Onchain Asset Management

Credit Strategies in Onchain Asset Management. A guide

Defining Onchain Credit Strategies

At their core, onchain credit strategies are strategies that involve lending capital onchain, underwriting credit risk, and structuring debt instruments via smart contracts. This can take several forms, such as unsecured or permissioned lending pools on Maple or Clearpool, tranching of risk into senior or junior pools or credit derivatives, or even niche asset-specific pools such as NFT backed loans on Gondi.

Borrowers will tap liquidity directly from pools or vaults, while investors, in this case our lenders, earn yield based on predefined, either static or dynamic, credit terms, enforced by smart contracts. Typically, these smart contracts control liquidation mechanisms in which the collateral is custodied by the smart contract and distributed to the lender in the event of a failure to repay. The result is that we end up with traditional credit functions, such as origination, underwriting and syndication, onchain, with more transparency and programmability than traditional alternatives.

Onchain credit sits at the debt capital markets layer of DeFi, providing the rails for lending and borrowing beyond simple overcollateralised loans. Protocols like Maple, Clearpool, Goldfinch, and Gondi match stablecoin liquidity with borrowers ranging from trading firms to NFT holders, using permissioned pools, whitelisting, or novel collateral frameworks. These markets integrate directly with the broader DeFi stack in that loans are denominated in stablecoins, claims on pools are tokenised, and vault infrastructure can package credit exposures into structured strategies.

History and Evolution of Onchain Credit Strategies

The origins of onchain credit in an asset management context, i.e. post-overcollateralised peer-to-peer vanilla lending like Aave, came when protocols like Maple and Goldfinch emerged to bring unsecured and RWA-backed lending onchain. Maple pioneered whitelisted institutional credit pools, where lenders could underwrite trading firms and market makers using stablecoin deposits, while Goldfinch sought to expand access to emerging-market borrowers via tokenised credit lines. These early experiments tested whether trust could be replicated onchain not only through collateral, but through governance, legal agreements, and delegated risk managers.

By 2023, the limits of that model were stress-tested through bear markets. Several pools faced defaults, underlining both the promise and the risks of permissioned credit. Yet the resilience of the framework, with tokenised claims, transparent pool-level data, and automated repayment flows, proved attractive enough to institutional allocators that development continued. Clearpool refined the concept further, offering pools of unsecured lending to vetted borrowers with tokenised LP shares providing tradable exposure.

In parallel, a more experimental branch of onchain credit emerged, namely NFT-backed lending. Platforms like Gondi and others introduced collateralised loans against digital art and collectibles, building liquidity for previously illiquid assets. While niche, these experiments showcased the extensibility of the model. If you can tokenise an asset, you can lend against it, and structure repayments programmatically. This also creates a direct tie between these onchain credit protocols and the growth of digital art and collectibles, an asset class that’s currently unserved elsewhere.

Fast forward to 2025, and onchain credit has become one of the fastest-growing segments of decentralised asset management. Maple’s syrupUSDC vault, with instant-liquidity wrappers on Uniswap and Balancer, has redefined how stablecoin float can be deployed, combining competitive yield with withdrawal flexibility. Institutions now view permissioned credit pools as a regulated, transparent alternative to private debt funds, while DAOs and treasuries increasingly deploy idle stablecoin reserves into these products. At the same time, NFT credit and RWA lending continue to expand the boundaries of what qualifies as collateral.

This article is a part of a series on Onchain Asset Management.

