Keyrock x Bitso Business

How Local Stablecoins Trade: From Exchange to Onchain

Written by Amir Hajian

Read the full report

Preface

Stablecoins have meant dollar stablecoins, and still mostly do. But the local ones have grown up.

This report examines local stablecoins by tracking their flows and trading across the four stages of their lifecycle, from centralised exchanges through to onchain pools. Co-published with Bitso, this report was first presented at Bitso’s 2026 stablecoin conference in Mexico, with insights from contributors across the stablecoin, traditional finance, and onchain landscape, including Dune, Ripple, Qivalis, Bridge, and Mirae Asset.

Introduction

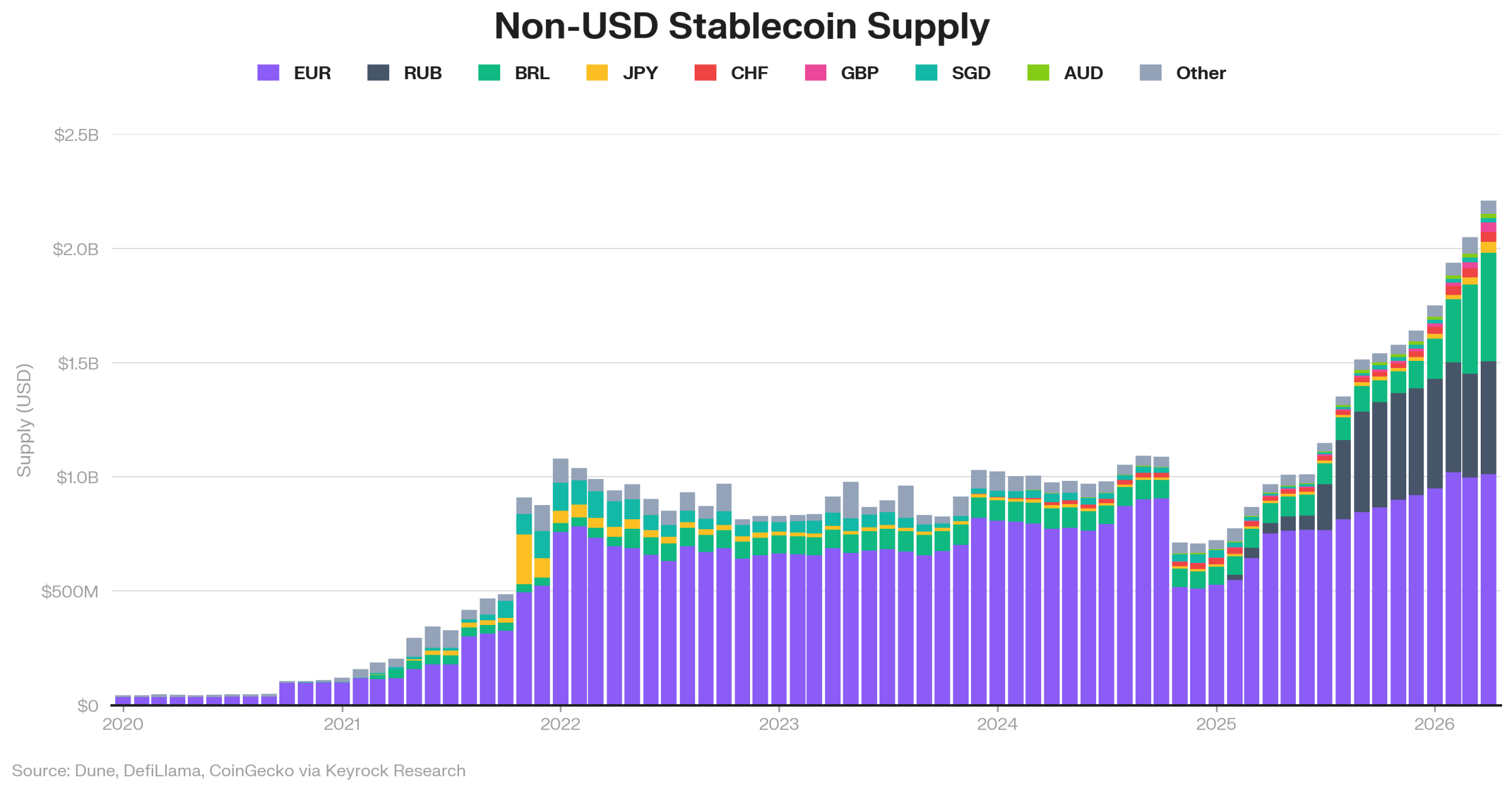

Through 2023 the euro, Brazilian real, Japanese yen, and a long tail of other currencies barely registered onchain. 2026 shows a different market. Non-USD supply has grown from $44 million to $2.2 billion, centralised exchanges cleared roughly $525 billion of fiat-to-stablecoin spot in 2025 across 19 local currencies, up from 10 two years ago, and native onchain DEX trading crossed $1 billion again in March 2026.

