Store of Value to Digital Oil: How Ussage Differs Between BTC to ETH

ETH: Store of Value or Utility Asset? The Data Settles the Debate

One in four ETH is locked in staking or ETFs. Yet it turns over at twice bitcoin’s rate. That contradiction is not a flaw. It is the feature that defines ethereum’s entire investment thesis.

Fidelity says ETH “can serve as medium of exchange and store of value.” VanEck has gone further, floating ETH as a potentially better store of value than BTC for corporate treasuries. Bold claims. We went to the onchain data to see if they hold up.

The Lock-Up: 25% and Growing

Approximately one in four ETH tokens are currently locked in staking contracts and ETF custody. ETH ETFs hold 5.24% of supply. Staking absorbs a further significant share. These are not short-duration positions. Staking requires commitment. ETF wrappers impose custody constraints.

The anchored float for ETH sits at 25.1%. That dwarfs bitcoin’s 6.7%. By raw percentage, more of ethereum’s supply is structurally removed from liquid circulation than bitcoin’s.

On paper, this looks like a stronger store-of-value signal.

In practice, the story is more complex.

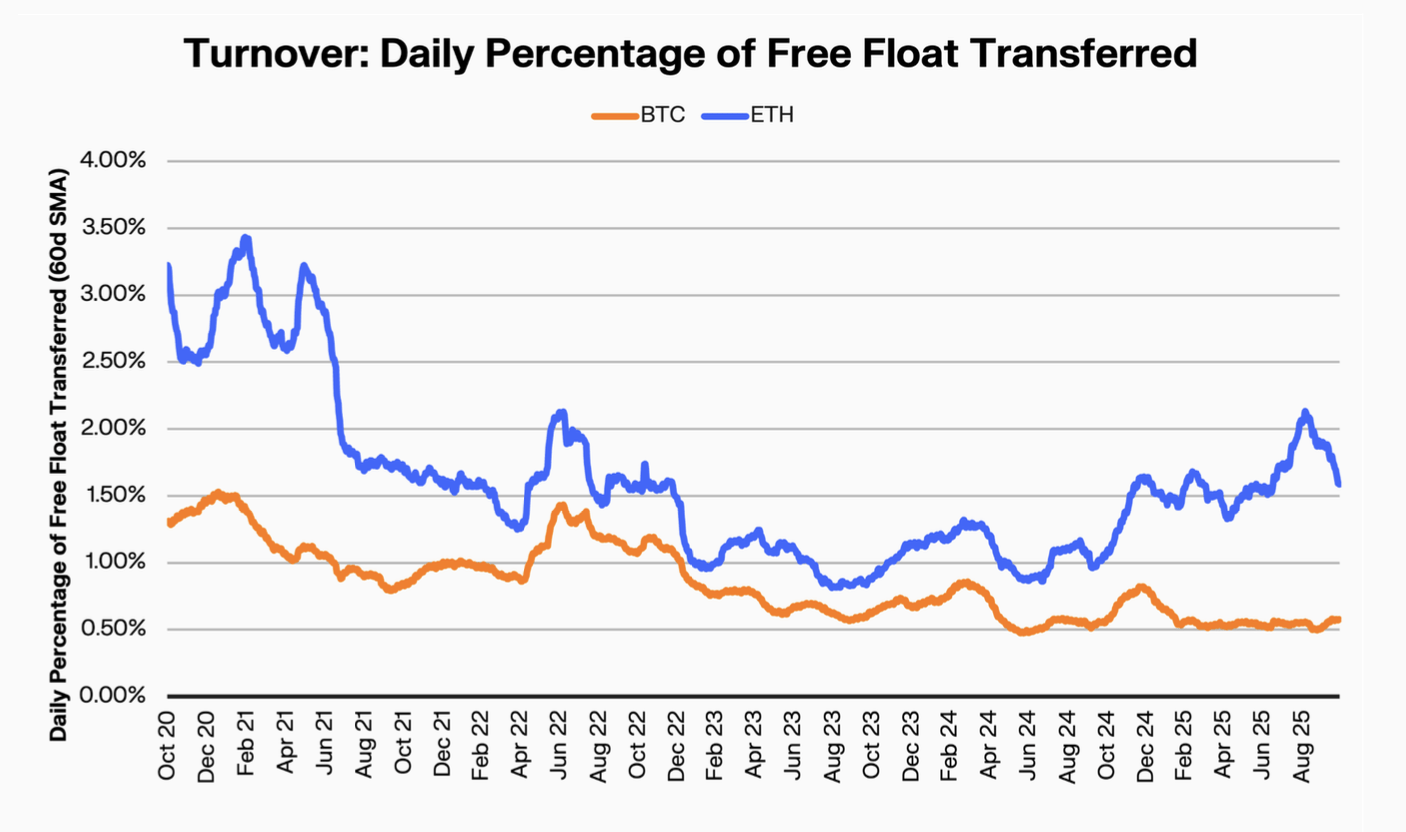

Turnover Tells a Different Story

ETH’s daily turnover runs at 1.34%. That is more than double bitcoin’s 0.61%. For context, gold turns over at 0.29% daily and the U.S. dollar at 20%. ETH sits closer to BTC than to fiat, but the gap between the two crypto assets is significant.

Higher turnover signals higher velocity. Coins move more frequently. They cycle through DeFi protocols, get restaked, serve as collateral, and flow through decentralised exchanges. This is not idle capital sitting in cold storage. This is capital at work.

Long-term ETH holders mobilise their holdings at three times bitcoin’s rate. The supply that is locked is locked. But the supply that is free moves fast and frequently.

