Store of Value to Digital Oil: How Usage Differs Between BTC to ETH

ETH DeFi Collateral: 16% of Supply Powers Onchain Finance (2026 Data)

16% of all ETH in existence is locked inside DeFi protocols, liquid staking derivatives, and collateralised structures. No other major asset comes close to that level of productive deployment. This is not a side effect of ethereum. It is the point.

While bitcoin’s value proposition rests on dormancy, ETH’s rests on motion. On being the collateral layer that powers a multi-billion-dollar onchain financial system. The data paints a picture of an asset that earns its value by working.

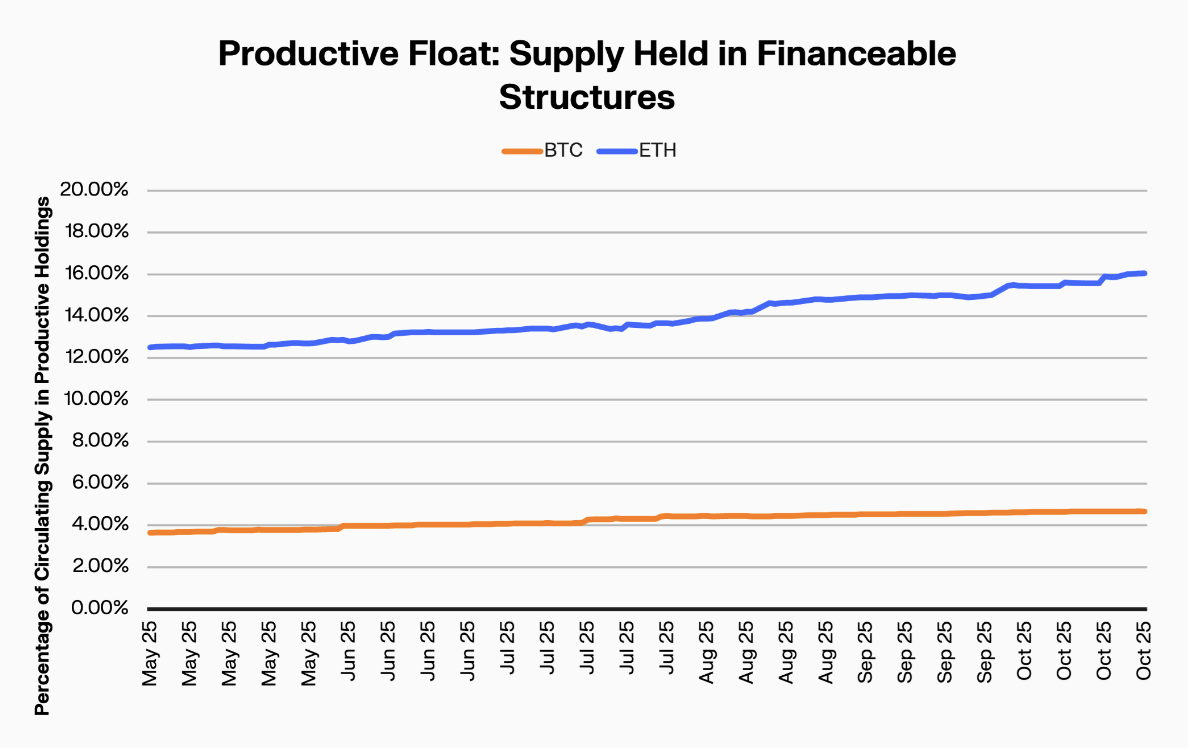

The Productive Float: 16.05% and What It Contains

Productive float measures supply actively generating yield, providing liquidity, or backing financial products onchain. For ETH, that number is 16.05%. For bitcoin, it is 4.66%.

That 3.4x gap is the single most important data point for understanding the difference between these two assets.

ETH’s productive float includes supply deployed across multiple layers of the onchain economy:

- Liquid staking: Protocols like Lido and Rocket Pool allow holders to stake ETH while receiving a liquid derivative (stETH, rETH) that can be redeployed as collateral elsewhere. One unit of ETH generates staking yield and serves as DeFi collateral simultaneously.

- Lending markets: Aave, Compound, and Morpho accept ETH as collateral for borrowing stablecoins and other assets. Deposited ETH earns lending yield while enabling leverage across the ecosystem.

- Liquidity provision: Decentralised exchanges like Uniswap and Curve require ETH in trading pairs. Liquidity providers earn fees from every swap their capital facilitates.

- Collateralised structures: ETH backs synthetic assets, structured products, and cross-chain bridges. Each layer locks supply while generating economic activity.

