Prediction Markets: The Next Frontier of Financial Markets

Corporate Prediction Markets — Google, Microsoft, HP Case Studies (2026)

HP’s internal prediction market beat the company’s official forecasts 75% of the time. Not by a small margin — by 20-25% less forecasting error. Google ran prediction markets for two decades. Microsoft’s market spotted a doomed software project weeks before management acknowledged it. These are not theoretical outcomes. They are documented, repeated, and still underused.

For more than twenty years, Fortune 500 companies — Google, Microsoft, HP, Ford, Samsung, Best Buy, GE, Electronic Arts — have tested internal prediction markets to improve forecasting, reduce bias, and surface information that top-down planning processes miss. The results are unambiguous. Prediction markets belong in every large organisation’s decision-making toolkit.

The Premise: Skin in the Game Changes Everything

The concept is straightforward. Employees trade contracts on internal questions — product launch dates, sales targets, project timelines, hiring outcomes. Resulting prices reflect the organisation’s collective expectation.

The difference from surveys: prediction markets require participants to stake something on accuracy. Even virtual currency shifts incentives — from telling managers what they want to hear toward revealing what people actually believe will happen. That shift changes everything about the quality of information you receive.

Google: Prophit and Gleangen

Google has run the most extensive corporate prediction market programmes of any company. Prophit launched in 2005. Its successor, Gleangen, followed in 2020. Across both platforms, approximately 20% of Google employees participated — a remarkable adoption rate for any internal tool.

The range of topics traded:

- Product metrics: Gmail user counts, product release dates, feature adoption timelines

- Industry predictions: Whether Apple would switch to Intel chips (correctly predicted)

- Operational planning: Office reopening schedules during and after the pandemic

- Strategic questions: Competitive dynamics, partnership outcomes, market share shifts

Google’s internal research, documented by Bo Cowgill and others, found that prediction markets can “quantify beliefs” across large, distributed organisations in ways that surveys, executive committees, and traditional planning processes cannot. But one critical caveat emerged: markets must be explicitly linked to decisions to deliver full value. When they operated as standalone curiosities — interesting but disconnected from resource allocation — participation waned and accuracy suffered.

