Store of Value to Digital Oil: How Ussage Differs Between BTC to ETH

Bitcoin Store of Value: Onchain Data Proves the Digital Gold Thesis (2026)

More than 61% of all bitcoin has not moved in over a year. That single data point tells you more about BTC’s identity than a thousand white papers ever could.

The store-of-value narrative is not a marketing slogan. It is a behavioural pattern etched into the blockchain itself. When we analyse how holders interact with their BTC, the picture that emerges is one of deep conviction, structural dormancy, and a monetary asset that increasingly resembles gold.

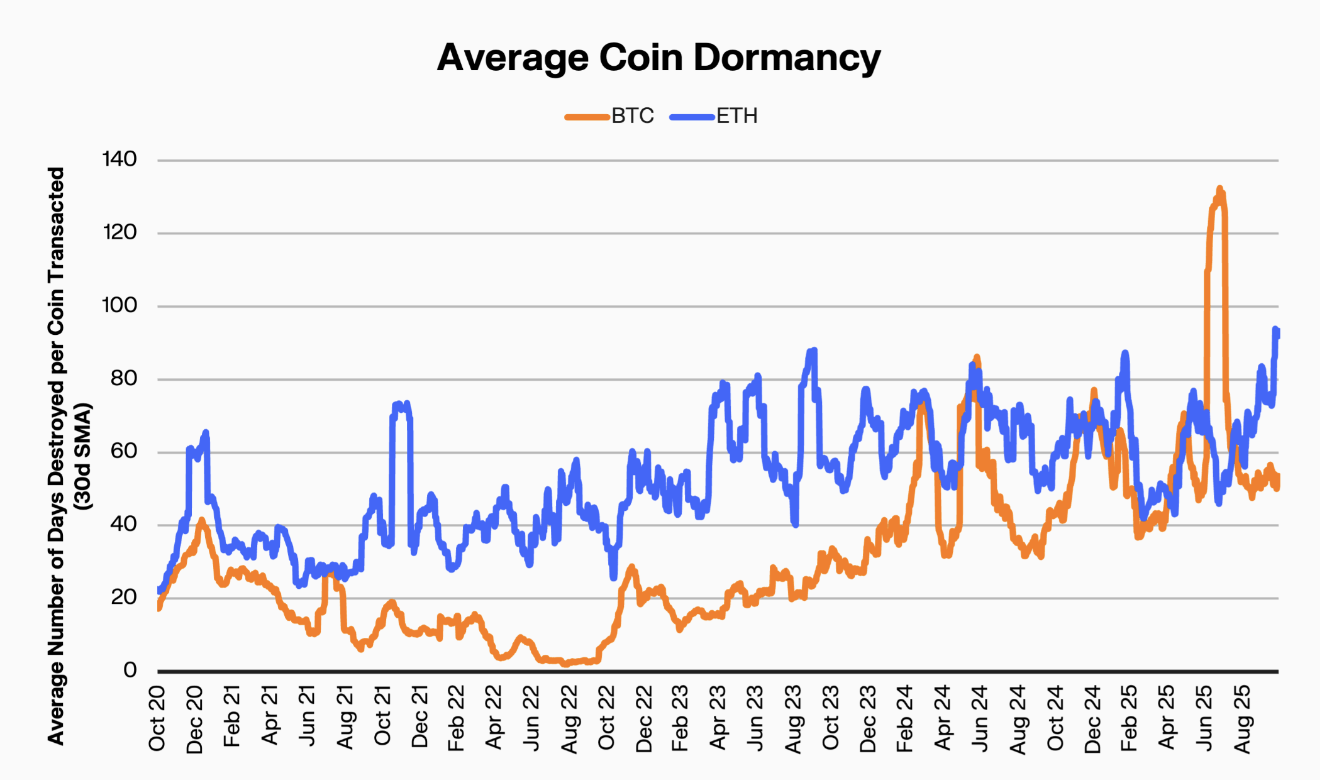

Dormancy: The Defining Metric

Bitcoin’s daily turnover sits at just 0.61%. Compare that to gold at 0.29% and the U.S. dollar at 20%. BTC slots neatly between the world’s oldest store of value and its most liquid medium of exchange.

That positioning is not accidental.

Holders overwhelmingly choose to sit. They accumulate and wait. The supply that does move tends to circulate among short-term traders and arbitrageurs, while the vast majority remains locked in cold storage, multisig wallets, and long-term custody solutions. This creates a supply dynamic where the marginal seller becomes rarer over time.

Gold’s daily turnover of 0.29% reflects centuries of established store-of-value behaviour. Bitcoin, at 0.61%, is converging on that pattern within a single generation. The gap is closing. Fast.