The Rise of SyrupUSDC: The AUM Growth of Onchain Credit Strategies

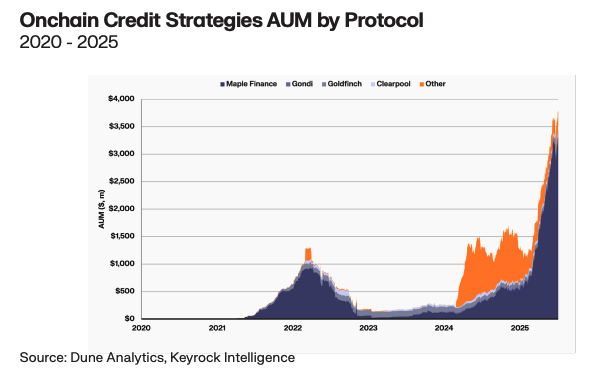

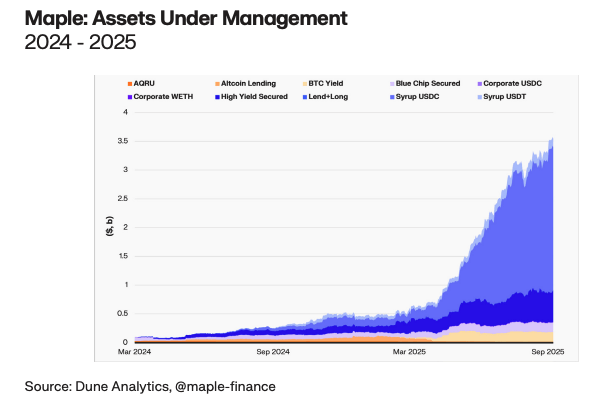

Onchain credit has staged one of the most impressive rebounds in the asset management stack. After the collapse of early unsecured lending experiments in 2022, AUM contracted sharply, leaving doubts about whether the model could recover. The past 18-months have answered that question, with Maple Finance re-emerging as the anchor protocol, driving its own AUM above $3 billion, and total strategy AUM close to $4 billion. Maple’s AUM growth has been supported by innovations such as syrupUSDC, which introduced fungibility and liquidity into what was once a bespoke, illiquid product set. Alongside Maple, newer entrants such as Gondi have carved out a crypto-native niche by using NFTs as collateral, broadening the definition of credit markets onchain.

There has been a shift in composition, where Clearpool and Goldfinch once commanded their own corner of the market on 2022, Maple now dominates. We also see the ‘Other’ category, a concoction of experimental protocols, has fallen to near-zero levels as Maple’s dominance has risen.

Comparing Onchain Credit Strategies to Traditional Finance Counterparts

Onchain credit strategies represent lending and borrowing markets where investors provide capital directly to borrowers in exchange for yield, typically with the sourcing and placement of capital occurring onchain. These strategies span overcollateralised lending, unsecured corporate credit, DAO and protocol treasury loans, RWA financing, and NFT-backed lending. Their aim is to take the advantages of onchain lending protocols, and apply them more broadly with complex implementations, as well as to offchain projects, thereby broadening access to borrowers while offering lenders higher returns. Allocators include a mix of retail users in permissionless pools, DAOs managing treasury capital, and institutions participating in permissioned, underwritten credit markets.

Onchain credit yield is generated primarily from lending against digital collateral, often overcollateralised loans secured by stablecoins or liquid tokens, with interest paid directly onchain. Traditional finance private credit sources yield from extending loans to corporates, SMEs, or real estate projects, often unsecured or lightly collateralised but backed by legal contracts and covenants.

For onchain credit, the mapping to traditional finance is relatively direct, though with important nuances. The closest parallels lie in Private Credit Funds (PCFs), particularly those focused on direct lending. In addition to this, we explore Marketplace or Peer-to-Peer Lending Platforms (P2Ps) and High-Yield Corporate Bond Funds (HYFs).

| Potential Comparator | Comparative Relevance | Comparative Shortcomings | Overall Suitability |

| Private Credit Funds (PCFs) | Provides loans directly to corporates, SMEs, or specialised borrowers. Similar mandate to onchain credit pools. | Monthly or quarterly lock-ups versus instant liquidity onchain, low transparency, not permissionless, requires centralised underwriting. | Primary comparator |

| Peer-to-Peer Lending Platforms (P2Ps) | Retail-facing, permissionless in nature, connects lenders and borrowers directly. Mirrors user-driven onchain credit. | Centralised intermediaries, no composability, lower transparency vs. onchain credit. | Reasonable comparator |

| High-Yield Corporate Bond Funds (HYFs) | Capture higher yields through exposure to riskier debt, broadly reflecting similar risk and return profiles to some onchain pools. | Publicly traded and liquid. Exposure through bonds, not direct lending, is less idiosyncratic. | Less reasonable comparator |