Onchain activity alone does not show the full picture. Centralised exchanges are the primary FX venues for stablecoins today, and the story of local stablecoins only emerges by tracking their flows across each stage of their lifecycle. We mapped that journey across 30 centralised exchanges, 45 chains, and 87 non-USD stablecoins traded through more than 900 liquidity pools, drawing on Amberdata, Dune Analytics, DefiLlama, CoinGecko, and Keyrock’s internal data.

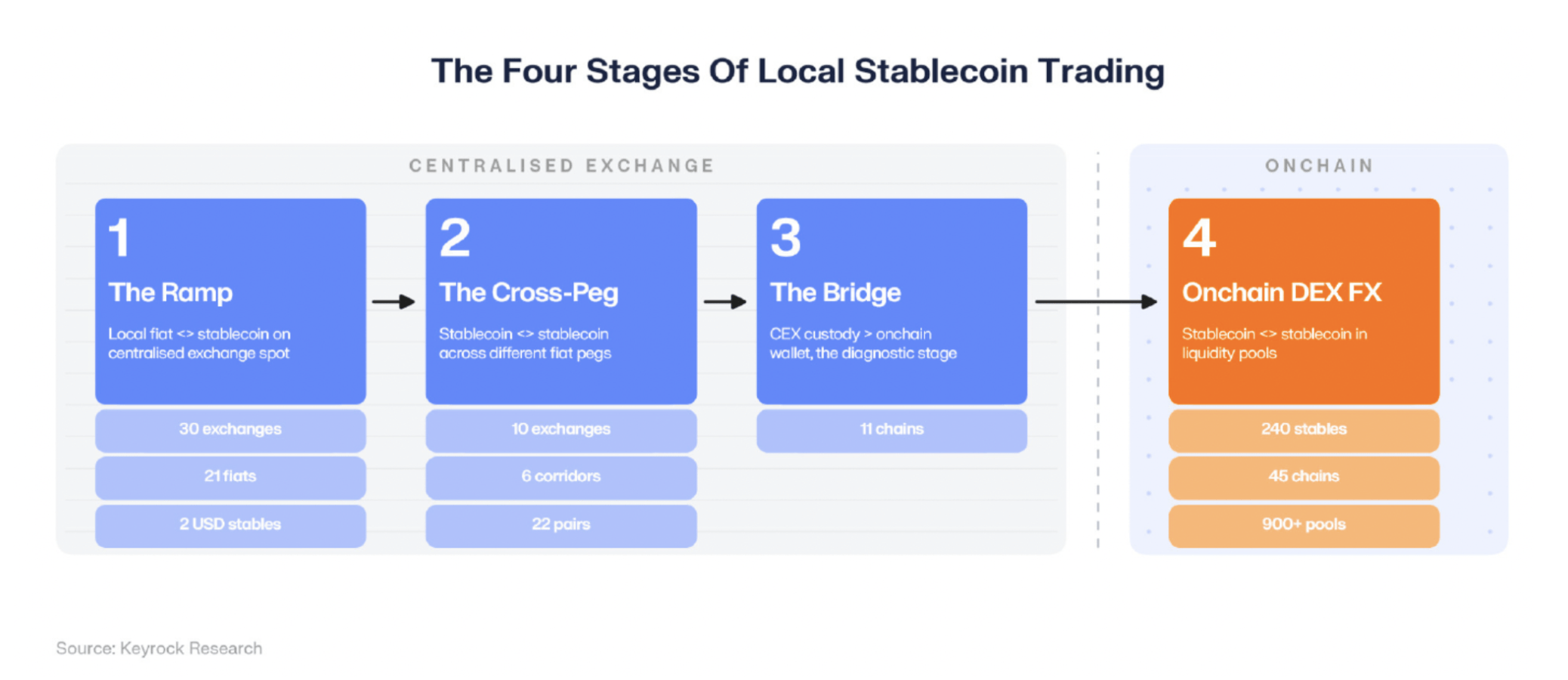

The Four Stages of Local Stablecoin Trading

A local stablecoin moves through four stages, in the order capital flows through it.

