Onchain Asset Management: Designing the Future of Investment Strategies

DeFi Asset Management Growth: $64B by 2026, 56.4% CAGR Forecast

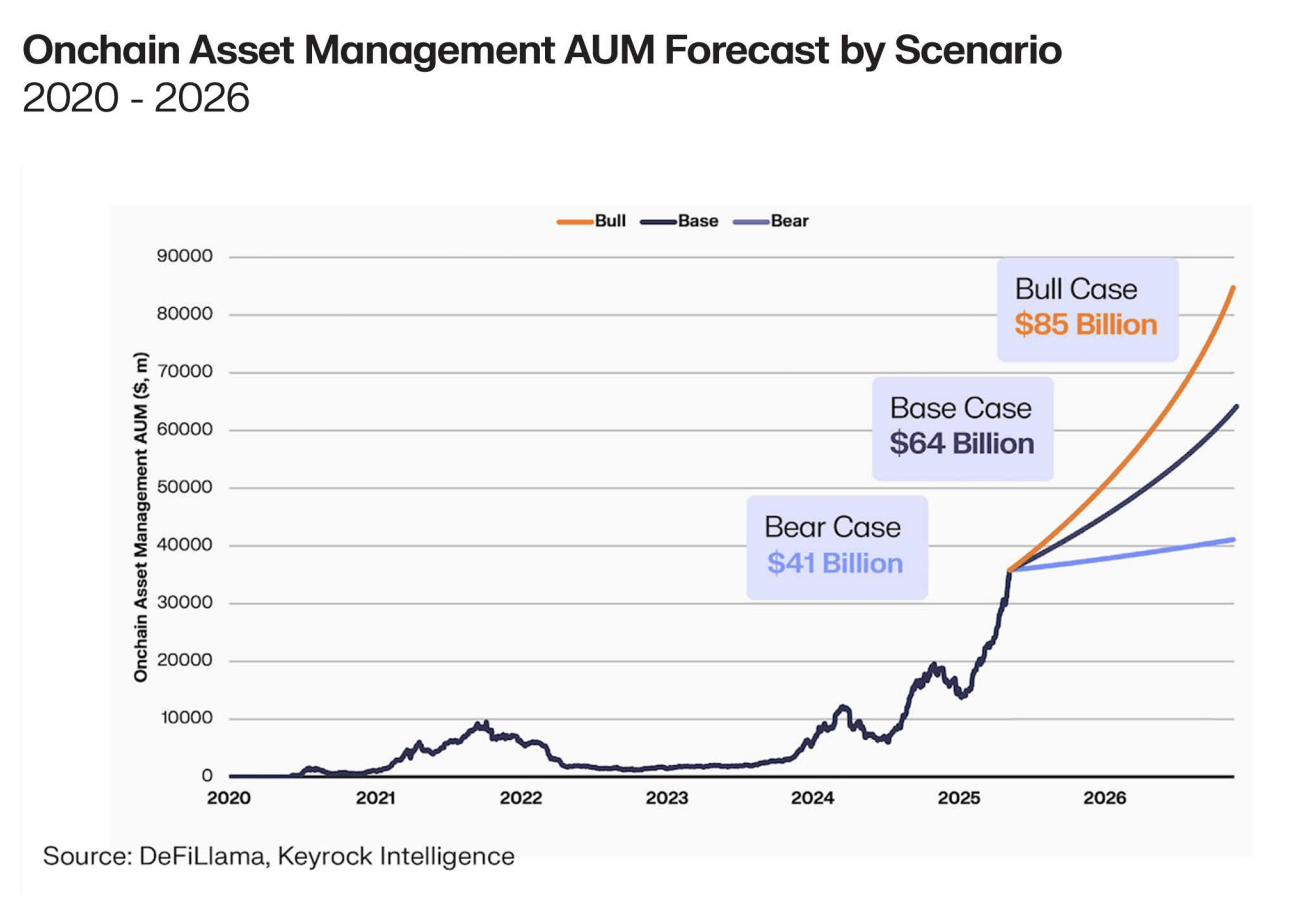

$35 billion today. $64 billion by end-2026. That is the base case. The bull case reaches $85 billion. Either scenario represents a fundamental repricing of how much capital the world is willing to deploy through programmable, transparent infrastructure.