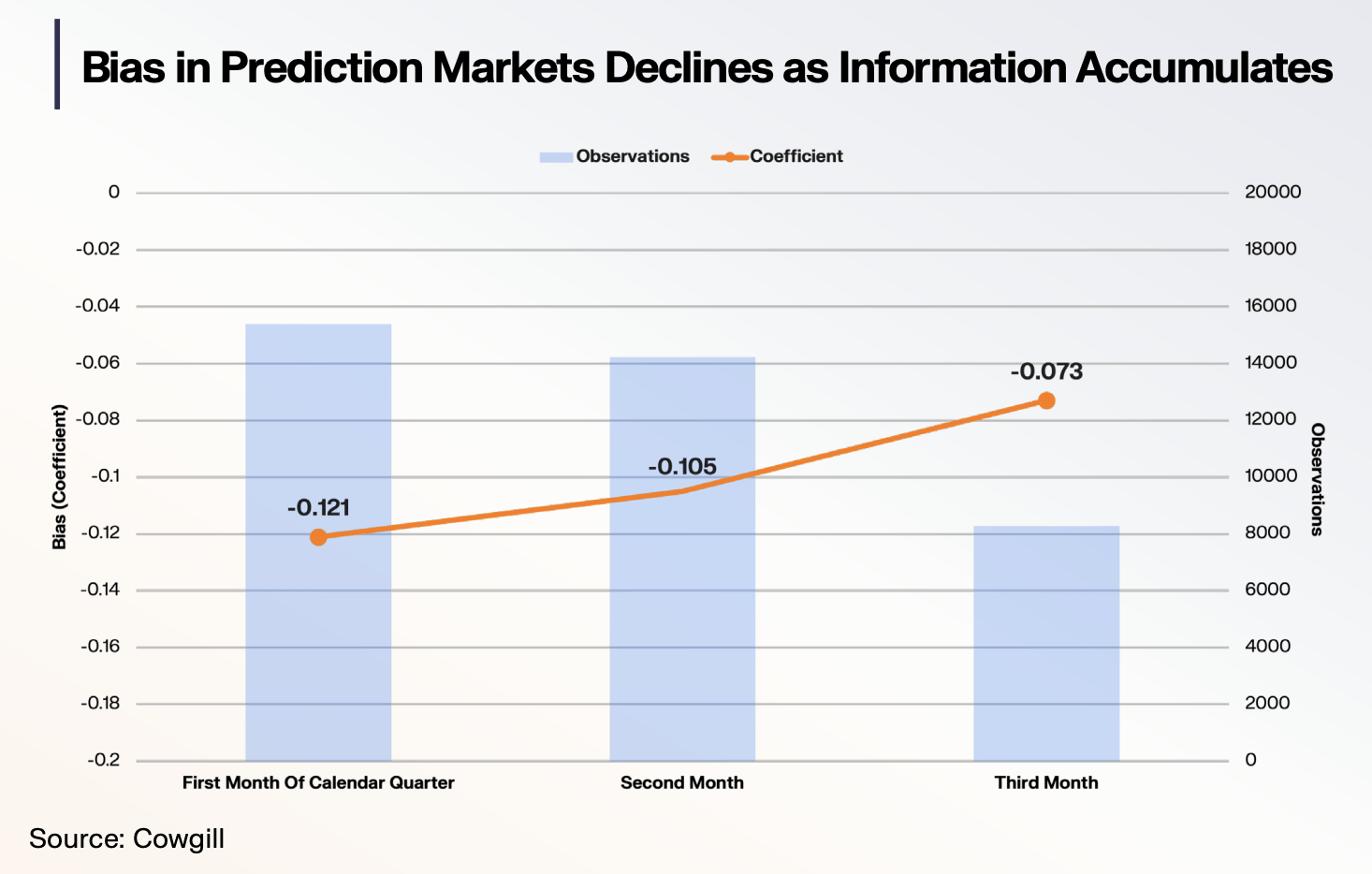

Bias Reduction Over Time

One of Google’s most important findings: prediction markets self-correct for optimism bias. Early in a market’s life, traders systematically overestimate positive outcomes. Initial trades skew toward outcomes participants hoped for rather than genuinely expected.

By month three, optimism bias measurably declined. Google’s internal bias tracking showed high bias in early weeks, steadily declining as information accumulated and participants observed the gap between estimates and reality. The longer a market runs, the more accurately it reflects genuine beliefs rather than institutional optimism.

This self-correcting property is one of the strongest arguments for sustained programmes. Do not judge a corporate prediction market by its first month.

HP: 75% Outperformance in Controlled Trials

HP conducted some of the most methodologically rigorous corporate prediction market trials in the literature. The design was direct: compare prediction market forecasts against official company forecasts for product demand and sales volumes. Same metrics. Same time horizons. Head-to-head.

The results were unambiguous. Crowd forecasts outperformed official company forecasts in 75% of trials. A 20-25% reduction in forecasting error.

For a company the size of HP, where production planning errors translate directly into excess inventory costs or lost sales from stockouts, a 20-25% improvement in forecast accuracy represents potentially hundreds of millions of dollars in value. That is not an abstraction. It is balance-sheet impact.

What made it work: information aggregation from dispersed sources. Individual product managers, sales representatives, supply chain analysts, and engineers each hold pieces of the forecasting puzzle. Traditional planning filters this through hierarchical reporting chains — each layer introducing compression, interpretation, and political distortion. The prediction market bypassed hierarchy entirely.

Microsoft: The Market Knew Before Management Did

Microsoft’s experience produced one of the most dramatic demonstrations of market-based forecasting in corporate history.

The company created internal prediction markets to track software project progress — whether projects would ship on time, hit quality benchmarks, or meet feature targets. In one well-documented case, a contract asking whether a specific project would deliver on schedule initially traded at moderate levels. Reflecting some optimism about the official timeline.

Then it collapsed to near zero within minutes.

Engineers, testers, project managers — people with firsthand knowledge of the project’s actual status — sold aggressively. Through their trades, they revealed what formal status reports had not yet acknowledged. The project ultimately shipped months late. Exactly as the market predicted.

The official reporting chain continued presenting optimistic timelines for weeks after the market had already priced in the delay. This is the core value proposition: prediction markets surface bad news faster than hierarchical reporting, because traders face financial incentives to be honest rather than political incentives to be optimistic.

Ford, Samsung, Best Buy, GE, and Electronic Arts

Beyond the heavily documented Google, HP, and Microsoft cases, several other major corporations experimented:

- Ford used prediction markets for vehicle sales forecasting — making production planning more responsive to real-time signals than dealer surveys and historical extrapolation alone.

- Samsung explored markets for technology roadmap planning, aggregating dispersed engineering knowledge about timelines and competitive dynamics.