For onchain credit strategies, the primary comparator is PCFs, specifically direct lending vehicles. While private credit, a $1.6 trillion industry, operates at a far greater scale, both strategies share the economic function of generating yield by underwriting loans to corporates or individuals, with returns driven by credit spreads. Similar to onchain pools, PCFs operate with relatively illiquid exposures and require active monitoring of borrower performance. The key difference lies in transparency, where private credit funds typically disclose performance quarterly and behind paywalls, while onchain credit allows lenders and prospective lenders to track every loan, repayment, and default in real time.

Given the close comparisons between onchain credit strategies and PCFs, this report will directly compare the two, while still leveraging weighted averages for fee and performance comparisons, in conjunction with qualitative assessment.

Benefits and Drawbacks of Onchain Credit Strategies Relative to Traditional Finance Counterparts

Onchain credit strategies preserve the essential value proposition of private credit, in that they generate yield from lending to businesses and institutions, while stripping away many of the frictions and inefficiencies that define the traditional model. Accessibility is perhaps the clearest differentiator. Traditional private credit funds typically require investment minimums in the range of $5-10 million, locking out all but the largest allocators. Onchain products, however, often lower the barrier to entry by several orders of magnitude, with thresholds measured in thousands or even hundreds of dollars. Combined with the permissionless nature of decentralised finance, this opens the asset class to a far broader allocator base, including DAOs and retail, while retaining institutional relevance.

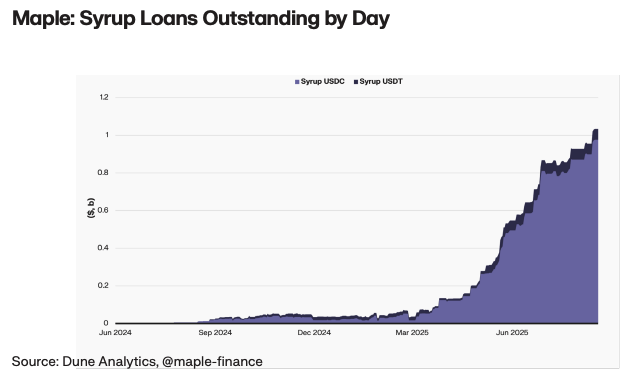

Liquidity and transparency provide further advantages. In private credit, lock-ups of three to seven years are standard, and reporting cycles are limited to monthly, quarterly or semi-annual windows, with loan-level detail hidden behind NDAs and manager discretion. Onchain, these constraints dissolve. Lock-ups can be non-existent in products such as Maple’s syrupUSDC, while pool exposures, repayments, and defaults are visible onchain in real time. Tokenisation such as syrupUSDC further enhances this model by compressing reporting lag from quarters to blocks, and by allowing lenders to enter and exit positions programmatically.

The efficiency gains extend to the operation of the strategies themselves, with smart contracts automating repayment flows and interest accrual, reducing administrative overhead and stripping out layers of intermediation that in traditional funds justify additional fees. Moreover, the tokenised nature of onchain credit positions means they can be rehypothecated across DeFi. LP tokens can serve as collateral in lending protocols, be traded in secondary markets, or even be integrated into structured products. This composability transforms credit exposures into versatile building blocks, enabling capital to work across multiple venues simultaneously.

Perhaps the most compelling innovation lies in the treatment of default risk. In traditional credit markets, collateral recovery is slow and uncertain, with processes such as liquidating real estate dragging out for months or years. Onchain, this risk is dramatically reduced through the integration of smart contract logic and collateral custody. Should default conditions be met, assets are transferred automatically and instantaneously to lenders, eliminating the delay and uncertainty that characterise enforcement in traditional markets. This structural edge, combined with transparency and efficiency, positions onchain credit as a credible and scalable alternative to one of traditional finance’s fastest-growing asset classes.