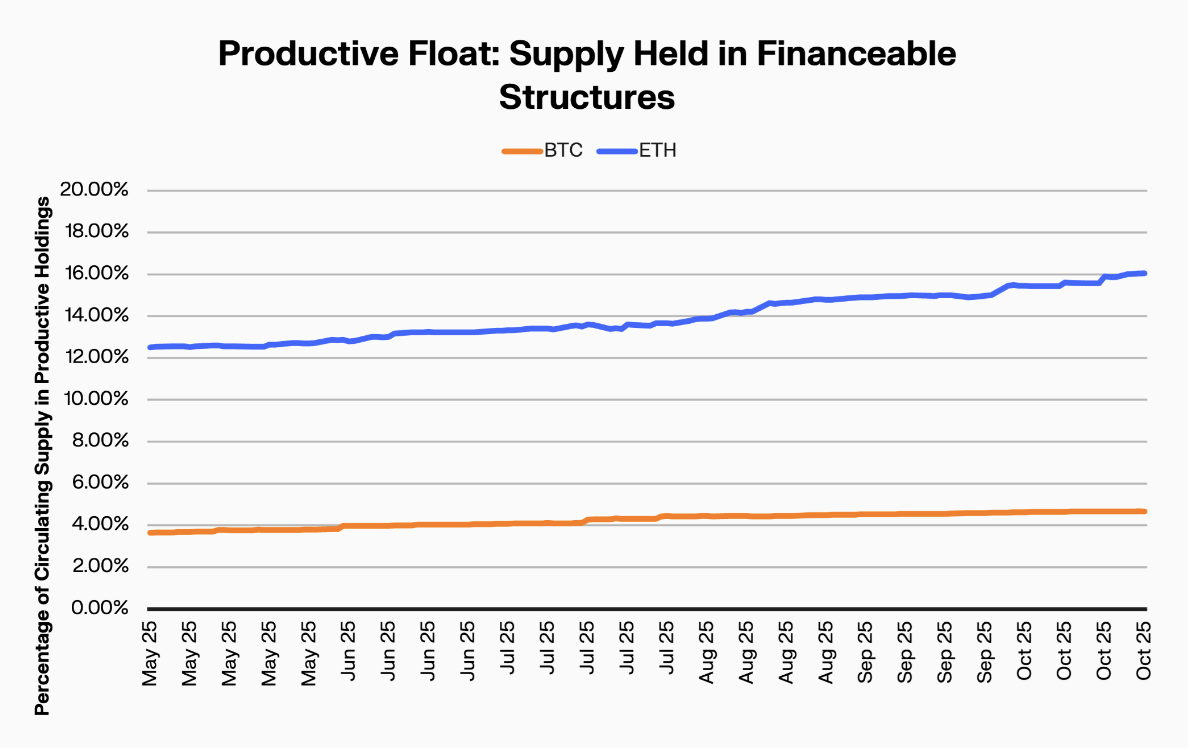

The Productive Float: Where ETH Diverges

ETH’s productive float stands at 16.05%. Bitcoin’s is 4.66%. That gap reveals the fundamental difference between these two assets.

Productive float measures supply actively deployed in DeFi, liquid staking, lending protocols, and collateralised structures. For ETH, 16% of total supply is generating yield, providing liquidity, or backing onchain financial products. For BTC, that figure barely crosses 4.5%.

A full 16% of ETH supply is embedded in DeFi, liquid staking, and collateralised structures. This creates a gravitational pull that keeps ETH circulating within the onchain economy rather than sitting dormant in wallets.

Bitcoin holders preserve. ETH holders deploy.

The VanEck Thesis: ETH as Treasury Asset

VanEck’s argument that ETH could serve as a better store of value than BTC for corporate treasuries rests on one key insight: yield. A treasury that holds ETH can stake it, earning protocol rewards while maintaining exposure to the asset’s price appreciation.

BTC treasuries, by contrast, hold a non-productive asset. Strategy securitises bitcoin for traditional financial markets, but the underlying BTC generates no native yield. It appreciates or it does not.

ETH offers a middle path. Store value and put it to work simultaneously.

The counter-argument is equally sharp. A store of value should be simple. Complexity introduces risk vectors. Bitcoin’s dormancy profile reflects an asset that demands nothing from its holder. ETH’s productive nature requires active management, smart contract exposure, and protocol risk tolerance.

Fidelity’s Framing

Fidelity’s assessment that ETH “can serve as medium of exchange and store of value” is carefully worded. The emphasis falls on “can.” ETH has the capacity for both roles. Whether it excels at either depends on the holder’s intent and time horizon.

For a DeFi-native treasury, ETH’s dual functionality is a feature. For a conservative institutional allocator seeking pure monetary assurance, the complexity is a cost.