How ETFs and Institutional Custody Reinforce Dormancy

BTC ETFs now hold 6.7% of the total bitcoin supply. These are not trading vehicles in the traditional sense. They are custody sinks that pull coins off exchanges and into regulated, long-duration wrappers.

Strategy, the company formerly known as MicroStrategy, securitises bitcoin for traditional financial markets. Their model converts corporate balance sheet demand into permanent BTC removal from liquid circulation. Every share issued against bitcoin holdings creates another layer of structural illiquidity.

JPMorgan’s research team now groups bitcoin alongside gold in what they call the “debasement trade.” When the world’s largest bank classifies BTC as a hedge against monetary expansion, the store-of-value thesis shifts from speculative to institutional consensus.

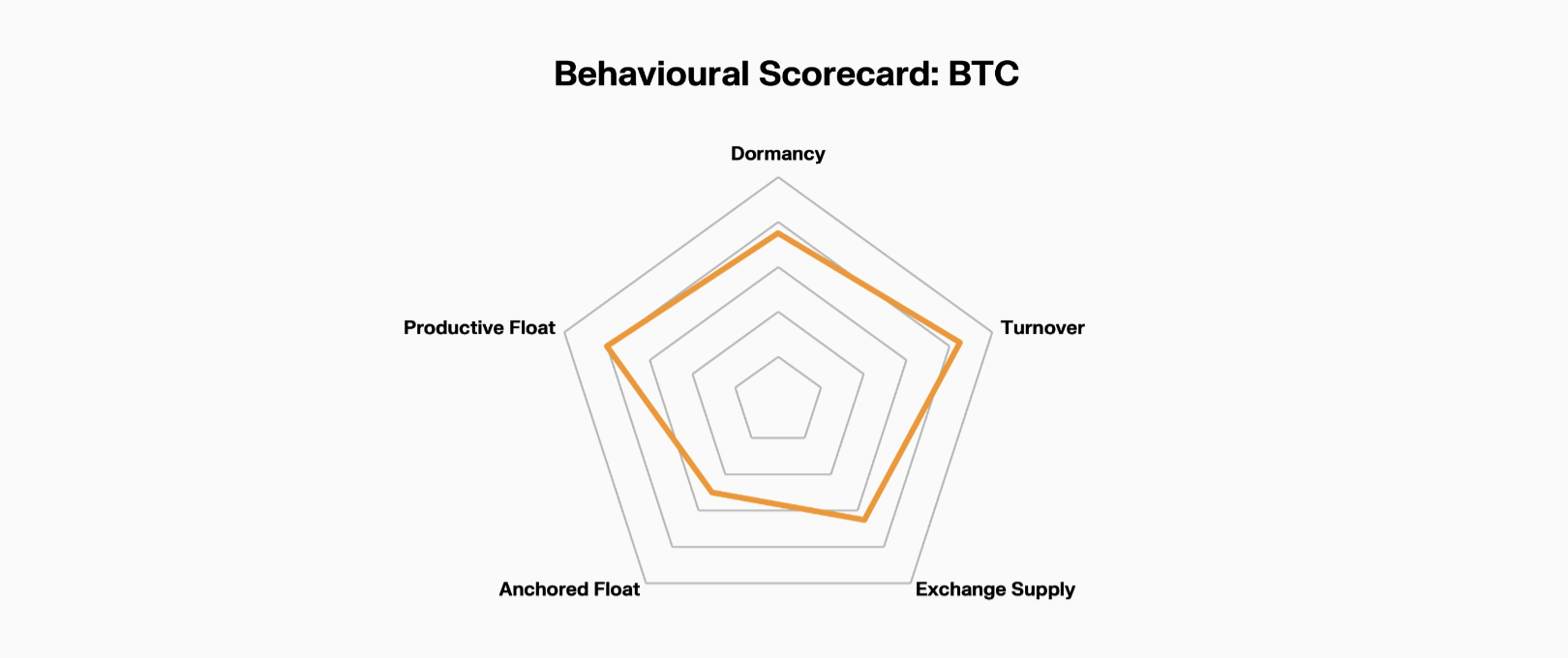

The Anchored Float

We define anchored float as supply held in ETFs, institutional custody, and similar long-duration structures. For BTC, that figure stands at 6.7%. It sounds modest until you consider the trajectory. Two years ago, the number was effectively zero for regulated ETF products.

Digitally Accessible Tokens (DATs) account for another 3.6% of supply. These sit in addresses linked to institutional-grade custody but outside ETF wrappers. Combined, over 10% of bitcoin supply is now locked in structures designed for holding, not trading.