It begins on the centralised exchange ramp, it can then trade against other stablecoins on the same book, then leaves the exchange into a user’s own wallet, then trades onchain in liquidity pools. The market thins at every step. The ramp is broad and active for every currency in this report, each stage below it is smaller than the last, and only the euro is active the whole way down.

The Ramp

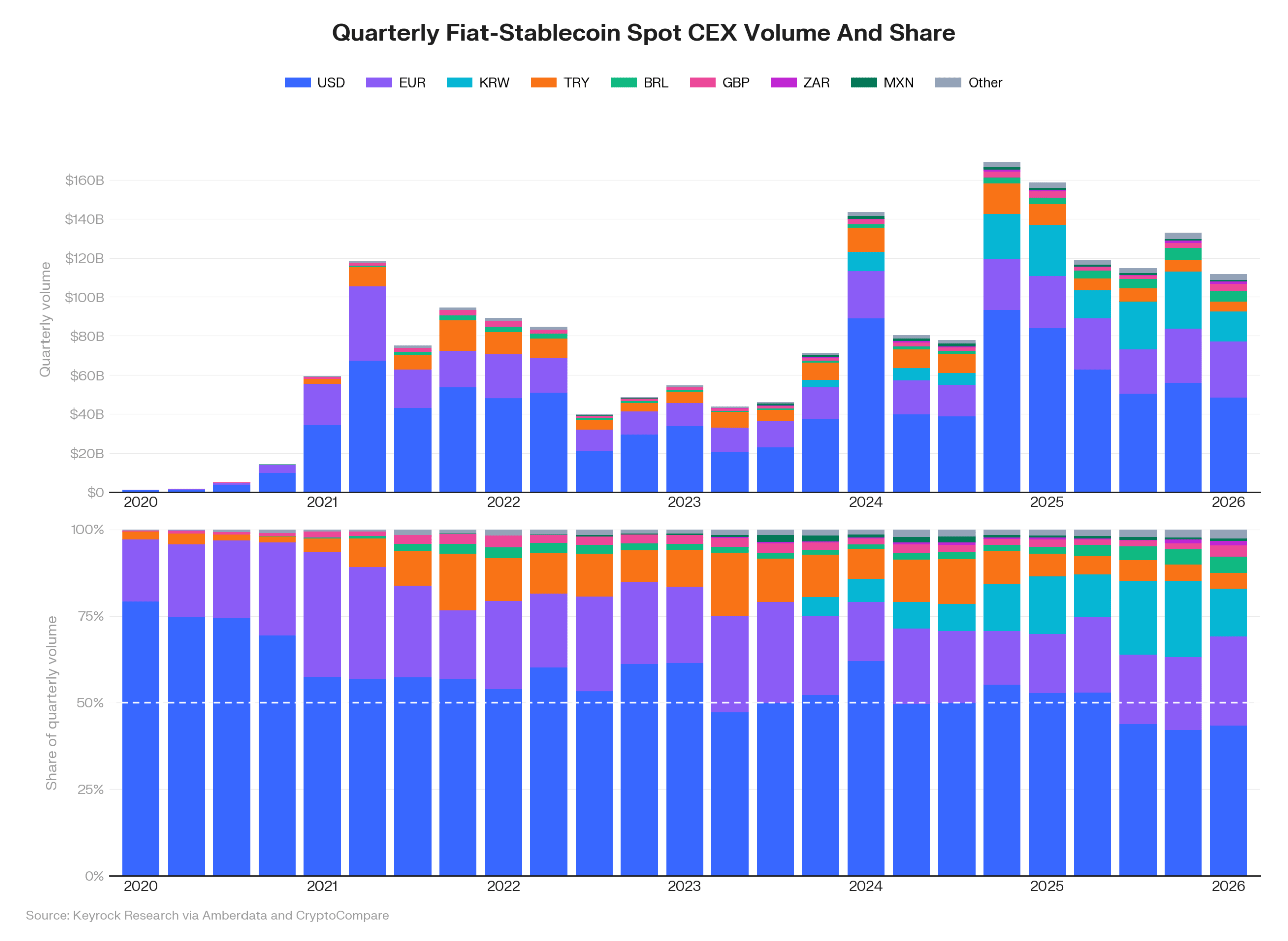

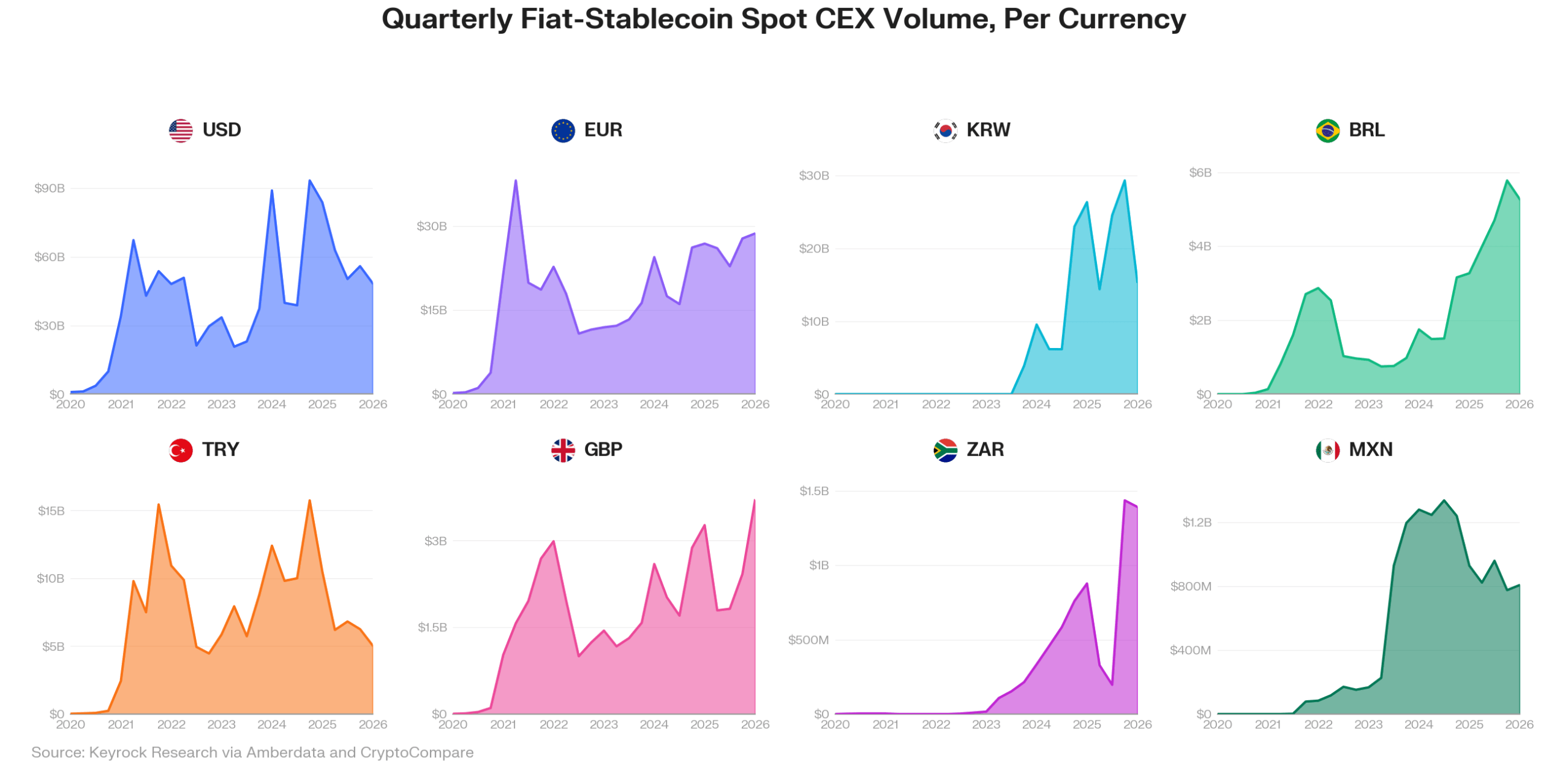

The ramp is where stablecoin FX actually happens today, and the stage most analyses of stablecoin growth miss. Centralised exchange order books moved $525 billion of fiat-to-stablecoin spot in 2025. Between 2022 and 2025 that volume roughly doubled, and the number of currencies with meaningful monthly volume rose from 10 to 19.