Despite the benefits of onchain credit, which are primarily centered around the product, there still remains a number of drawbacks that stem primarily from the nascency of the industry. The most significant here is the borrower pool size and diversity. Not only is the borrower pool far smaller than in traditional private credit, the majority of lenders are crypto-native, given the requirement to be comfortable with onchain mechanics when depositing to onchain credit strategies. These crypto-native lenders span DAO Treasuries, small crypto-native investment firms, and a handful of FinTech lenders. Private credit, on the other hand, spans borrowers across product type, industries and geographies, giving allocators better diversification.

Another consideration for onchain credit strategies is that credit underwriting depth is typically narrower than in traditional private credit. While protocols like Maple and Clearpool employ whitelisting and professional underwriters, underwriting data onchain is less standardised and occasionally left to the discretion of the lender. On the flip side, traditional lenders can leverage extensive financial statements, covenants, collateral appraisals and legal enforcement tools.

A risk that has been somewhat mitigated on chain is that of illiquidity. Private credit is also illiquid, but secondary markets and structured vehicles such as CLOs or BDCs provide more scale and optionality. Onchain, this has previously been an issue, but new structures such as syrupUSDC and similar vaults create more fungibility and liquidity for deposits to these types of strategies.

Of course, this risks section wouldn’t be complete without the mention of infrastructure and smart contract risk for onchain strategies, which primarily apply to credit strategies through the default mechanisms controlled by smart contracts. This is seen by some as a benefit, in that defaults are settled almost instantly in the event conditions are met, although it does introduce another layer of potential exploitation.

Onchain Credit Strategies Fees and Performance

As mentioned in our previous sections, when comparing onchain credit strategies to traditional finance, we’ve opted to compare to private credit. Both seek to generate yield by underwriting loans to corporates, institutions, or individuals.

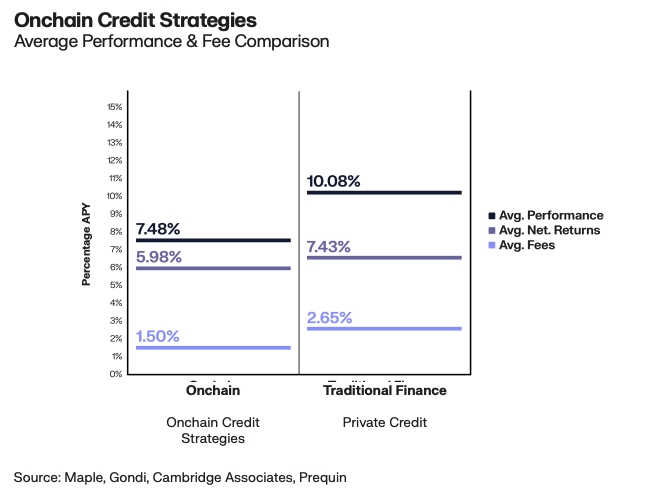

Onchain credit delivered a weighted-average gross return of 7.48%, versus 10.08% for the private credit funds in our benchmark group. Within DeFi, returns typically vary by pool type. Maple’s flagship syrupUSDC pool, with over $3 billion in deposits, generated 7.00%, while its High Yield pool delivered 10.20% on a much smaller $592 million base. By contrast, private credit funds like Blackstone’s Private Credit Fund, managing over $72 billion, or Oaktree’s $6.2 billion Strategic Credit Fund, have been able to sustain high single-digit to low double-digit yields while operating at much larger scale. This highlights the core distinction that DeFi credit is still experimental and fragmented, while private credit in TradFi has matured into one of the largest and most reliable private market strategies.

Fees tilt the comparison in favour of DeFi. Onchain credit strategies average 1.50%, largely reflecting smart contract costs and leaner administration. Traditional private credit funds, by contrast, average 2.65%, with layers of management and servicing fees that reflect heavier operational structures. This cost efficiency is one of the clearest advantages of the onchain model, where origination, servicing, and even collateral liquidation can be automated programmatically.