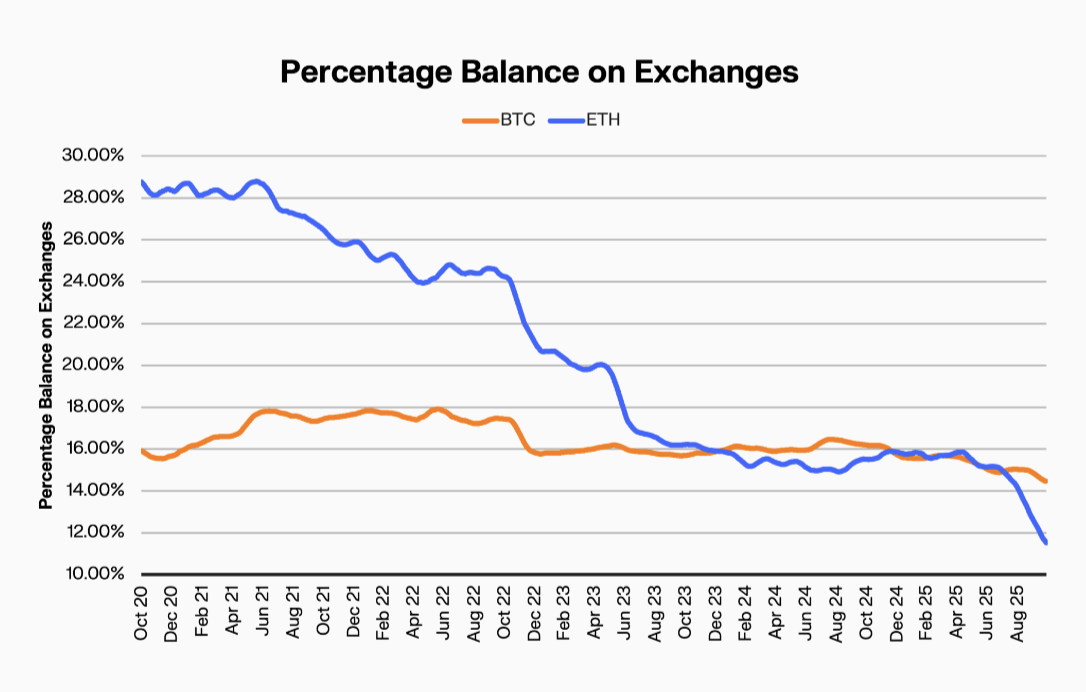

Exchange Posture: The Steepest Decline in Crypto

ETH’s exchange balance has declined by 18%. The exchange share has dropped from 29% to 11.3%. That is the steepest exchange balance decline among major crypto assets.

Where is the ETH going? Three destinations dominate.

Staking contracts. DeFi protocols. Institutional custody. Each absorbs ETH from exchange float and redirects it into productive or locked structures. The exchange exodus is not speculative panic. It is structural reallocation.

Compare that to BTC’s exchange decline of just 1.5%. Bitcoin leaves exchanges slowly, methodically, into cold storage. ETH leaves rapidly, into an expanding ecosystem of onchain applications that demand collateral.

The Dual Identity Problem

Every asset class benefits from a clear narrative. Gold is a store of value. The dollar is a medium of exchange. Bitcoin, increasingly, is digital gold.

ETH resists a single label. It is programmable money. It is yield-bearing collateral. It is the settlement layer for decentralised finance. It is a store of value for those who stake and hold. It is a utility token for those who build and transact.

This duality is both ETH’s greatest strength and its biggest communication challenge. Institutional allocators want clean categories. ETH refuses to fit neatly into any one of them.

The data suggests a resolution. ETH is not choosing between store of value and utility. It is building a new category: the productive monetary asset. One that stores value through programmatic yield rather than through inactivity.

What the Numbers Demand You Consider

25.1% anchored float. 16.05% productive float. Daily turnover at 1.34%. Long-term holders mobilising at three times bitcoin’s rate. Exchange share plummeting from 29% to 11.3%.