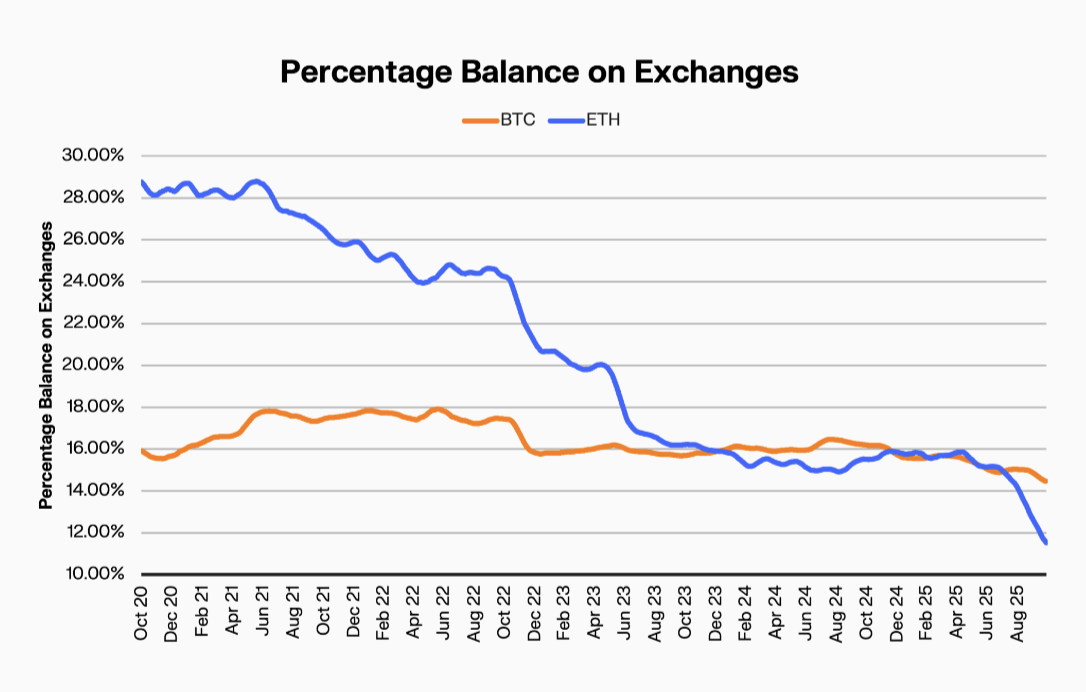

The Exchange Exodus

Exchange-held BTC has declined by 1.5%, with exchange share now sitting at 14.3%. The direction is clear, even if the magnitude appears modest relative to ETH’s far steeper exchange decline.

For bitcoin, this gradual drift matters more than it looks. BTC’s exchange balance has been falling steadily since 2020. Each percentage point removed from exchanges represents billions of dollars in supply that becomes structurally unavailable to the spot market.

Less supply on exchanges. More supply dormant. The store-of-value thesis compounds.

Bitcoin vs Gold: The Behavioural Comparison

Gold’s credentials rest on millennia of human behaviour. People hold it. They pass it down. They store it in vaults and forget about it. Bitcoin is replicating that same behavioural DNA in compressed time.

