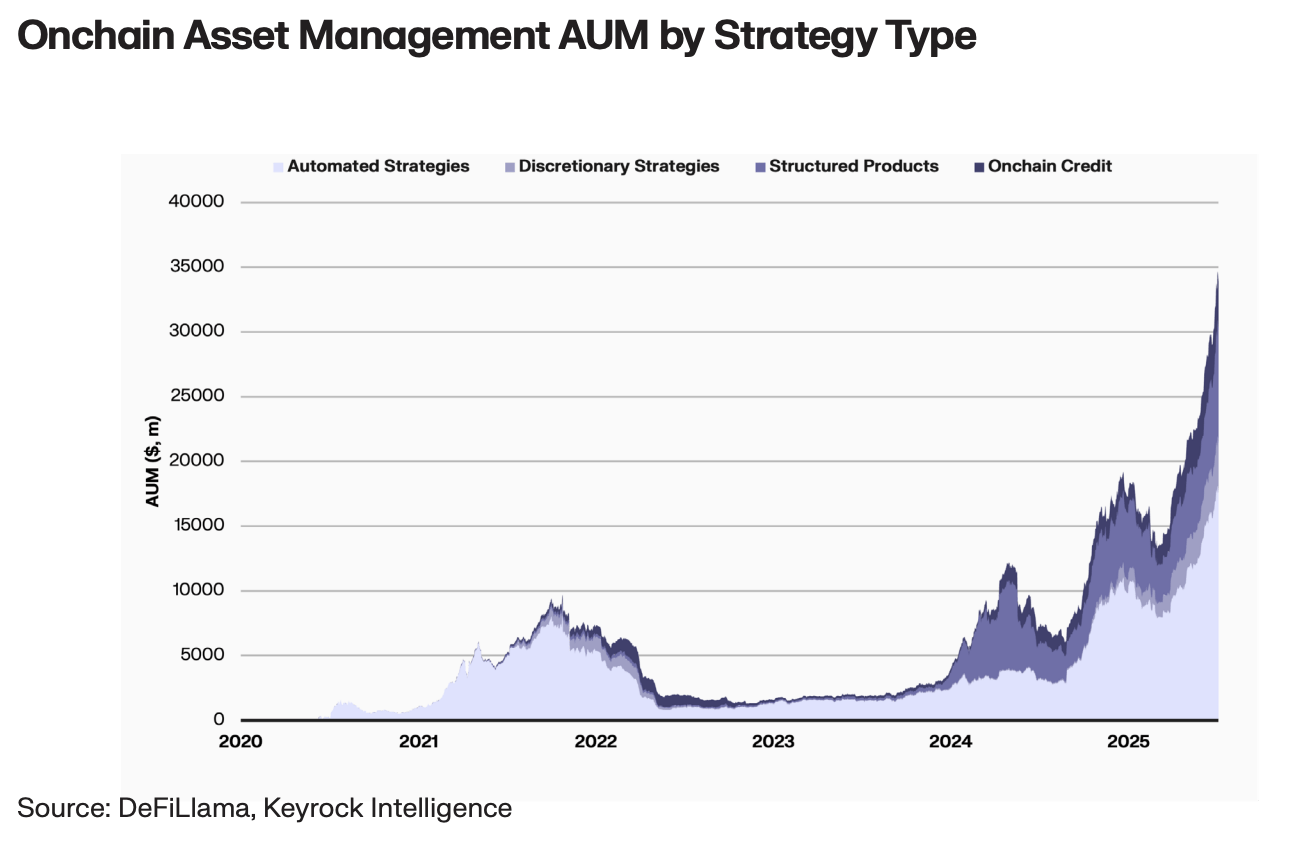

As of 2025, onchain asset management AUM stands at $35 billion. That represents 118% year-to-date growth. Not a slow climb. A repricing of what programmable finance can absorb.

The capital concentrates across four distinct strategy types:

- Automated yield vaults — $18 billion AUM, the dominant category by far

- Discretionary strategies — actively managed by teams like Gauntlet and MEV Capital

- Onchain credit — institutional lending through Maple, Gondi, and peers

- Structured products — yield tokenisation and derivatives via Pendle and Aevo

The ecosystem runs on composability. Each protocol plugs into others. Capital flows between strategies with zero friction. That interconnection is not a feature. It is the architecture.

Protocol Concentration: Morpho, Pendle, Maple

Three names dominate. Morpho, Pendle, and Maple together account for 31% of all onchain AUM. In a space with hundreds of protocols, that concentration tells you something about product-market fit.

