Prediction Markets: The Next Frontier of Financial Markets

Institutional Hedging with Prediction Markets: The New Derivatives (2026)

For decades, hedging against a specific event — an election result, a regulatory decision, an inflation surprise — meant cobbling together proxy positions from correlated assets. Short a sector ETF. Buy VIX futures. Construct multi-leg options trades. Hope the correlation holds.

Prediction markets eliminate that indirection. You trade a contract that pays out based on the event itself — not its secondary market effects.

Fixed payouts. Capped risk. No greeks. No margin calls. As we describe it in our research, prediction markets are the simplest derivative format available. For institutional risk desks, that simplicity is the feature.

Why Prediction Market Hedging Works

Traditional derivatives carry structural overhead that prediction markets simply strip away.

Options have time decay (theta), sensitivity to volatility (vega), directional risk (delta and gamma), and margin accounts that can trigger forced liquidation at the worst moment. Futures carry rollover costs and basis risk. Structured products embed counterparty risk and opaque pricing.

A prediction market contract on a specific event has a binary payoff: $1 if the event occurs, $0 if it does not. Maximum loss is the purchase price. No margin requirements, no greeks to hedge, no expiration roll, no counterparty risk beyond the platform itself.

As Justin Riggs puts it, prediction markets offer “pure speculation without the baggage of traditional derivatives.” For institutional hedgers, that translates into faster implementation, clearer risk profiles, and lower operational overhead.

Event-Level Hedging vs. Proxy Hedging

The core value of prediction market hedging is precision. You hedge the event, not its symptoms. To understand why that matters, look at the alternatives institutions have historically relied on.

The Brexit Example

When the 2016 Brexit referendum approached, hedge funds with significant UK exposure needed protection against a Leave vote. No derivative directly referenced the referendum outcome.

So firms hired private pollsters, built proprietary models, and placed FX bets — shorting the pound or buying USD/GBP options — as indirect hedges. Capital-intensive, imprecise, and exposed to basis risk. The pound’s movement post-vote correlated with the Leave outcome but depended on dozens of other factors: market positioning, central bank response, risk-off flows.

A prediction market contract — “Will the UK vote to leave the EU? Yes/No” — would have offered a direct, event-level hedge with known payoffs, no basis risk, and no need for private polling infrastructure.

The Trump Trade Example

The 2016 U.S. presidential election produced a similar tangle. “Trump trades” involved long USD, short Mexican peso, short Treasuries, long defence stocks — each position carrying its own risk factors unrelated to the election outcome. Enormous capital required. Substantial basis risk.

Prediction markets compress all of that into a single contract. One price. One binary outcome. One known maximum loss.

For institutional risk management, simplicity is capital efficiency.