After fees, private credit retains an edge, with net returns for our sample of funds averaging 7.43%, compared to 5.98% for onchain credit strategies. This suggests that while DeFi credit has structural advantages in efficiency and accessibility, it currently struggles to match the scale-adjusted performance of established private credit platforms. The ability of Blackstone, Oaktree, and KKR to deliver similar or higher returns while deploying billions underscores the institutional depth of traditional credit markets. That said, onchain credit offers benefits that TradFi cannot replicate such as real-time transparency, permissionless access, and composability, features that may grow in importance as these products mature and attract a wider allocator base.

Allocator Profiles to Onchain Credit Strategies

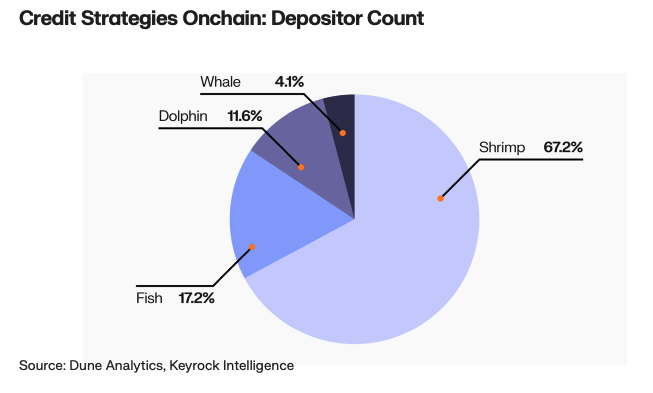

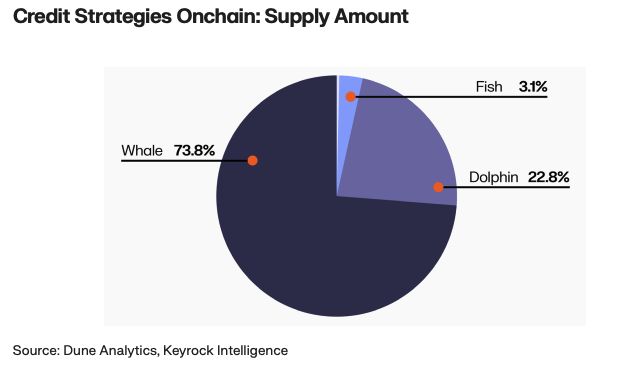

When looking at the depositor count to onchain credit strategies, we see primarily retail users interacting with Maple Finance’s syrupUSDC product, as shown by the fact that 67% of this audience are categorised as Shrimps, defined as depositors of under $10k. Access models reflect the risk in the pool, with unsecured corporate lending being whitelisted, while NFT- or RWA-backed lending tends to be permissionless. This segmentation has allowed onchain credit to serve both sides of the market, those seeking institutional-grade credit exposure and those experimenting with new collateral types.

Of course, the permissionless side of these markets that attracts retail accounts only for a small portion of the total capital deployed to onchain strategies. Looking at the supply amount, we can see that the permissioned, larger depositors are allocating far more capital than the smaller depositors. Whales account for 74% of AUM in onchain credit. This better reflects the maturation of the onchain credit industry. Institutional players and protocol treasuries typically allocate tickets in the million dollar range, favouring permissioned pools with rigorous, institutional-grade borrower underwriting.

Catalysts for Onchain Credit Strategies Growth

The next leg of growth in onchain credit will likely be defined by institutionalisation and composability. On the institutional side, regulatory clarity is already enabling banks, fintechs, and credit funds to participate in permissioned pools, with Maple and Clearpool showing the model works at scale. As regulatory pilots in the US, UK, and Singapore mature, we should expect larger tranches of private credit to migrate onchain, particularly in shorter-duration corporate lending where transparency and operational efficiency are decisive advantages. Tokenised wrappers such as syrupUSDC are critical here, creating liquid entry and exit points that transform what was once a multi-year commitment into a yield-bearing, tradable instrument.