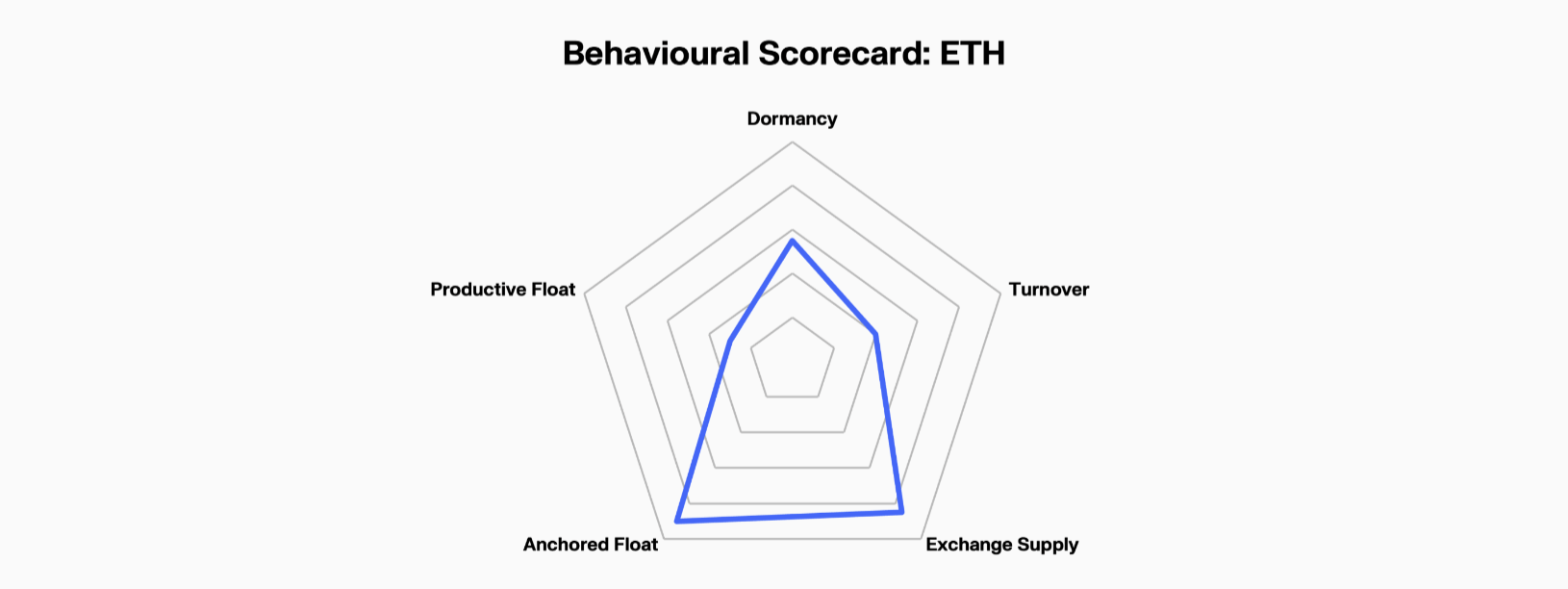

The productive float for BTC sits at 4.66%. This measures supply actively deployed in DeFi, lending, or yield-generating structures. Compare that to ETH’s productive float of 16.05%. Bitcoin holders are not looking for yield. They are looking for preservation.

That distinction is the entire argument in one number.

When Fidelity published their assessment that ETH “can serve as medium of exchange and store of value,” the implicit framing placed BTC squarely in the pure store-of-value category. No dual identity. No utility trade-off. Just monetary assurance.

What Long-Term Holder Behaviour Reveals

BTC long-term holders mobilise their supply at a fraction of the rate seen in other crypto assets. ETH long-term holders, by contrast, move their holdings at three times the rate of BTC holders. This is not a criticism of ETH. It reflects a fundamentally different asset identity.

Bitcoin holders behave like gold holders. They buy, they store, they wait. The blockchain records this patience in immutable detail. Every month of dormancy strengthens the case. Every cycle of accumulation without distribution adds another layer of evidence.

VanEck has floated the idea that ETH could serve as a better store of value than BTC for corporate treasuries. The onchain data disagrees. Treasury assets demand predictable dormancy, low turnover, and minimal productive complexity. BTC delivers all three.

The Structural Case

Pull the threads together and the picture is stark. 61% of supply dormant for over a year. Daily turnover at 0.61%, converging toward gold. ETF holdings at 6.7% and growing. Exchange balances falling. Long-term holders sitting with conviction.

Bitcoin does not need to become a medium of exchange to succeed. It does not need smart contracts, DeFi composability, or staking yield. Its value proposition is simpler and, arguably, more powerful.

Hold it. Wait. Let monetary debasement do the rest.

Frequently Asked Questions

Why is bitcoin considered a store of value?

Bitcoin’s fixed supply of 21 million coins, combined with the fact that 61% of supply has not moved in over a year, creates a scarcity profile similar to gold. Its daily turnover of 0.61% sits between gold (0.29%) and fiat currencies (USD at 20%), positioning it as a digital monetary asset optimised for preservation rather than spending.

How does bitcoin compare to gold as a store of value?

Gold’s daily turnover is 0.29%; bitcoin’s is 0.61%. Both assets share a behavioural pattern of deep dormancy among holders. BTC ETFs now hold 6.7% of supply, and JPMorgan groups bitcoin alongside gold in their “debasement trade” thesis. The convergence is measurable and accelerating.

What percentage of bitcoin is held long term?

Over 61% of BTC supply has not moved in more than a year. BTC ETFs hold 6.7% of supply, DATs account for 3.6%, and exchange balances continue to decline. The anchored float, which measures supply in long-duration institutional structures, sits at 6.7% and is growing.

Do bitcoin ETFs affect its store-of-value status?

Yes. BTC ETFs hold 6.7% of total supply in regulated custody structures designed for long-term holding, not active trading. This removes coins from liquid circulation and reinforces bitcoin’s dormancy profile. Companies like Strategy further securitise bitcoin for traditional markets, deepening the structural illiquidity.