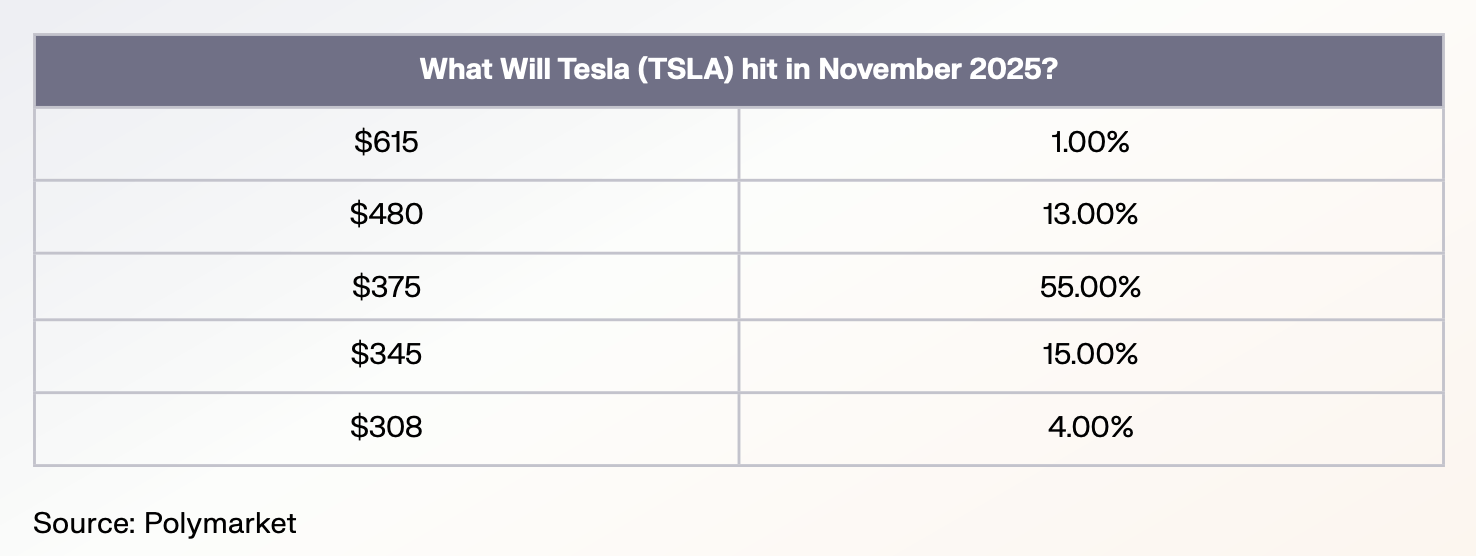

Prediction Markets as Options: The TSLA Multi-Strike Example

One of the most compelling demonstrations of prediction markets functioning as derivatives comes from Polymarket’s multi-strike markets on Tesla (TSLA).

Rather than offering a single binary contract, Polymarket created markets at multiple price thresholds — effectively constructing a discrete probability surface across different TSLA price levels. Each threshold functions as a binary option: “Will TSLA close above $X on date Y?”

Buy Yes at a lower strike and No at a higher strike, and you have a range-bound position analogous to a traditional options spread. The difference: instead of backing out implied probabilities from options chain pricing and implied volatility, the probability is stated directly in the contract price.

Explicit probability surface. Capped risk. No options-chain infrastructure or margin account required.