The Korean won went from a standing start in late 2023 to $29 billion in a single quarter, the largest single-currency arrival in the dataset, while the Brazilian real has compounded at about 20% per quarter for two years. In 2025 the dollar’s share of total spot volume fell below 50% and stayed there for three consecutive quarters, the first sustained run below that line. The dollar is losing share without losing scale.

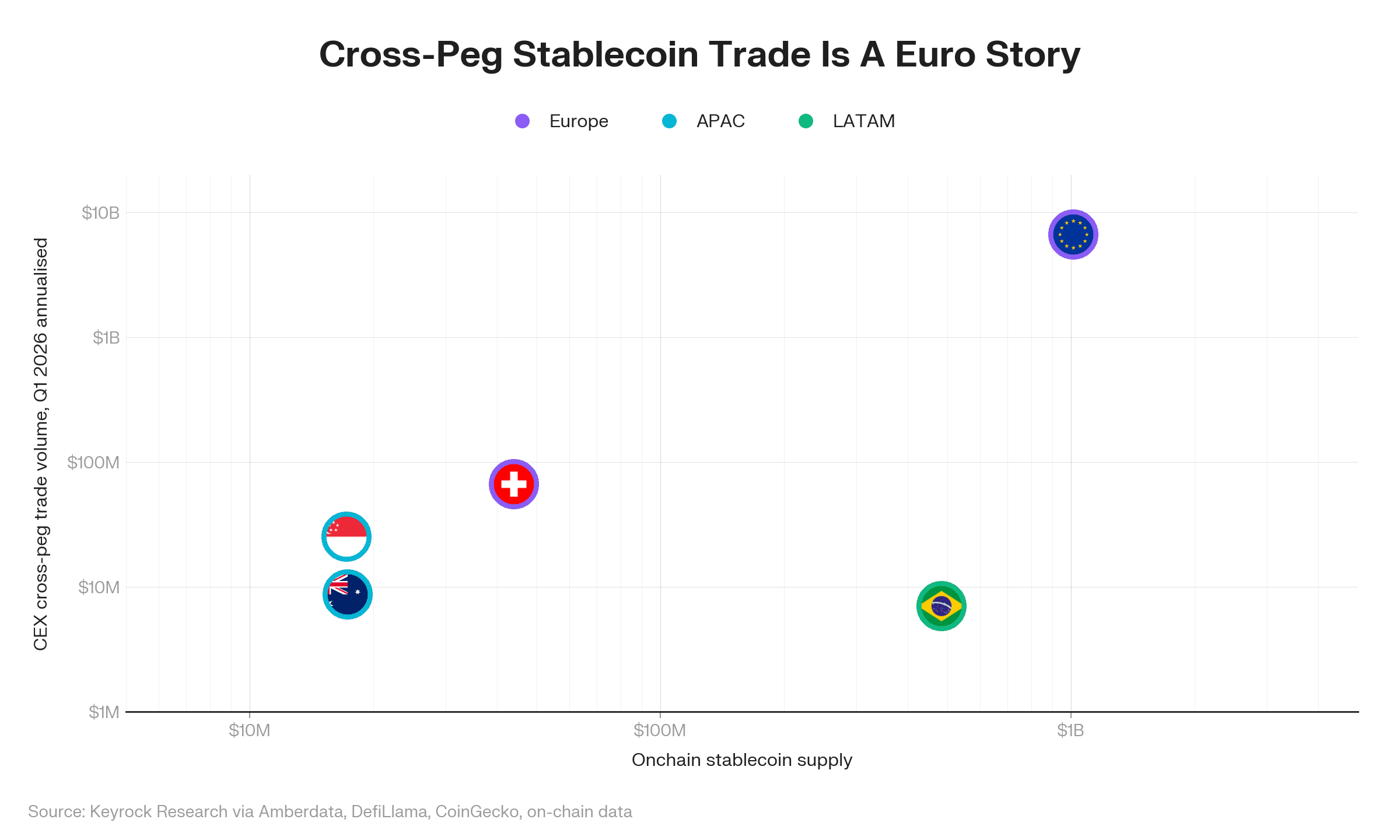