ETH is not bitcoin. It never will be. But the assumption that bitcoin owns the store-of-value narrative by default deserves scrutiny. ETH’s onchain behaviour reveals an asset that stores value differently. Not through dormancy. Through deployment.

Whether that model proves more durable is the defining question of the next market cycle.

FAQ

Is ETH a store of value or a utility token?

ETH functions as both. One in four tokens are locked in staking or ETFs (store-of-value behaviour), while 16% of supply is actively deployed in DeFi and collateralised structures (utility behaviour). Fidelity describes ETH as capable of serving as “medium of exchange and store of value.” The data supports a dual identity rather than a single classification.

Why does ETH have higher turnover than bitcoin?

ETH’s daily turnover of 1.34% (versus BTC’s 0.61%) reflects its role as collateral and fuel within the DeFi ecosystem. Supply cycles through staking, lending, liquidity provision, and decentralised exchanges. Long-term ETH holders mobilise their holdings at three times bitcoin’s rate, driven by productive onchain opportunities.

Could ETH replace bitcoin as a treasury asset?

VanEck has floated this idea, arguing that ETH’s staking yield gives it an advantage over non-productive BTC for corporate treasuries. ETH’s anchored float of 25.1% exceeds bitcoin’s 6.7%, and the productive float of 16.05% generates returns. The trade-off is added complexity: smart contract risk, protocol governance, and active management requirements that bitcoin avoids.

What percentage of ETH is staked or locked?

Approximately one in four ETH tokens are locked in staking contracts or ETF custody. ETH ETFs hold 5.24% of supply. The total anchored float, including staking, ETFs, and institutional custody, reaches 25.1% of circulating supply. An additional 16% sits in DeFi protocols and collateralised structures.