- Best Buy tested retail demand forecasting, leveraging store-level employee knowledge that outperformed centralised analytics models.

- GE experimented with project portfolio management and strategic decision-making across diverse business units.

- Electronic Arts used markets for game sales forecasting and release date optimisation — domains where employee intuition about product quality often predicts commercial outcomes more accurately than quantitative models.

The common thread: prediction markets consistently revealed information that existing processes missed, suppressed, or distorted. The challenge was never accuracy. The markets worked. The challenge was integration — connecting signals to actual decision-making workflows.

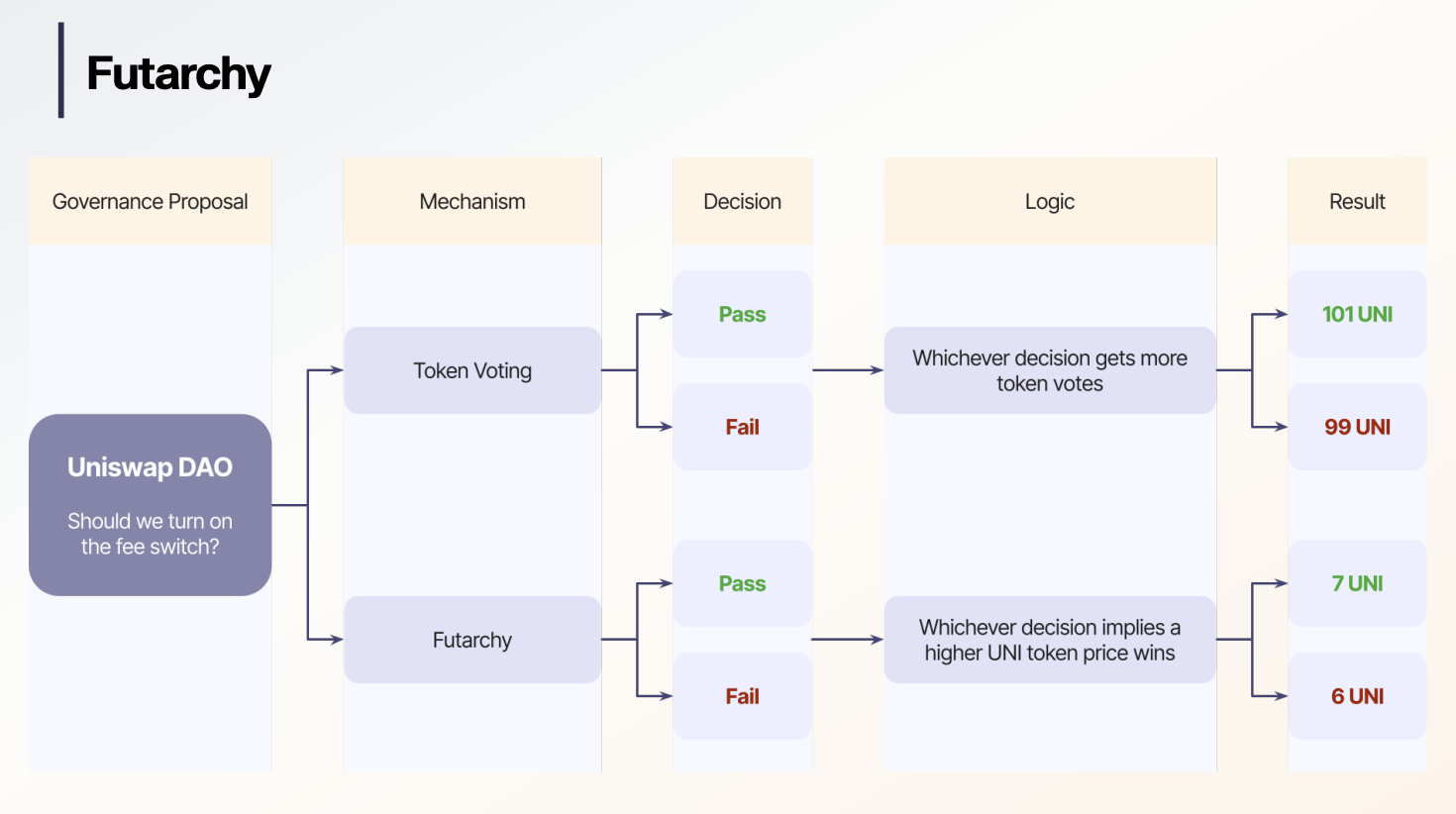

Futarchy: Vote on Values, Bet on Beliefs

Economist Robin Hanson’s concept of futarchy extends corporate prediction markets into governance and policy. The principle: organisations “vote on values but bet on beliefs.”

