Store of Value to Digital Oil: How Ussage Differs Between BTC to ETH

ETH Store of Value or Utility? The Data Behind Ethereum's Dual Identity (2026)

Bitcoin and ethereum share a blockchain. They share a market. They share headlines. What they do not share is a behavioural profile. And the onchain data makes that distinction impossible to ignore.

We analysed dormancy, turnover, exchange posture, holder mobilisation, and productive deployment across both networks. The result is not a winner-takes-all verdict. It is a map of two assets doing fundamentally different jobs.

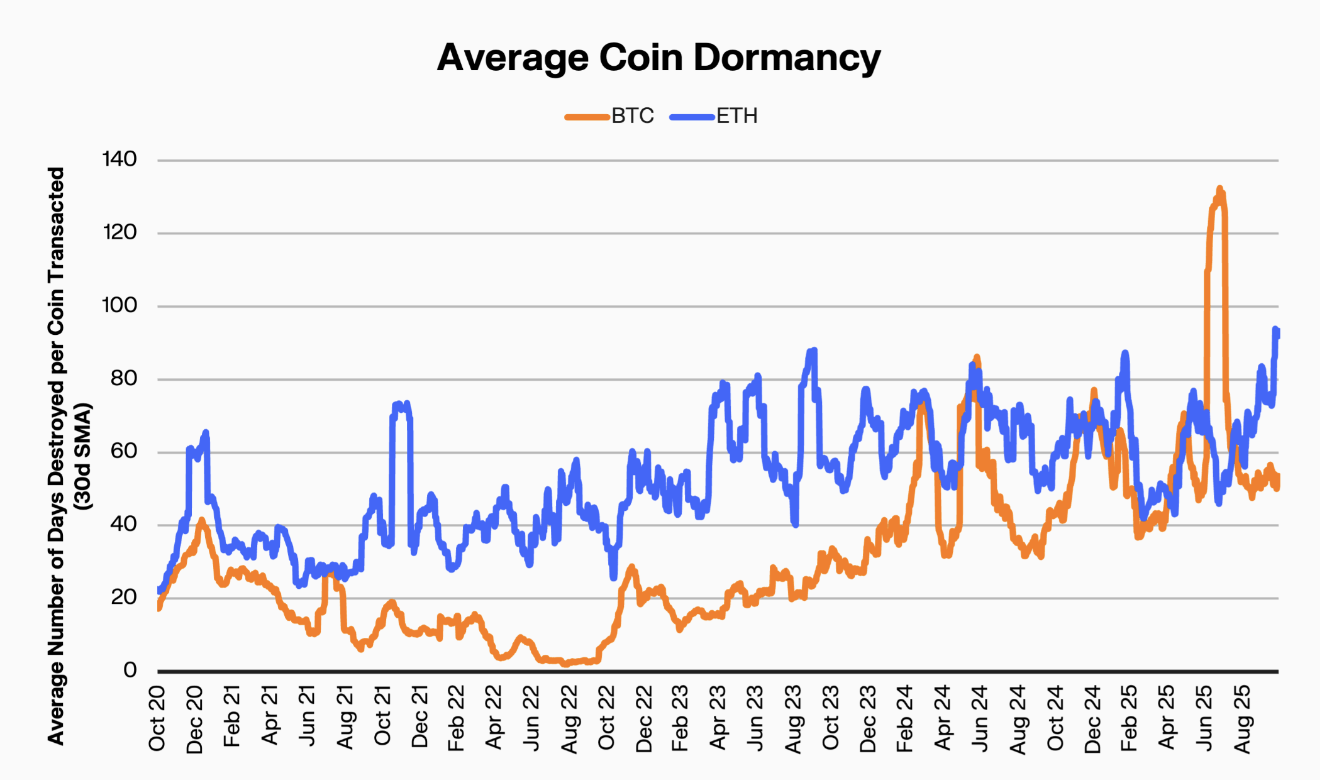

Dormancy: The Stillness Gap

61% of bitcoin supply has not moved in over a year. That is the highest sustained dormancy rate of any major crypto asset. BTC holders accumulate and wait. They treat it like gold in a vault.

ETH tells a different story. While one in four tokens are locked in staking or ETFs, the free-floating supply moves with far greater frequency. Long-term ETH holders mobilise at three times the rate of their BTC counterparts.

The gap is not marginal. It is structural.

BTC’s dormancy profile aligns with gold, which turns over 0.29% of its supply daily. ETH’s profile sits somewhere between a monetary asset and productive capital. Neither is wrong. But conflating the two misses the point entirely.