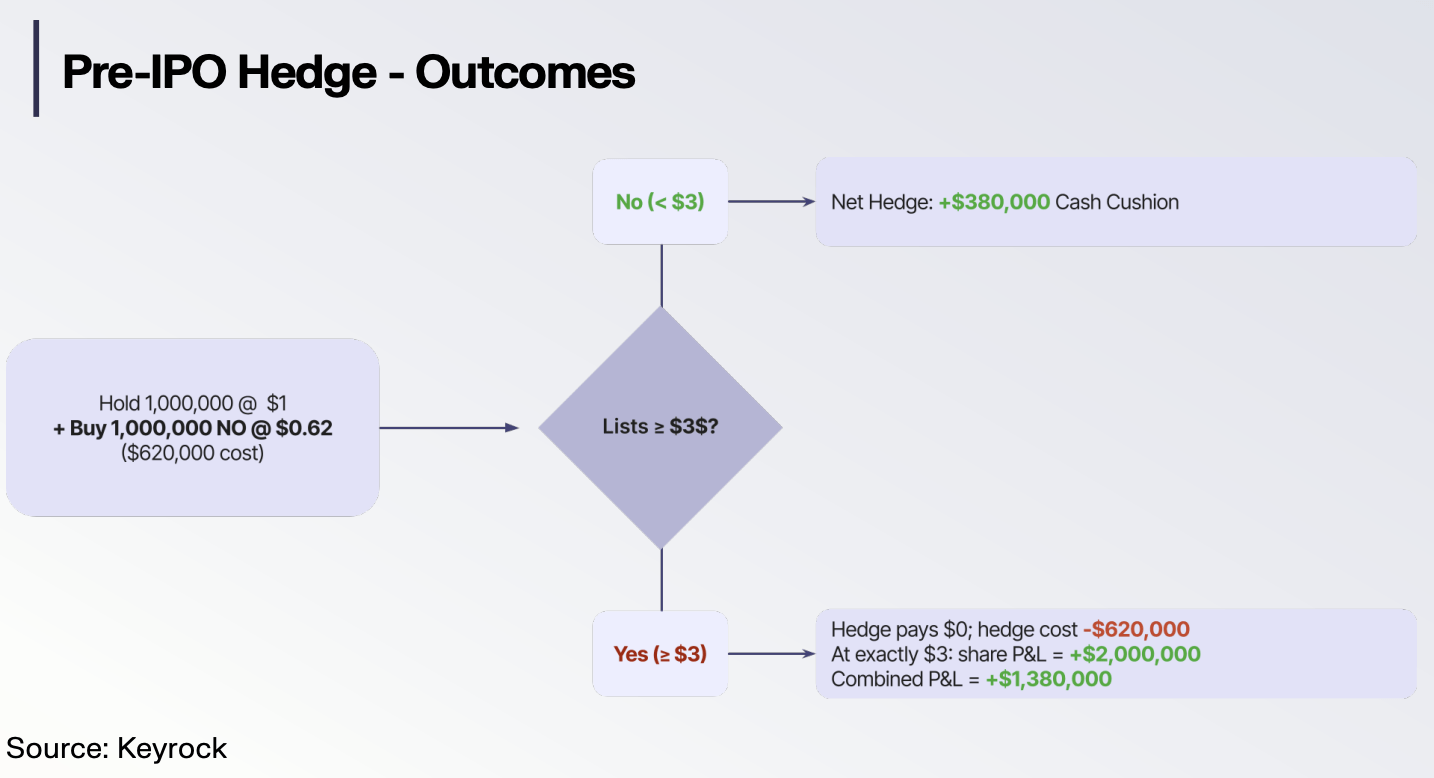

Pre-IPO and Pre-TGE Hedging

Prediction markets open hedging possibilities that do not exist in traditional finance. Pre-IPO and pre-TGE (Token Generation Event) hedging is the most significant.

You hold a substantial pre-IPO allocation. If the IPO is delayed or cancelled, that allocation loses most of its value. You cannot buy a put option on a stock that does not yet trade publicly.

With prediction markets, you buy No contracts on the IPO occurring. In an illustrative scenario from our research: an investor buys No at $0.62 for 1 million contracts. IPO cancelled — each contract pays $1, generating a $380,000 profit that offsets losses on the locked-up equity position. IPO proceeds — the investor loses $620,000 on the prediction market position but profits from the IPO itself.

Cost known upfront. Maximum loss capped. Hedge directly references the event that creates the risk. No traditional derivative replicates this.

The same logic applies to Token Generation Events in crypto, where pre-TGE investors face identical binary risk: the token launches and their allocation becomes liquid, or it does not.

Prediction Markets vs. Traditional Hedging Instruments

To appreciate the institutional appeal, compare the mechanics directly.