The Cross-Peg

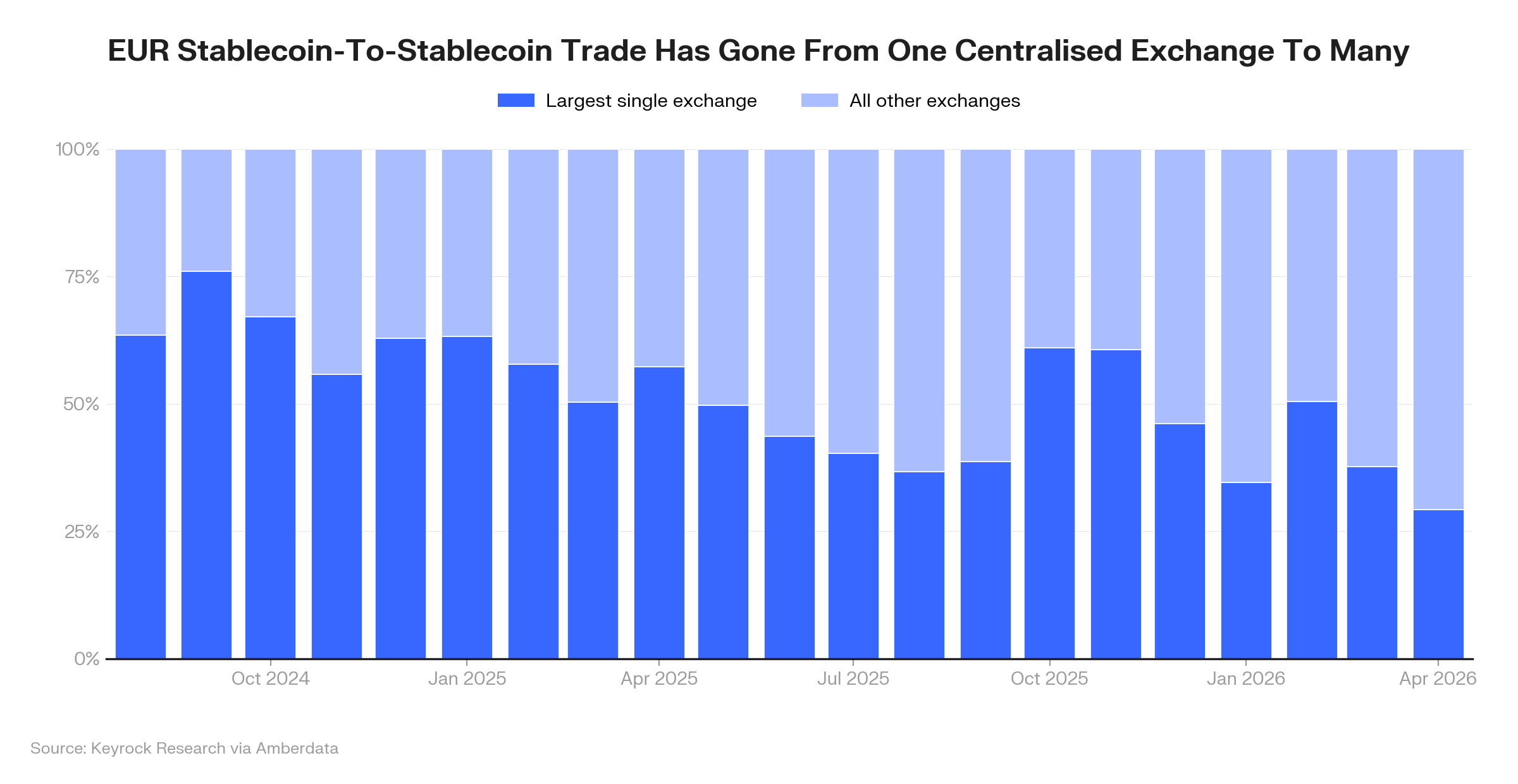

Once a local stablecoin trades against fiat, the next question is whether anyone wants to hold it rather than just pass through it. The cross-peg measures spot trade between two stablecoins on the same book, and it is the narrowest stage in the funnel. It runs at $6.7 billion annualised, about 1.5% of the ramp’s volume, and the euro alone accounts for 95% of it since 2022.