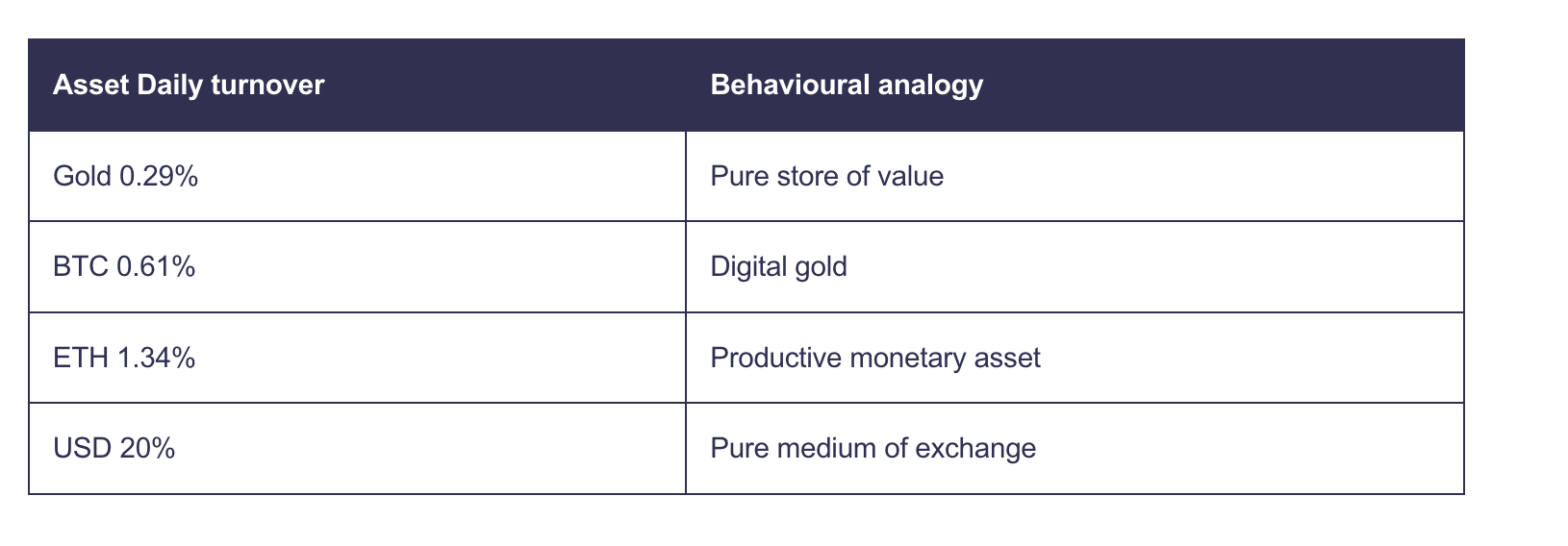

Turnover: Speed Reveals Identity

Daily turnover is the clearest lens we have into how an asset actually behaves in the hands of its holders.

BTC at 0.61% daily turnover sits twice as high as gold but thirty-three times lower than the dollar. ETH at 1.34% doubles BTC’s rate. The spectrum runs from vault to velocity, and these two assets occupy distinctly different positions on it.

For investors building a bitcoin-as-digital-gold thesis, that 0.61% figure is validation. For those evaluating ETH’s dual identity, the 1.34% confirms the asset moves more than a pure store of value should.

Exchange Posture: Two Flavours of Exodus

Both BTC and ETH are leaving exchanges. The magnitude and trajectory could not be more different.

BTC exchange balances have declined 1.5%. The current exchange share sits at 14.3%, a slow and steady drift that has persisted since 2020. Bitcoin leaves exchanges into cold storage, multisig custody, and ETF wrappers. The movement is methodical.

ETH exchange balances have declined 18%. Exchange share has collapsed from 29% to 11.3%. That is not a drift. That is a structural evacuation.

Where does the ETH go? Three destinations absorb the outflow: staking contracts, DeFi protocols, and institutional custody. Each pulls ETH off exchanges and into productive or locked structures. The exchange decline narrative applies to both assets, but ETH’s version is more dramatic by an order of magnitude.