At the same time, onchain credit is becoming increasingly composable with the rest of DeFi. Lending positions that once sat siloed within closed funds can now be tokenised and rehypothecated across money markets, DEXs, and structured product vaults. This composability multiplies utility, where a credit LP token might simultaneously generate yield, serve as collateral, and form part of a hedged structured strategy. As standards like ERC-4626 proliferate, integration costs fall, opening the door to fund-of-funds models and dynamic credit portfolios that would be operationally impossible in Traditional Finance.

New borrower segments also represent an underappreciated catalyst. Beyond institutional unsecured pools, protocols like Gondi are proving that NFT-backed lending can be scaled transparently, carving out niches in digital asset financing that do not exist in traditional markets. Combined with falling operational frictions, this diversity of collateral types should deepen liquidity and attract more sophisticated lenders into the ecosystem.

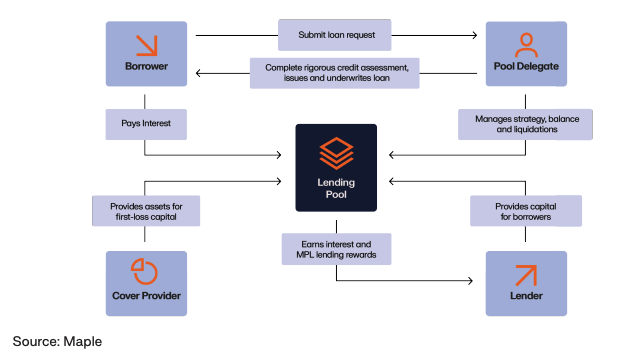

Launched in 2021, Maple Finance built institutional-grade onchain lending infrastructure that epitomises onchain asset management. Founded with the goal to bring DeFi lending beyond legacy, closed systems, Maple has since facilitated over $9 billion in loans across hundreds of institutional participants, making it the largest onchain asset manager provider to date. As Maple themselves put it in an interview with Keyrock, “Maple has now originated over $9bn in loans through our smart contract infrastructure. Each of these loans has the unique feature of being fully verifiable onchain. Lenders are able to see the loan terms, loan status and repayments.”

The platform itself serves a dual-role, with the protocol layer serving as a permissioned marketplace where institutions can underwrite pooled credit with whitelisted borrowers. The capital deployment layer, on the other hand, via its own products like syrupUSDC, offers liquid, aggregated exposure to credit strategies built onchain.

We see Maple as a critically important protocol for the evolution of onchain asset management. It catalysed a move of DeFi credit away from purely retail focused crypto-native borrowers, towards institutional-quality lending. Maple was also one of, if not the, first protocols to introduce permissioned and whitelisted pools, emphasising the importance of compliance alignment to push the industry forward.

A core focus of Maple’s innovation has been their syrupUSDC product, offering yield-bearing derivatives for both USDC and USDT, though the market has primarily backed the USDC-implementation. Historically, onchain credit markets were illiquid and bespoke, but Maple’s syrupUSDC creates a fungible, instantly redeemable dollar yield instrument. In practice, this bridges the gap between short-term liquidity needs of lenders, and long-term credit exposure in a product that opens up credit market accessibility to a whole new cohort of allocators, and importantly, capital. On top of this, syrupUSDC is integrated into a handful of DeFi protocols, including but not limited to Pendle, Morpho, Euler, Jupiter and Kamino to provide additional yield composability and leverage.

Another feature that Maple worked into its product is the combination of traditional finance underwriting with DeFi composability, while maintaining overcollateralisation. Maple was able to combine traditional credit practices, ranging from due diligence and whitelisted borrowers to professional underwriting, with the permissionlessness and flexibility of DeFi. This essentially builds a hybrid model, in which the risk and learning curve associated with onchain protocols is somewhat mitigated by the recognisable, and reputable traditional finance practices, while still maintaining the value adds offered by onchain products. Maple referred to this point specifically in our interview, “we view these as complimentary rather than in competition with each other. The more we innovate and improve our technology the more we are able to scale without compromising on our credit management and underwriting standards.”