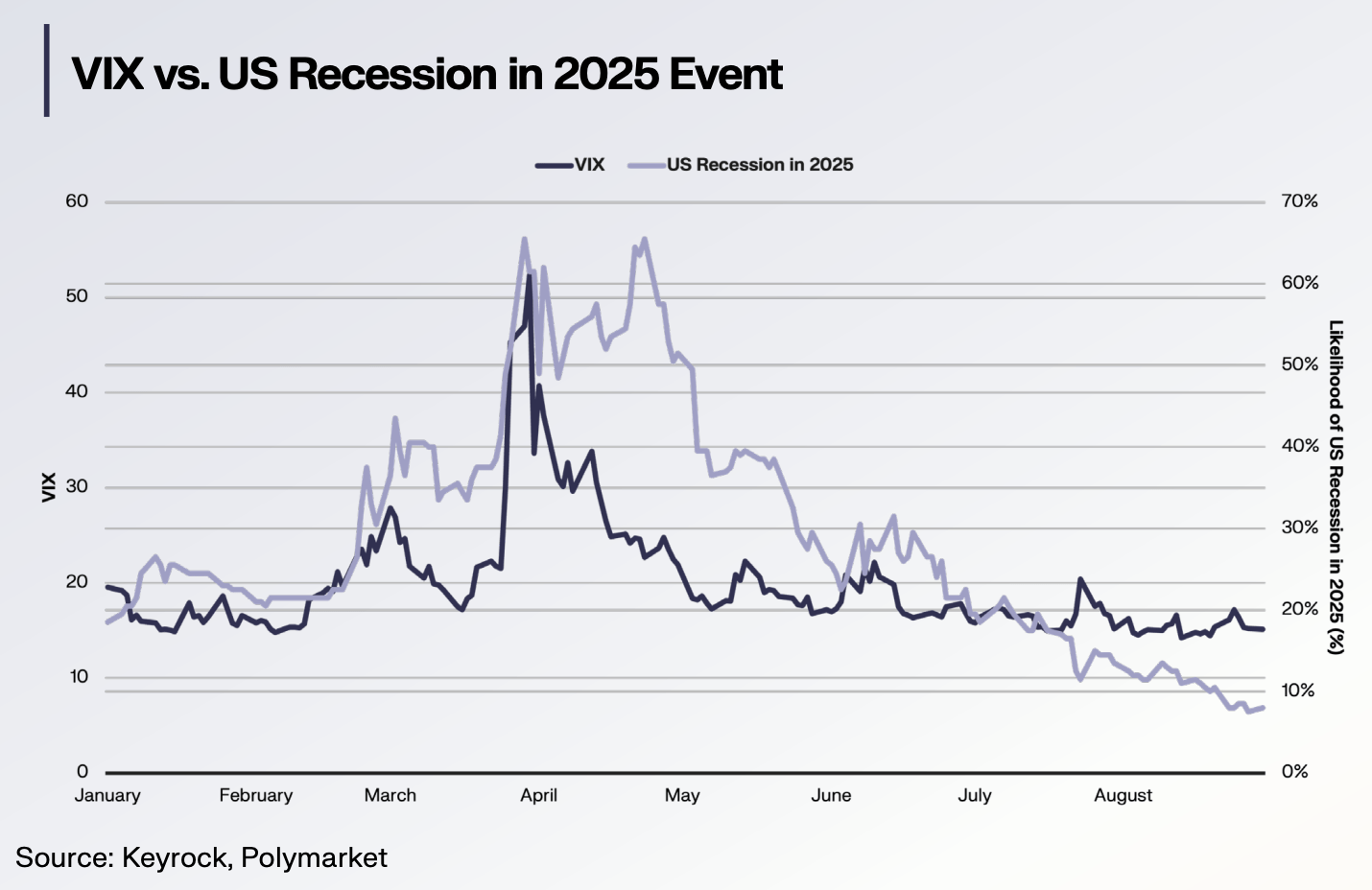

VIX vs. U.S. Recession Event Contracts

The VIX — the “fear gauge” — hedges the symptoms of uncertainty (expected stock market volatility), not the cause (the specific event creating it). An institution worried about a U.S. recession buys VIX futures, but the VIX captures all sources of volatility, not just recession risk. You pay for hedging against irrelevant volatility drivers and face rollover costs on VIX futures contracts.

A prediction market contract on “Will the U.S. enter a recession in 2025?” isolates the specific risk. Payoff tied directly to the outcome you care about. No contamination from unrelated volatility sources.

CME FedWatch vs. Polymarket Fed Rate Markets

Both track expectations for monetary policy. Both show strong co-movement around macro releases. But the prediction market version offers real-time pricing with global participation, no futures margin requirements, and the ability to hold a position through resolution without rollover.

Kalshi Inflation Markets as Leading Indicators

The data here is striking. FedNow is 4.3x more volatile than Kalshi’s inflation market. Kalshi prices move more smoothly and often anticipate where FedNow expectations will settle — functioning as a leading indicator that reprices ahead of official data releases.

For institutions using inflation expectations to size positions or make allocation decisions, prediction markets offer a cleaner, less noisy input than traditional rate-based measures.

Three Institutional Use Cases: The KPMG Framework

Duncan Hennes of KPMG identifies three primary ways institutions engage with prediction markets:

- Proprietary trading: Firms with superior information or models trade mispriced contracts for profit. Fixed-payout structure makes P&L attribution straightforward and risk management simple.

- Forecasting: Organisations use prediction market prices as inputs for decision-making — strategic planning, risk assessment, capital allocation. A continuously updated consensus probability from participants with financial incentives to be accurate.

- Hedging: Institutions directly offset event-specific risks by taking positions that pay out when adverse outcomes occur. This is the “new options” thesis — event-level derivatives that complement or replace traditional hedging instruments.

These use cases are not mutually exclusive. A firm can use market prices to inform forecasting models, identify mispricings for its prop desk, and hedge specific event exposures — all on the same platform.

The Capital Efficiency Advantage

Traditional derivatives hedging demands significant operational infrastructure:

- Margin accounts with substantial capital buffers

- Ongoing margin maintenance and potential margin calls

- Roll costs for futures and options approaching expiry

- Multiple correlated positions to approximate desired exposure

- Continuous delta hedging as market conditions shift

Prediction market hedging requires none of this. Maximum cost is known at entry. No margin calls. No delta to manage. A single contract directly references the event being hedged.

For capital-constrained institutions or those seeking to minimise operational complexity, the advantage is significant.

What Stands Between Prediction Markets and Full Institutional Adoption

Despite the structural advantages, barriers remain. Regulatory clarity varies by jurisdiction. Position limits on platforms like Kalshi may be too small for large institutional hedges. Liquidity in niche markets is insufficient for institutional-size positions. Many compliance frameworks have not yet been updated to include event contracts as approved hedging instruments.

But the trajectory is clear.

Kalshi’s CFTC-regulated status, the onboarding of professional market makers like Susquehanna (which increased order book depth by 30x in certain markets), and growing institutional engagement all point in one direction: prediction markets becoming a standard component of the institutional hedging toolkit.

For institutions hedging event risk today through expensive, imprecise proxy positions, prediction markets offer the alternative: direct exposure to the events that matter, fixed and capped risk, zero margin requirements, and accuracy that outperforms the tools currently used to size those proxy hedges in the first place