A 56.4% compound annual growth rate. Not in speculation. In managed assets generating real yield through verifiable strategies.

The Forecast Framework

Projecting onchain AUM growth requires modelling three variables: inflow of new capital, compounding of existing capital, and the rate at which traditional allocators migrate to onchain infrastructure.

The base case ($64 billion by end-2026) assumes:

- Continued institutional adoption at current growth rates

- No major adverse regulatory events that restrict onchain fund operations

- Protocol infrastructure continues maturing without systemic smart contract failures

- Stablecoin supply growth supports capital formation for onchain strategies

The bull case ($85 billion) layers on:

- Accelerated regulatory clarity in major jurisdictions (US, EU, UK)

- One or more major TradFi asset managers launching onchain products at scale

- Tokenised real-world assets growing fast enough to expand the collateral base significantly

- A sustained bull market in crypto assets that attracts new capital to the ecosystem

Neither scenario requires miracles. Both extrapolate from observable trends.

From $35 Billion to $64 Billion: The Math

118% YTD growth in 2025 puts the current trajectory well above the base case. But growth rates compress as the base expands. Moving from $5 billion to $10 billion is easier than moving from $35 billion to $70 billion. The law of large numbers applies.

A 56.4% CAGR over the projection period accounts for this deceleration. It assumes:

- Organic compounding — existing strategies generating 5–15% yields that compound within the ecosystem

- Net new inflows — fresh capital from institutional allocators discovering product-market fit

- Strategy proliferation — new protocol categories that do not exist today attracting incremental AUM

- Migration from CeFi — capital moving from centralised yield platforms to non-custodial onchain alternatives

The 56.4% figure is conservative relative to 2025’s 118%. But it is aggressive relative to traditional asset management growth. The difference is structural: onchain strategies are building into whitespace that traditional funds cannot access.

Five Catalysts for the Next Phase

1. Regulatory Clarity

Uncertainty is the largest single barrier to institutional capital entry. Every week that passes without adverse regulation represents capital that moves from “interested but waiting” to “allocated.” The EU’s MiCA framework, evolving US guidance, and progressive approaches in jurisdictions like the UAE and Singapore each unlock incremental capital pools.

2. Tokenised Real-World Assets

The tokenised assets market is projected to reach hundreds of billions. Every tokenised treasury, bond, or credit instrument that arrives onchain becomes raw material for yield strategies, structured products, and credit protocols. The collateral base expands. The strategy space expands with it.

3. Institutional Infrastructure

Custody solutions, compliance wrappers, institutional-grade wallets, and regulated onramps remove friction for the next tier of allocators. Each infrastructure layer that matures converts a segment of traditional capital from “cannot access” to “ready to deploy.”

4. Stablecoin Growth

Stablecoin supply growth directly correlates with onchain AUM capacity. More stablecoins in circulation means more capital available for deployment into yield strategies, credit pools, and structured products. The stablecoin and onchain asset management flywheel reinforces itself.

5. Performance Track Record

Time builds trust. Every quarter that onchain strategies deliver consistent, auditable returns adds another data point for institutional due diligence teams. The 186 basis point outperformance in automated vaults becomes harder to ignore as the track record lengthens.

