Stablecoin Payments: The Trillion Dollar Opportunity

How Stablecoin Payment Cards work? A guide

Introduction

Stablecoin-linked debit and credit cards bring digital dollars into everyday life. By connecting stablecoin balances directly to Visa and Mastercard rails, they let users pay tens of millions of merchants worldwide. Two key innovations are helping drive this shift.

On the backend, stablecoins enable tokenized receivables that streamline card settlement and improve issuers’ capital efficiency. On the frontend, users can now hold stablecoins on card rails, offering seamless dollar access and usability, even in dollar-constrained markets.

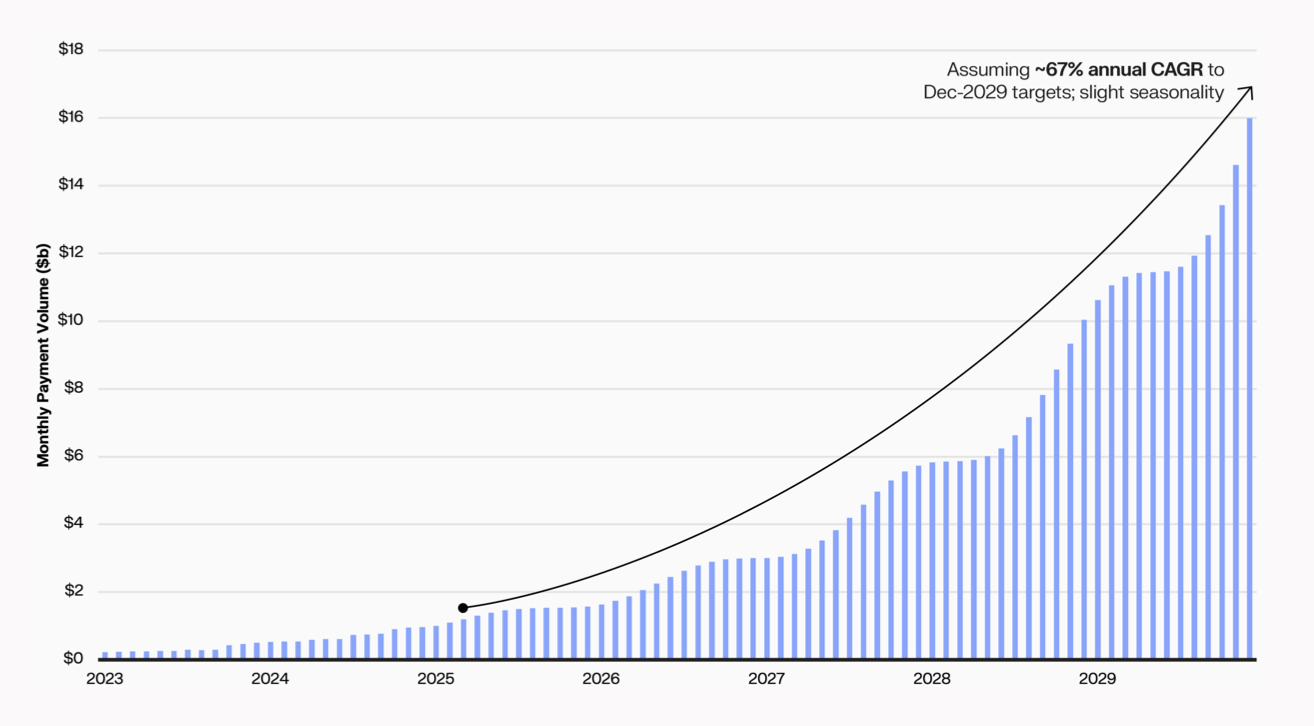

Artemis’ data shows that stablecoin card payment volume (among tracked partners) grew from about $250 million per month in early 2023 to over $1 billion per month by early-2025.

“Crypto can’t be a compromise. It has to be better. More convenient, more flexible, more powerful. We’re already closer than we were a year ago, but to win, we have to integrate features like direct debit, SEPA transfers, and local alternatives to Visa and Mastercard. We need to blur the line so completely that users forget there ever was a line.” — Stefan George, Co-Founder of Gnosis Pay

Stablecoin Monthly Card Volumes Set to Surge 15x to $16b

Source: Artemis, Keyrock

Tokenized receivables

Traditionally, when you use a credit card, the issuer (e.g. Chase, Capital One) advances payment to the merchant, creating a receivable on its balance sheet. The issuer must then finance that receivable until the customer’s repayment, often by selling batches of receivables to warehouse lenders. This legacy process involves heavy paperwork and coordination, and it typically imposes a ~2‑week lag between purchase and capital recovery. The result is significant working-capital inefficiency.