While not exclusive to Maple, this hybrid approach still enables the transparency of borrower performance, defaults, repayments, and pool health that enable real-time monitoring. Allocators can see risks as they emerge, not in quarterly reports offered by traditional finance counterparts. We strongly believe this is the future for private credit, a hybrid system that merges the best of both worlds. Maple describes this as a structural advantage over Traditional Finance, “credit markets are opaque, unknown and inaccessible for the majority of investors today. Maple enables broad and distributed access to credit, removing the frictions of borders, investment minimums, and active removal of investors.”

The borrower profile on Maple has evolved significantly. What began with small, crypto-native firms has expanded into larger, publicly listed companies and multi-billion-dollar businesses. As Maple notes, “when Maple launched in 2021 we had a small number of crypto native firms that borrowed at small sizes. Today, Maple lends to public companies and multi billion dollar businesses. It shows the progress across the crypto industry and reinforces our long term belief that the financial system will move entirely onchain over the coming decade.”

Vaults like Maple’s have the potential to gain position amongst allocator portfolios as direct substitutes for short-term credit or money-market products. This is true across all allocator types, especially risk-adverse allocators like pension and insurance funds. By demonstrating regulatory alignment and delivering consistent yields, Maple can showcase that institutional-grade credit products work onchain, catalysing a wave of allocator participation.

Gondi is a decentralised, peer-to-peer, non-custodial NFT liquidity protocol that enables users to buy, sell, and borrow against NFTs. The component of this product that we’re particularly focused on is the borrowing, which can be structured as sophisticated onchain credit facilitation utilising crypto-native collateral, with the ability to refinance and the introduction of tranche seniority.

Unlike other credit protocols that anchor themselves in tokenised treasuries or whitelisted borrowers, Gondi leans fully into the crypto-native side of the spectrum. It treats NFTs as balance-sheet assets, enabling holders to unlock liquidity without intermediaries or custodians. In practice, that means a Chromie Squiggle or CryptoPunk can serve the same financial function as real estate or a stock portfolio, transforming the asset into a yield-bearing, loan-collateral asset class. With instant refinancing, programmable repayment mechanics, and full transparency on borrower behaviour, Gondi is pushing the frontier of what onchain credit can look like.

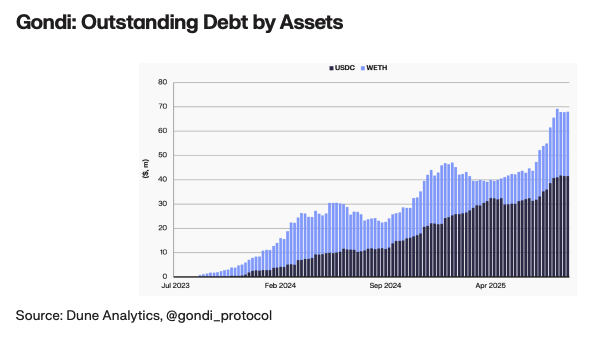

Gondi has seen phenomenal growth YTD, with outstanding debt, defined as the outstanding principal and interest for loans originated on Gondi, having grown 60.6% YTD to $69 million. The two loan denomination assets currently available on Gondi are USDC and ETH, with the former being the market preference at 60.1% dominance, highlighting the fact that despite the underlying NFT assets being typically valued in ETH-terms, these loans are utilised by investors seeking dollar-denominated returns.