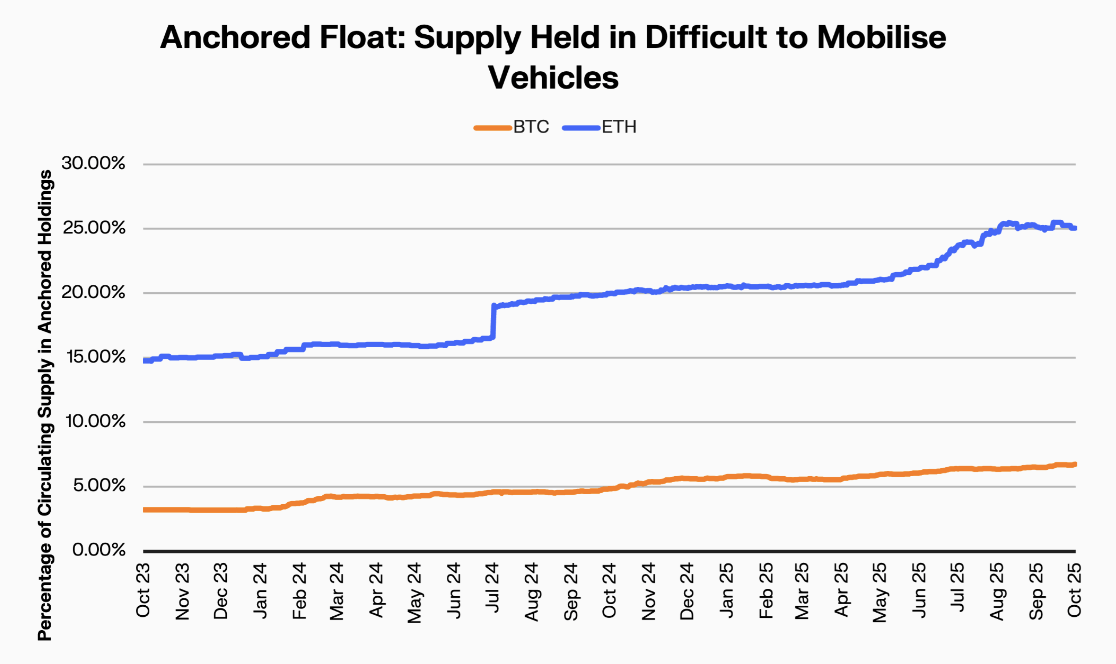

Anchored Float: Locked Supply Compared

Anchored float measures supply held in ETFs, staking, and institutional custody. These are positions designed for duration, not trading.

BTC anchored float: 6.7%. ETH anchored float: 25.1%.

That 3.7x gap challenges assumptions. More of ETH’s supply is structurally locked than bitcoin’s. BTC ETFs hold 6.7% of supply. ETH ETFs hold 5.24%. The ETF figures are comparable. The divergence comes from staking, which has no bitcoin equivalent at this scale.

DATs reinforce the pattern. BTC DATs hold 3.6% of supply. ETH DATs hold 4.9%. At every measurement point, ETH’s anchored supply exceeds bitcoin’s.

Yet bitcoin still feels more like a store of value. Why? Because dormancy and turnover matter more than lock-up ratios. Bitcoin’s supply is dormant by choice. ETH’s supply is locked by mechanism. The distinction shapes perception as much as the data does.