Compare that to BTC’s productive float of 4.66%, which largely consists of wrapped BTC on ethereum and early-stage bitcoin DeFi protocols. The infrastructure exists. The adoption lags by a full cycle.

Why ETH Became the Default Collateral Layer

ETH’s dominance as DeFi collateral is not accidental. Three structural factors drive it.

First, native programmability. Ethereum’s smart contract architecture allows ETH to interact natively with every protocol built on the network. No wrapping. No bridging. No trust assumptions beyond the base layer. BTC requires wrapping (wBTC, tBTC) or cross-chain infrastructure to participate in DeFi, adding complexity and counterparty risk.

Second, the staking flywheel. Since the merge, ETH generates native yield through proof-of-stake validation. Liquid staking derivatives turn that yield into composable collateral. A holder stakes ETH, receives stETH, deposits stETH into a lending protocol, borrows against it, and deploys the borrowed assets elsewhere. One unit of ETH powers multiple layers of financial activity.

Third, the reflexive demand loop. Every new DeFi protocol creates incremental demand for ETH as collateral. As DeFi grows, more ETH gets absorbed into productive structures, tightening the free float available on exchanges. Reduced exchange supply can drive price appreciation, which increases the value of existing ETH collateral, which enables more borrowing and deployment.

The Composability Multiplier

In traditional finance, collateral sits in one place and does one job. In DeFi, ETH collateral can be rehypothecated across multiple layers simultaneously.

A single ETH token can:

- Be staked to secure the network (earning ~3-4% annually)

- Generate a liquid staking token (stETH) that trades at near parity

- Serve as collateral in a lending protocol (earning additional yield)

- Back a loan denominated in stablecoins

- Have those stablecoins deployed into another yield opportunity

This composability multiplies the economic output of each unit of ETH. It also multiplies risk. Smart contract vulnerabilities, oracle failures, and liquidity cascades can unwind layered positions rapidly. The simplicity of bitcoin’s dormancy model exists precisely because it avoids this complexity.

But the market has spoken with its capital. 16% of ETH supply is deployed in these structures. Holders accept the risk premium because the returns justify it.

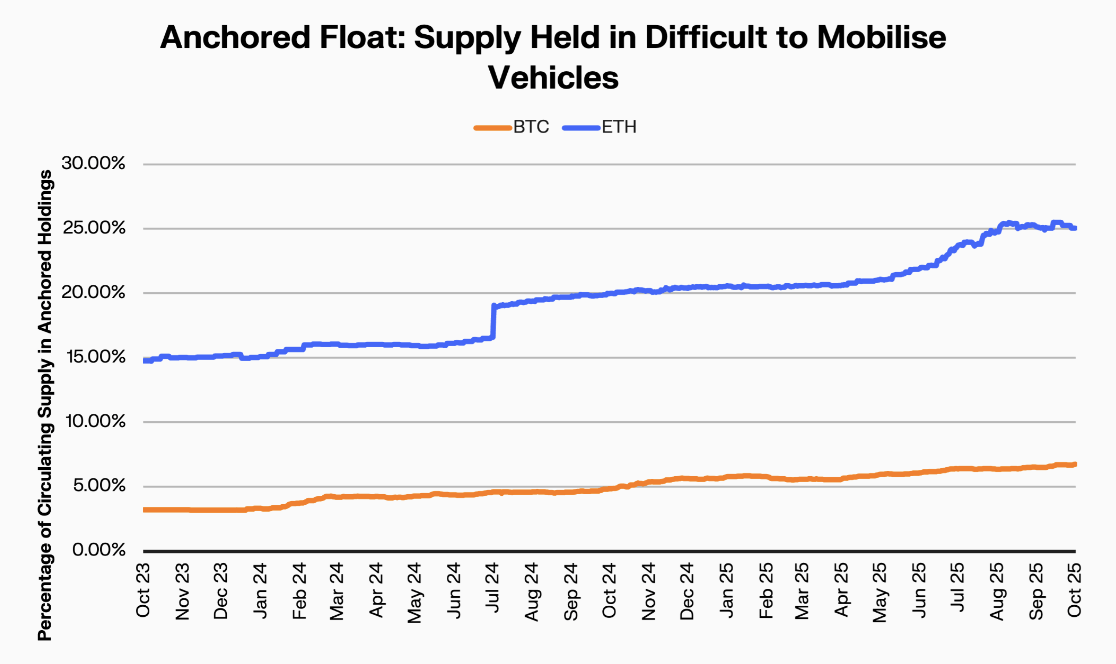

The Anchored Float Context

ETH’s anchored float sits at 25.1%. That includes ETF holdings (5.24% of supply), staking, and institutional custody. Add the productive float of 16.05%, and over 40% of ETH supply is either locked or actively deployed.