Morpho powers permissionless lending markets with modular risk parameters. Pendle splits yield-bearing assets into principal and yield tokens, enabling precise duration and rate exposure. Maple connects institutional borrowers with onchain liquidity through structured credit pools.

Each occupies a distinct niche. Together they form the backbone of an industry that barely existed three years ago.

Who Supplies the Capital

This is not retail-driven growth. The data is unambiguous.

Whales — wallets holding over $1 million — and dolphins — wallets above $100,000 — supply 70–99% of AUM across every strategy type. The range varies by protocol, but the pattern holds universally. Large allocators have found product-market fit with onchain strategies.

Why? Composability. Programmability. Transparency. These are not marketing words. They are structural advantages that let sophisticated capital move faster, compound harder, and verify everything onchain.

When you can audit a strategy’s full history in real time, redemption becomes a transaction rather than a negotiation. That changes the risk calculus for every allocator.

Why Onchain Wins: Structural Advantages Over Traditional

Traditional asset management operates on trust, paperwork, and quarterly reports. Onchain strategies operate on code, transparency, and continuous settlement.

The advantages are not marginal. They are categorical:

- Composability — strategies can be stacked, combined, and routed through other protocols without intermediaries

- Programmability — risk parameters, rebalancing logic, and fee structures execute autonomously via smart contracts

- Transparency — every allocation, every fee, every return is verifiable onchain in real time

- Instant redemption — no lock-ups, no 45-day notice periods, no gates

As Kevin de Patoul, CEO of Keyrock, puts it: we have seen this evolution firsthand. The infrastructure that powers tokenised assets and stablecoin settlement now underpins a full investment management stack.

The Strategy Spectrum

Not all onchain capital wants the same thing. The strategy spectrum mirrors traditional finance — but with radically different plumbing.

Automated Yield Vaults

The workhorse of onchain asset management. These vaults automatically allocate deposits across lending markets, liquidity pools, and staking opportunities. $18 billion in AUM. Performance beats traditional peers by 186 basis points after fees. Protocols like Yearn pioneered this category. Morpho and others have since scaled it to institutional relevance.

Discretionary Strategies

Human judgement meets onchain execution. Teams like Gauntlet and MEV Capital run actively managed strategies that deliver returns net of fees in line with TradFi hedge funds. The difference: full transparency, instant settlement, and no minimum investment periods measured in years.

Onchain Credit

Credit strategies bring institutional lending onchain. Maple and Gondi lead. Borrowers access capital without the friction of traditional bank relationships. Lenders earn yield backed by real underwriting. Performance lags slightly after fees compared to automated vaults, but the risk profile attracts a different allocator.

Structured Products

Pendle and Aevo push the frontier with yield tokenisation and derivatives. Fixed-rate exposure, leveraged yield, principal-protected structures. These products replicate what investment banks build — but with permissionless access and transparent pricing.

The Institutional Inflection

The capital composition reveals maturity, not hype. When 70–99% of AUM comes from wallets exceeding $100,000, you are looking at institutional allocation decisions. Due diligence. Risk committee approvals. Portfolio construction models that sanction onchain exposure.

This is the inflection point every emerging asset class must reach. The moment large allocators move from exploration to committed allocation. Onchain asset management crossed that threshold in 2024. The 118% growth in 2025 is the result.

What converted them? Performance data. Automated yield vaults beating traditional peers by 186 basis points is not a theoretical argument. It is a track record that risk committees can underwrite.