Where Growth Concentrates

Not all strategy categories grow equally. Based on current trajectories and structural advantages:

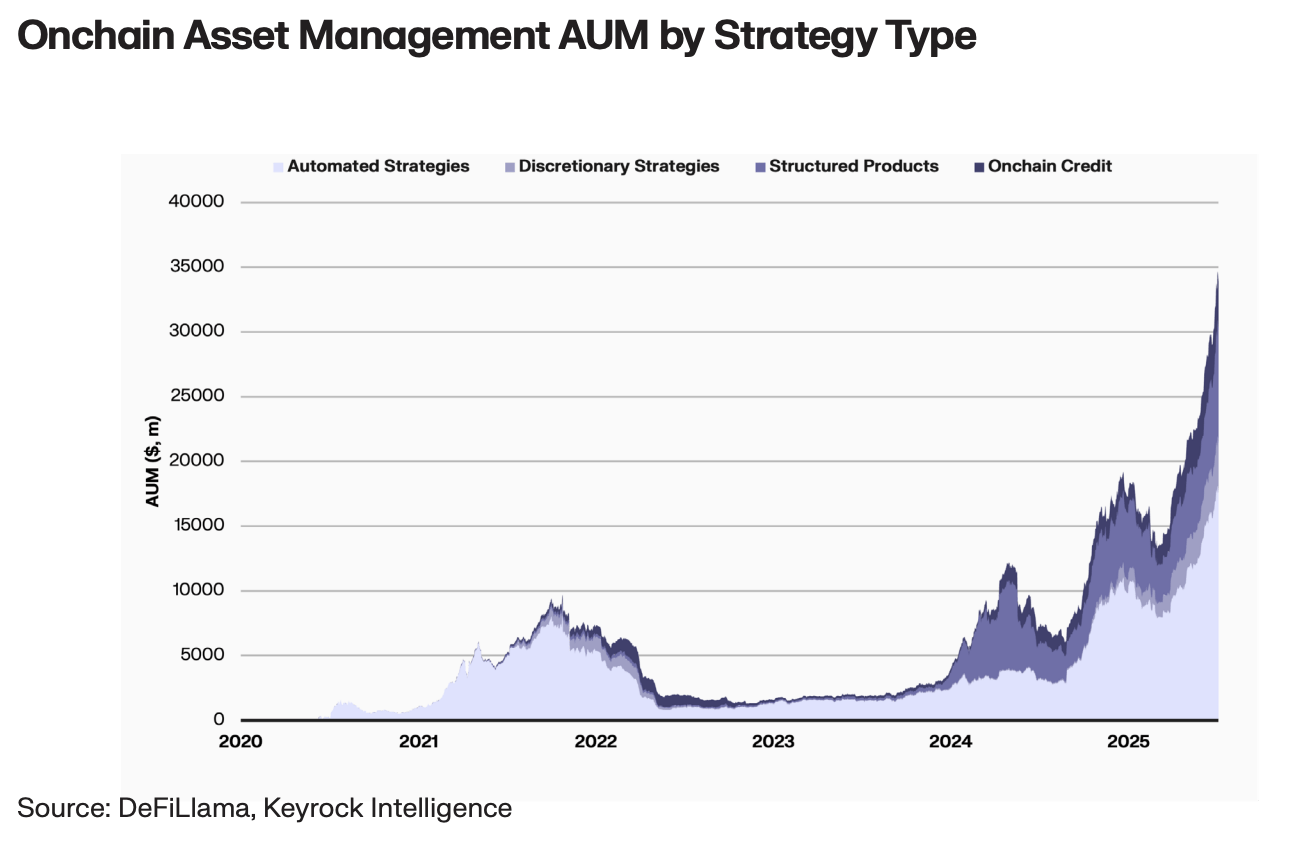

- Automated yield vaults — remain the largest category. Currently $18 billion. Projected to maintain 45–55% share as the simplest onramp for new capital.

- Structured products — fastest percentage growth as yield tokenisation attracts fixed-rate seekers from traditional markets

- Discretionary strategies — steady growth as Gauntlet, MEV Capital, and new entrants prove their track records match TradFi hedge funds

- Onchain credit — growth tied to tokenised collateral expansion and institutional borrower adoption

The protocol landscape will also shift. Morpho, Pendle, and Maple currently hold 31% of all AUM. As the market grows, new protocols will emerge and the concentration may dilute. Or the winners may compound their advantages. Both scenarios are consistent with the $64 billion aggregate target.