The remaining ~60% constitutes the truly free float: supply on exchanges (11.3%), in personal wallets, and in various states of readiness.

For BTC, the anchored float is 6.7% and the productive float is 4.66%. Combined, roughly 11% is locked or deployed. But 61% of supply has not moved in over a year. Bitcoin’s “lock-up” is voluntary. Behavioural, not mechanical.

ETH’s is both. Mechanical lock-ups through staking and DeFi complement behavioural holding among long-term participants. The result is a tighter effective free float than raw numbers suggest.

ETH's DeFi Supply vs Traditional Asset Comparisons

No traditional asset deploys 16% of its supply in productive financial structures. Gold sits in vaults. Government bonds sit in custody accounts. Even equities, which can be lent for short-selling, see utilisation rates well below 16% for most stocks.

ETH has created a new category. A monetary asset where a significant share of supply is structurally embedded in financial infrastructure. Not just held. Not just traded. Put to work.

Fidelity’s assessment that ETH “can serve as medium of exchange and store of value” captures part of this picture. But it understates the third dimension. ETH also serves as productive collateral. A yield-generating, liquidity-providing, composable financial primitive.

The Risk Side of the Ledger

16% of supply in DeFi means 16% of supply exposed to smart contract risk, governance attacks, oracle manipulation, and liquidity crises. This is not a theoretical concern.

Past incidents have demonstrated how quickly collateral cascades can unwind. When stETH temporarily depegged during the 2022 credit crisis, the ripple effects moved through every protocol where it served as collateral. Positions were liquidated. Liquidity dried up. The composability that multiplied returns also multiplied contagion.

This risk profile is why bitcoin purists reject the productive-asset model entirely. A store of value should store value. Full stop. Adding yield mechanics introduces failure modes that gold and dormant BTC simply do not have.

The counter-argument: risk is priced. ETH holders who deploy into DeFi earn returns that compensate for smart contract exposure. The 16% productive float is not naive capital. It is capital that has evaluated the risk-reward and chosen deployment over dormancy.

What the Productive Float Means for ETH's Future

If DeFi continues to grow, the share of ETH supply in productive structures will expand. Restaking protocols like EigenLayer add new layers of yield and utility on top of existing staking positions. Every protocol innovation creates another use case for ETH collateral.

The ceiling is not obvious. Could 25% of ETH end up in DeFi? 30%? The onchain behaviour comparison shows that ETH’s trajectory diverges sharply from bitcoin’s, and the productive float is the engine of that divergence.

For institutional allocators evaluating ETH, the productive float is the differentiator. It transforms ETH from a speculative asset into an income-generating one. Corporate treasuries, endowments, and sovereign funds that hold ETH can stake and earn. That changes the calculus entirely.

ETH is not digital gold. It is digital oil. And 16% of its supply is already in the refinery.

FAQ

How much ETH is locked in DeFi?

16% of total ETH supply is deployed in DeFi protocols, liquid staking derivatives, and collateralised structures. This includes lending markets (Aave, Compound), liquidity pools (Uniswap, Curve), liquid staking (Lido, Rocket Pool), and cross-chain bridges. The productive float of 16.05% compares to bitcoin’s 4.66%, a 3.4x difference.

Why is ETH used as DeFi collateral more than bitcoin?

Three reasons: native programmability (ETH interacts directly with smart contracts without wrapping), the staking flywheel (proof-of-stake yield creates composable liquid staking tokens), and reflexive demand (more DeFi protocols means more demand for ETH collateral). BTC requires wrapping (wBTC) or bridges to participate in DeFi, adding friction and counterparty risk.

What is productive float in crypto?

Productive float measures the share of an asset’s supply actively deployed in yield-generating, liquidity-providing, or collateral-backing activities within the onchain economy. ETH’s productive float is 16.05%; bitcoin’s is 4.66%. The metric distinguishes between supply that is simply held (dormant) and supply that is working within financial protocols.

Is ETH a store of value or a utility token?

ETH functions as both. One in four tokens are locked in staking or ETFs (store-of-value behaviour), while 16% of supply is actively deployed in DeFi and collateralised structures (utility behaviour). Fidelity describes ETH as capable of serving as “medium of exchange and store of value.” The data supports a dual identity rather than a single classification.