Growth Trajectory: Where This Goes

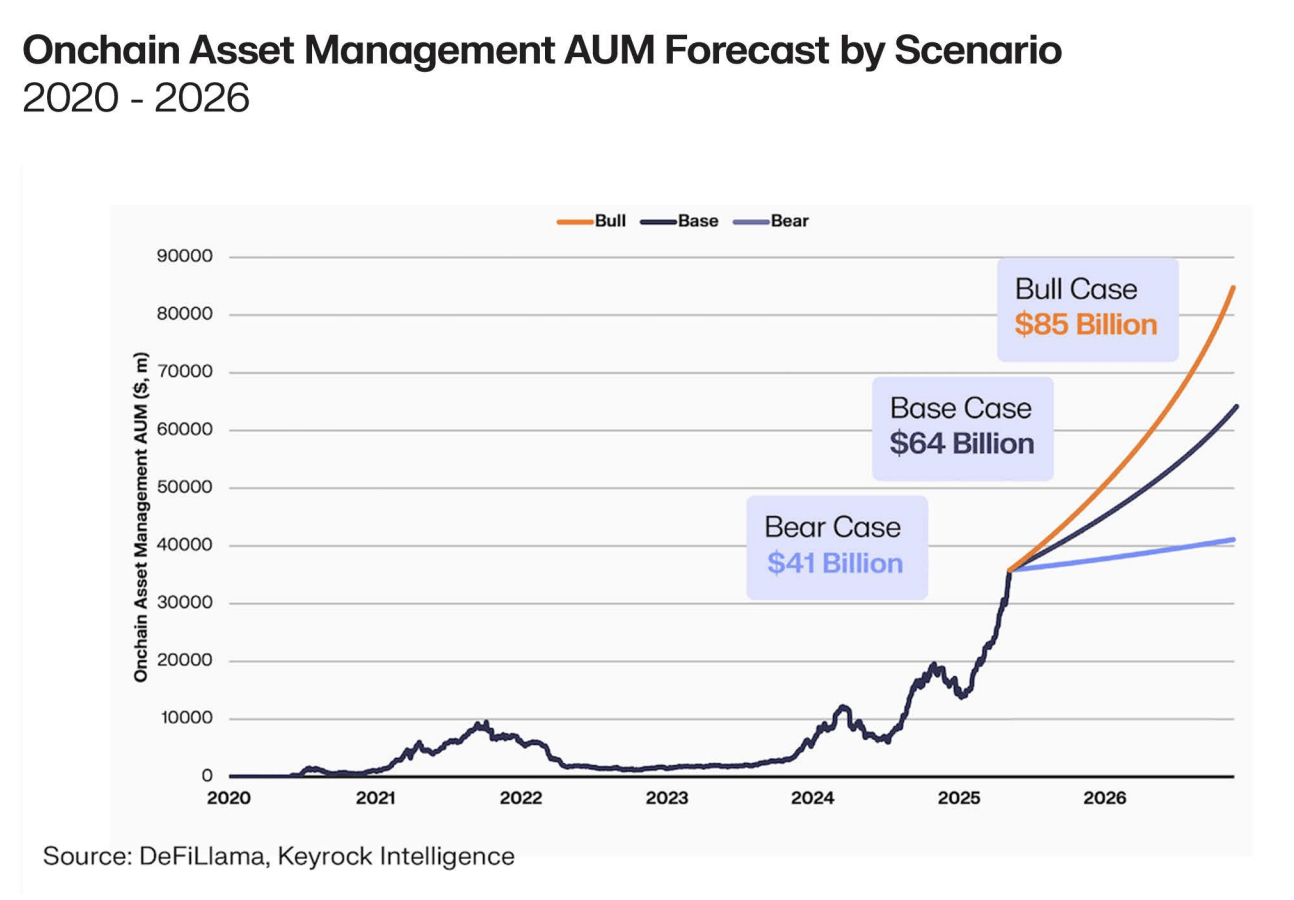

The base case projects $64 billion in onchain AUM by end-2026. A 56.4% compound annual growth rate. The bull case reaches $85 billion. Both scenarios assume continued institutional adoption and regulatory clarity around tokenised financial infrastructure.

These are not fantasy numbers. They are extrapolations from current run rates, adjusted for macro conditions and protocol maturity curves.

Five catalysts power the next phase:

- Regulatory clarity — MiCA in Europe, evolving US guidance, progressive frameworks in UAE and Singapore

- Tokenised collateral expansion — every real-world asset that moves onchain expands the strategy design space

- Stablecoin growth — more stablecoin supply means more capital available for deployment

- Infrastructure maturation — custody, compliance, and institutional onramps removing friction

- Track record compounding — each quarter of consistent performance converts another tier of allocators

The flywheel is simple: better infrastructure attracts more capital. More capital funds better infrastructure. We are still in the early turns.

Frequently Asked Questions

What is onchain asset management?

Onchain asset management refers to investment strategies that operate entirely on blockchain infrastructure. Capital allocation, rebalancing, fee collection, and redemption all execute via smart contracts. This replaces traditional fund administrators, custodians, and transfer agents with programmable, transparent code.

How large is onchain asset management in 2025?

Total AUM reached $35 billion in 2025, representing 118% year-to-date growth. Three protocols — Morpho, Pendle, and Maple — account for 31% of all assets. Automated yield vaults represent the largest category at $18 billion.

Who invests in onchain asset management strategies?

Institutional and high-net-worth allocators dominate. Whales (wallets over $1 million) and dolphins (wallets over $100,000) supply 70–99% of AUM across all strategy types. Retail participation exists but does not drive the growth.

What are the main types of onchain investment strategies?

Four categories dominate: automated yield vaults ($18 billion), discretionary strategies (actively managed), onchain credit (institutional lending), and structured products (yield tokenisation and derivatives). Each serves different risk-return profiles and investor preferences.