Rain, a stablecoin card-issuing platform, has disrupted this model by fully tokenizing its Visa credit receivables. In Rain’s system, corporate clients deposit USDC (or another approved stablecoin) into a vault to establish their credit limit. At the end of each billing cycle, any outstanding balance is settled automatically through onchain liquidation.

“Nearly 50% of our e-commerce transactions globally are tokenized.” — Ryan McInerney, CEO of Visa Inc.

Moreover, Rain tokenizes settlements on a per-swipe basis. When a user spends on their card, Rain instantly borrows the amount from a lender and settles the merchant immediately, onchain. This eliminates batching. Every transaction immediately releases working capital.

All repayments also flow onchain. When clients pay their bills, smart contracts automatically distribute principal and interest to lenders, removing any fiat repayment risk. Rain reports saving roughly $180,000 in legal and operational costs annually thanks to this automation.

Payment cards for USD access

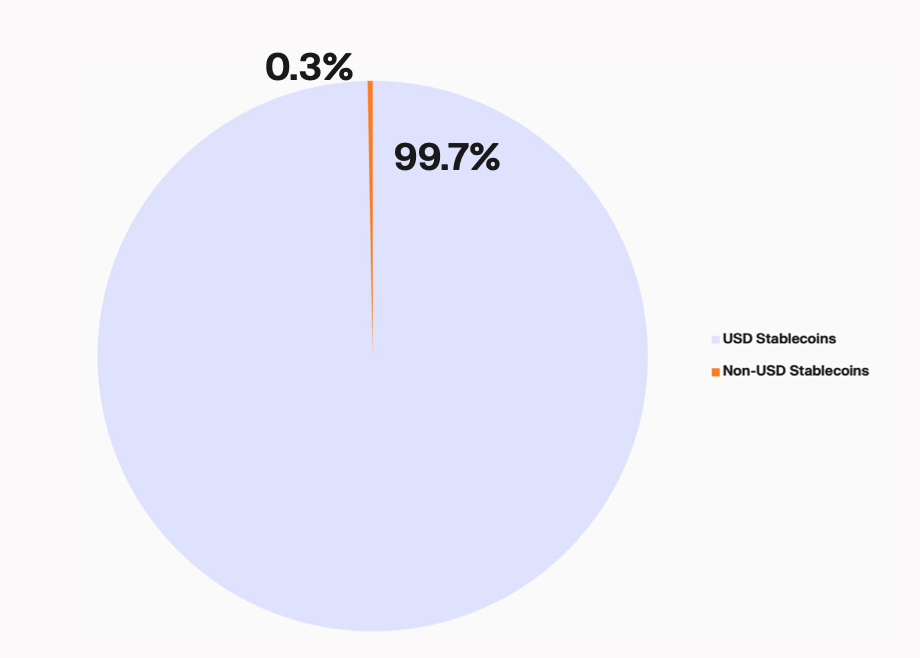

Underlying consumer demand for these cards is the global need for reliable dollar access. About 75% of USD resides outside the United States, yet many regions lack stable access to dollars through local banks. In fact, a survey in Nigeria, Indonesia, Turkey, Brazil and India found 47% of respondents cited better dollar access as their primary motivation for using stablecoins.

USD Stablecoins Dominate The Market

Source: RWA.xyz, Keyrock

Stablecoins act like a global dollar correspondent when linked to Visa/Mastercard. They provide both the stability of a dollar balance and the universal acceptance of major cards. Users holding stablecoin on a card can spend at any merchant and still retain the option to earn yield on their underlying balance.

The practical benefit is clear, since the remittance recipient often pays two fees when converting USD to local currency:

- Workers in developed economies send salaries or remittances abroad.

- Recipients receive funds in local currency, often facing high inflation and steep exchange fees due to less competitive banking markets.

- Consequently, recipients pay fees when converting inbound USD to local currency and when converting local currency back to USD for international purchases (e.g. paying for Amazon cloud services).

“Localized stablecoins are part of the solution, not perfect, but necessary. Most people don’t think in dollars; they think in their own currency because that’s how they live and spend. Even in countries like Argentina, people still want some local exposure. And in places like Brazil, where the economy is relatively strong, local currencies are even outperforming the dollar. We shouldn’t assume everyone wants to dollarize, there’s more nuance than that.” — Stefan George, Co-Founder of Gnosis Pay

The stablecoin-linked cards use case is straightforward. A remittance-receiving family can get fully-reserved U.S. payment stablecoins (in USDC) and spend them locally with familiar card rails at minimal cost. Likewise, a global contractor can be paid in stablecoins and use them wherever Visa/Mastercard is accepted. These capabilities (e.g. stable value, global liquidity, and universal acceptance) illustrate how stablecoin-linked cards deliver real-world utility.