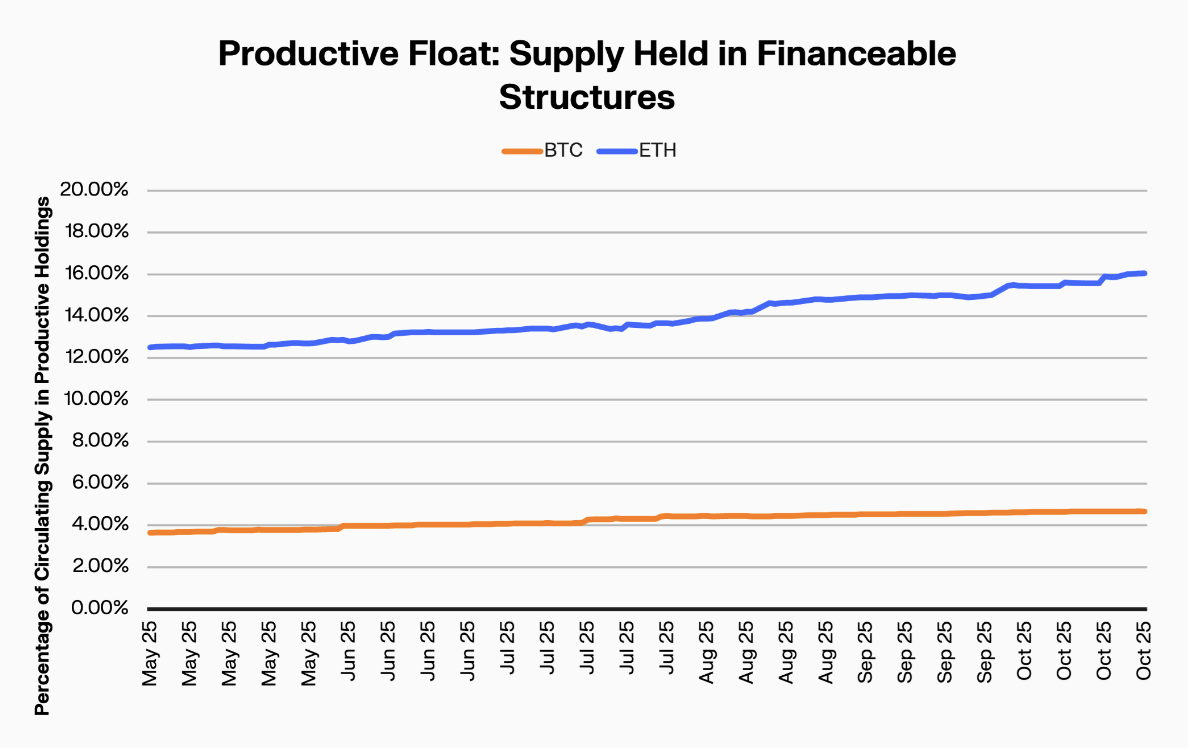

Productive Float: The Defining Divergence

Productive float captures supply actively deployed in DeFi, lending, liquid staking, and collateralised positions.

BTC productive float: 4.66%. ETH productive float: 16.05%.

ETH’s productive float is 3.4 times larger than bitcoin’s. A full 16% of ETH supply is at work inside the onchain economy. That includes liquidity pools, lending markets, restaking protocols, and bridges. Every token in productive deployment is simultaneously stored and utilised.

BTC’s 4.66% productive float reflects the early stages of bitcoin DeFi. Wrapped BTC on ethereum, bitcoin-native DeFi protocols, and cross-chain bridges account for most of it. The trajectory is upward but remains a fraction of ETH’s.

Long-Term Holder Behaviour: Patience vs Participation

Long-term holders are the backbone of any asset’s store-of-value claim. How they behave under market pressure reveals the asset’s true character.

ETH long-term holders mobilise at three times BTC’s rate. That means ethereum’s most committed holders are still significantly more active than bitcoin’s. They stake. They restake. They provide liquidity. They participate in governance.

BTC long-term holders, by contrast, do very little. They hold. The blockchain records their patience in block after block of unchanged UTXOs. This inactivity is itself a signal. A powerful one.

Neither behaviour is inherently superior. BTC’s stillness builds the digital gold narrative. ETH’s activity powers a $50 billion onchain financial system. Different assets. Different jobs.

Institutional Framing: How the Big Players See It

JPMorgan groups bitcoin alongside gold in their “debasement trade” thesis. The framing places BTC in the category of monetary hedges against fiscal expansion. No utility function required.

Fidelity positions ETH as capable of serving as “medium of exchange and store of value.” The language is deliberately inclusive. ETH does not have to choose.

VanEck pushed further, floating the idea that ETH could be a better store of value than BTC for treasuries, citing staking yield as the differentiator. Strategy, meanwhile, securitises bitcoin for traditional financial markets, treating BTC as pure monetary exposure.

The institutions are not confused. They see two distinct assets serving different portfolio functions. The onchain data confirms their positioning.

The Synthesis

BTC is digital gold. Dormant, scarce, structurally illiquid, and becoming more so with every ETF inflow and every month of unchanged supply. Its onchain behaviour maps to gold with striking precision.

ETH is digital oil. Productive, deployed, in constant motion through the machinery of decentralised finance. Its value derives not from stillness but from utility. From prediction markets to lending protocols, ETH is the fuel.

Comparing them on a single axis misses the point. The data does not crown a winner. It draws a map.

FAQ

What is the main difference between BTC and ETH onchain behaviour?

BTC displays deep dormancy (61% of supply unmoved for over a year) with low daily turnover (0.61%). ETH has a higher anchored float (25.1% locked in staking and ETFs) but also higher turnover (1.34% daily) and a productive float of 16.05% versus BTC’s 4.66%. BTC behaves like digital gold; ETH behaves like productive capital.

Why is ETH leaving exchanges faster than bitcoin?

ETH exchange balances have declined 18% versus BTC’s 1.5%. The difference is driven by ETH’s utility: supply flows into staking contracts, DeFi protocols, and institutional custody. BTC primarily moves into cold storage and ETFs. ETH has more productive destinations competing for supply.

Which has a higher store-of-value potential, BTC or ETH?

By traditional store-of-value metrics (dormancy, low turnover, simplicity), BTC leads. Its behaviour maps to gold. ETH has a higher anchored float (25.1% vs 6.7%) but its supply is more active, with long-term holders mobilising at three times BTC’s rate. ETH stores value differently, through productive deployment rather than dormancy.

How do BTC and ETH ETF holdings compare?

BTC ETFs hold 6.7% of total supply. ETH ETFs hold 5.24%. The figures are in a similar range, but ETH’s total anchored float (25.1%) far exceeds bitcoin’s (6.7%) due to staking, which has no comparable bitcoin equivalent at scale.