Capital Composition: Who Drives the Next $30 Billion

Today, whales and dolphins supply 70–99% of onchain AUM. That concentration pattern likely persists in the base case. But the composition of those large allocators shifts:

- Crypto-native treasuries — DAOs, protocols, and crypto companies deploying treasury assets

- Family offices — early adopters among traditional wealth seeking uncorrelated yield sources

- Asset managers — traditional fund managers launching onchain products or allocating to existing strategies

- Corporate treasuries — companies holding stablecoins for operational purposes deploying idle capital

The bull case ($85 billion) specifically requires at least one major institutional category — pension funds, sovereign wealth, or large asset managers — to move from exploration to meaningful allocation. That has not happened yet. When it does, the growth rate re-accelerates.

Risks to the Forecast

Models break. Forecasts fail. The path to $64 billion is not guaranteed. Key risks:

- Regulatory clampdown — adverse legislation that restricts onchain fund operations in major jurisdictions

- Smart contract exploit — a systemic failure in a major protocol (Morpho, Pendle, or Maple) that destroys confidence

- Macro risk — a severe crypto bear market that reduces total crypto AUM and investor appetite simultaneously

- Stablecoin depegging — a major stablecoin failure that disrupts the capital base for all onchain strategies

- Competition from TradFi — traditional funds co-opting the onchain model faster than native protocols can scale

Each risk has historical precedent. The 2022 cycle saw multiple protocol failures, a stablecoin collapse (UST), and a crypto winter that compressed AUM severely. The market recovered and grew 118% YTD. Resilience is demonstrated, not assumed.

The Tokenisation Convergence

The most powerful growth driver may be the convergence of onchain asset management with tokenised real-world assets. As traditional assets — treasuries, corporate bonds, private credit, real estate — move onchain, they become composable with existing DeFi infrastructure.

A tokenised treasury bill can be deposited into a Morpho vault. A tokenised corporate bond can serve as collateral in a Maple lending pool. A tokenised real estate cash flow can be split via Pendle into principal and yield components.

Each tokenised asset expands the strategy design space. The $35 billion ecosystem is built primarily on crypto-native assets today. When traditional assets arrive at scale, the addressable opportunity multiplies.

That multiplication is why the bull case reaches $85 billion. And why even that figure may prove conservative on a longer time horizon.

What Kevin de Patoul Sees

Kevin de Patoul, CEO of Keyrock, frames it directly: we have seen this evolution firsthand. From early yield aggregators to a full-spectrum investment management ecosystem. The trajectory is clear. The infrastructure is ready. The question is pace, not direction.

When you build market infrastructure for a living — as Keyrock does across crypto markets globally — you recognise inflection points. Onchain asset management passed its inflection point in 2024. Everything now is growth rate, not existence proof.

Frequently Asked Questions

How large will onchain asset management be by 2026?

The base case projects $64 billion in total onchain AUM by end-2026, representing a 56.4% compound annual growth rate from the current $35 billion. The bull case reaches $85 billion, assuming accelerated regulatory clarity and major institutional entrants. Both scenarios extrapolate from current growth trends with appropriate deceleration assumptions.

What is driving DeFi asset management growth?

Five primary catalysts: regulatory clarity in major jurisdictions, growth in tokenised real-world assets expanding the collateral base, institutional infrastructure maturation (custody, compliance, onramps), stablecoin supply growth supporting capital formation, and lengthening performance track records that satisfy institutional due diligence requirements.

Is a 56.4% CAGR realistic for onchain AUM?

Current 2025 growth stands at 118% YTD, well above the 56.4% CAGR projected forward. The forecast accounts for growth deceleration as the base expands — moving from $35 billion to $64 billion requires more absolute capital than earlier doublings. The projection is conservative relative to current momentum but aggressive relative to traditional asset management norms.

What could prevent onchain AUM from reaching $64 billion?

Key risks include adverse regulation restricting onchain fund operations, a systemic smart contract exploit destroying confidence, severe crypto bear market reducing total ecosystem capital, a major stablecoin failure disrupting the capital base, or traditional finance co-opting the onchain model faster than native protocols can scale.