Decision-makers define the outcomes they want to optimise for — revenue growth, employee satisfaction, market share, carbon reduction. Prediction markets price the expected result of each proposed action. The policy whose market indicates the best expected outcome gets adopted.

This separates two fundamentally different activities. Choosing goals: a value judgement requiring human deliberation. Forecasting consequences: an empirical question where markets consistently outperform committees.

A real-world illustration: Microsoft’s stock rose 8% on the day Steve Ballmer announced his resignation as CEO. The market priced the expected impact of a leadership change — not a value judgement about Ballmer as a person, but a forecast of financial consequences under new leadership. In a futarchy-inspired system, this type of signal would be formally integrated into governance decisions rather than observed after the fact.

As Stefan George noted, prediction markets are increasingly influencing politics and governance beyond the corporate context. The same mechanisms that allow Google employees to forecast product timelines can allow citizens to forecast the consequences of policy proposals.

Why Corporate Prediction Markets Work

The academic evidence is extensive, drawing on research by Bo Cowgill (Google), Kay-Yut Chen (HP), and others. Five structural properties explain the outperformance:

- Information aggregation: Markets combine dispersed knowledge from hundreds or thousands of participants. No single forecaster can match this breadth.

- Incentive alignment: Even with virtual currency, participants face reputational and competitive incentives to be accurate rather than optimistic. This counters the well-documented bias in corporate planning toward overconfidence.

- Real-time updating: Unlike quarterly forecast cycles, prediction markets update continuously. Microsoft’s project delay was visible in prices weeks before formal reports acknowledged it.

- Bias reduction over time: As Google demonstrated, early trades carry optimism bias, but it declines measurably by month three. Sustained markets produce increasingly calibrated forecasts.

- Anonymity and psychological safety: Anonymous trades allow employees to express views they would never voice in a meeting. The engineer who knows a project will miss its deadline can sell the “on-time” contract without fear of political repercussions.

Barriers to Adoption — And What Breaks Them

Despite compelling results, corporate prediction markets have not yet achieved mainstream adoption. Three barriers explain the gap:

First, organisational culture resists mechanisms that bypass hierarchical authority. When a prediction market contradicts a senior executive’s forecast, the institutional response is frequently to question the market rather than the executive. Second, regulatory concerns in some jurisdictions create uncertainty about whether internal markets — even virtual-currency ones — constitute gambling. Third, many early programmes were treated as experiments rather than operational tools, limiting their influence on actual decisions.

What is changing: blockchain-based prediction market infrastructure has matured. Public acceptance of prediction markets has grown. A new generation of managers grew up trading on Polymarket and Kalshi. Cultural resistance is eroding.

The question is no longer whether corporate prediction markets work. HP’s 75% outperformance rate and Google’s bias reduction data answer that definitively. The question is how fast organisations integrate them at the speed and scale the technology now enables.

Frequently Asked Questions

Which companies use internal prediction markets?

Google, Microsoft, Hewlett-Packard, Ford, Samsung, Best Buy, GE, and Electronic Arts have all experimented with internal prediction markets. Google operates the longest-running programmes: Prophit (launched 2005) and Gleangen (2020), with approximately 20% of employees participating across topics ranging from Gmail user counts to office reopening schedules.

How accurate are corporate prediction markets?

In HP’s controlled trials, prediction market crowd forecasts outperformed official company forecasts in 75% of cases, with a 20-25% reduction in forecasting error. At Microsoft, an internal market predicted a major software project delay weeks before formal status reports acknowledged the problem. Google’s research documented measurable declines in optimism bias by the third month of market operation.

What is futarchy?

Futarchy is a governance concept where organisations “vote on values but bet on beliefs.” Decision-makers define desired outcomes, and prediction markets price the expected result of each proposed policy or action. The action whose market indicates the best outcome is adopted. This separates value judgements (human deliberation) from empirical forecasting (market aggregation), leveraging each where it performs best.

Can prediction markets replace traditional business forecasting?

Prediction markets are unlikely to fully replace traditional forecasting, but the evidence strongly supports using them as a complement. They are particularly valuable for reducing optimism bias, surfacing dispersed employee knowledge, and detecting problems that hierarchical reporting chains suppress. Google’s research emphasises that markets must be explicitly linked to decisions to deliver full value — standalone “curiosity” markets underperform their potential.