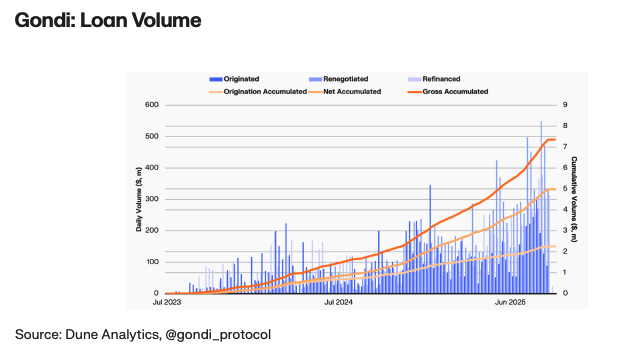

What’s interesting about the breakdown of this loan volume, is that the refinancing and renegotiation volumes now outpace new originations, which is an indication that the onchain, NFT-denominated credit markets are maturing. While early adoption was about proving that NFT-backed loans could work, the focus is now on optimising existing debt positions, much like traditional credit markets where refinancing dominates flows. In the same vein, this points to an enhancement of borrower sophistication, where borrowers are acting more strategically with their debt, rolling over or renegotiating terms instead of simply repaying or defaulting. Burga from Gondi touched on this by saying that, “Borrowers have evolved from short-term speculators to long-term holders using credit strategically. Early on, loans were often just hedges – a way to lever up or buy optionality. Now we see people using NFTs as collateral for meaningful life events such as buying homes, bridging a property sale, or funding projects.”

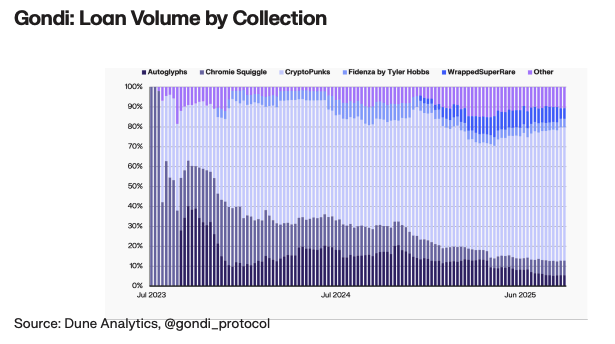

The rise in refinancing activity also reflects growing competition among lenders. Onchain credit allows a loan originated at one rate to be seamlessly refinanced if another lender offers better terms, creating a fluid, competitive environment that continuously improves borrower conditions. As Gondi themselves note, “we’ve seen the lender base at GONDI start to shift from individuals to professional funds underwriting at scale. As more capital enters, rates compress, and suddenly borrowing becomes attractive to a much broader group of holders. A 12% APR loan opens doors that a 25% loan never could. Equally important is what this refinancing trend says about collateral quality. The willingness to refinance against the same NFTs, rather than forcing liquidation, signals growing confidence in the durability of bluechip collections like CryptoPunks, Chromie Squiggles, and XCOPYs. Lenders increasingly treat these assets as reliable stores of value, stable enough to support multiple loan cycles. This evolution in perception has helped consolidate collateral flows around a handful of top-tier collections, a trend that becomes clear when loan volume is broken out by collection. As can be seen below, 97.2% of loan volume is concentrated in just five collections on Gondi, namely CryptoPunks, Chromie Squiggles, Autoglyphs, Wrapped SuperRare’s and Fidenza by Tyler Hobbs.

Another structural edge of onchain credit lies in its transparency. As Gondi put it, “onchain, every repayment, default, and underwriting decision is visible. Good actors rise to the top, bad actors can’t hide. That openness creates more trust and healthier competition than traditional credit ever allowed.” This dynamic enforces discipline among borrowers and lenders and accelerates market efficiency, with strong actors quickly building credibility, while weak actors are filtered out.

Looking ahead, the most important catalyst will be the scaling of liquidity, with Gondi noting, “the next catalyst is liquidity plus flexibility. As more capital flows in, we’ll see the mechanics that make onchain credit unique, like sale-and-repay, where an NFT can be sold mid-loan and the transaction automatically repays the lender, become widely adopted.” These trustless, atomic flows are impossible in traditional credit, but they reduce friction, expand optionality, and make it rational for more wealth to be held in digital assets. In the same way that access to cheap mortgages transformed real estate into a mass asset class, programmable credit could reinforce and accelerate the rise of digital assets as a mainstream store of value.