For the euro that means its stablecoins have graduated from exit ramp to held position, with the book turning over the entire onchain euro supply more than six times a year. The euro has also spread from a single exchange in 2024 to nine by the first quarter of 2026. Outside it, the corridor map is mostly dormant or just starting.

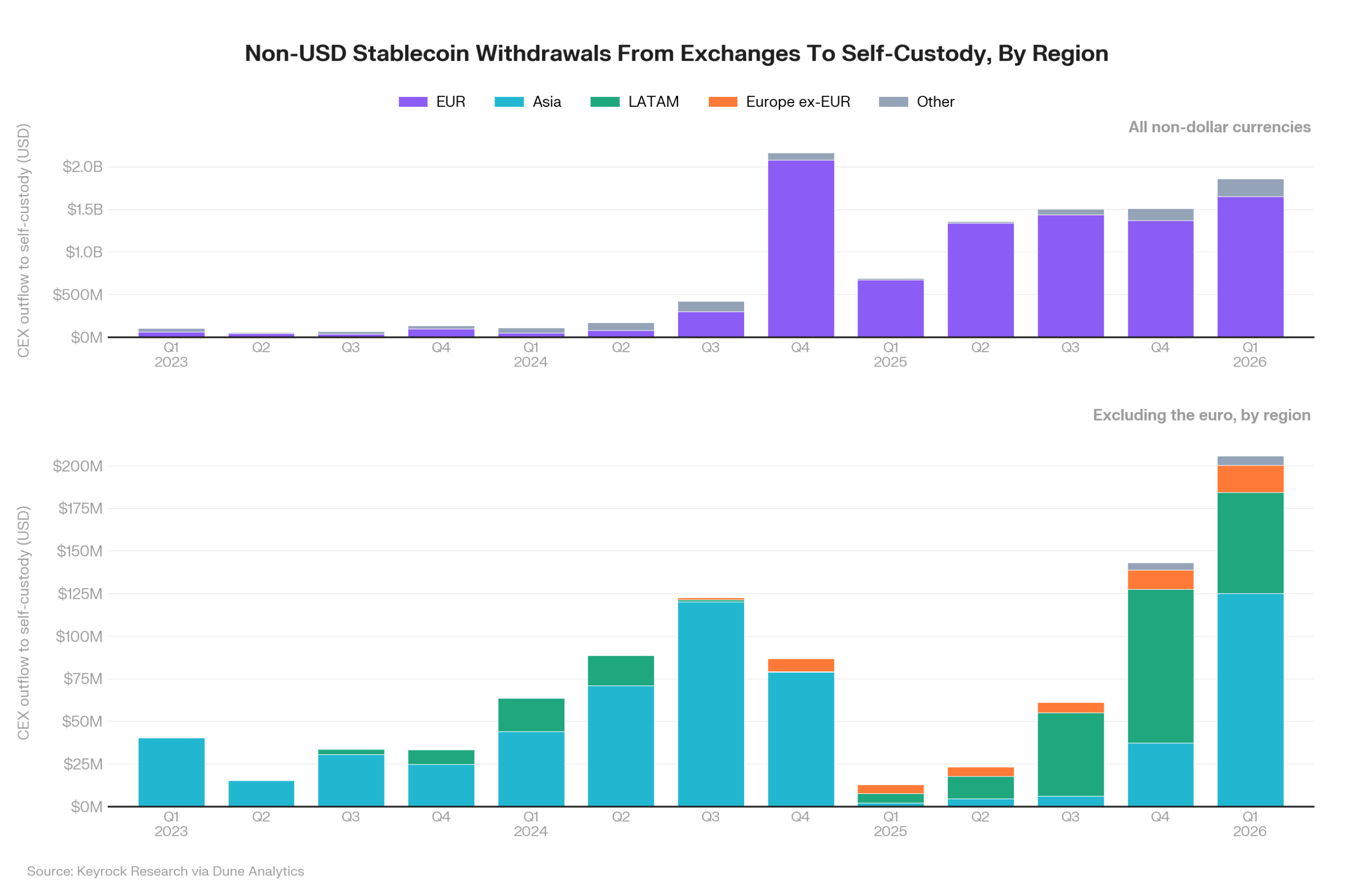

The Bridge

The bridge is where exchange demand becomes onchain money, measured by withdrawals from exchanges into self-custodial wallets. A withdrawal is someone deliberately taking custody, which makes it the cleanest gauge in this report of real onchain demand.

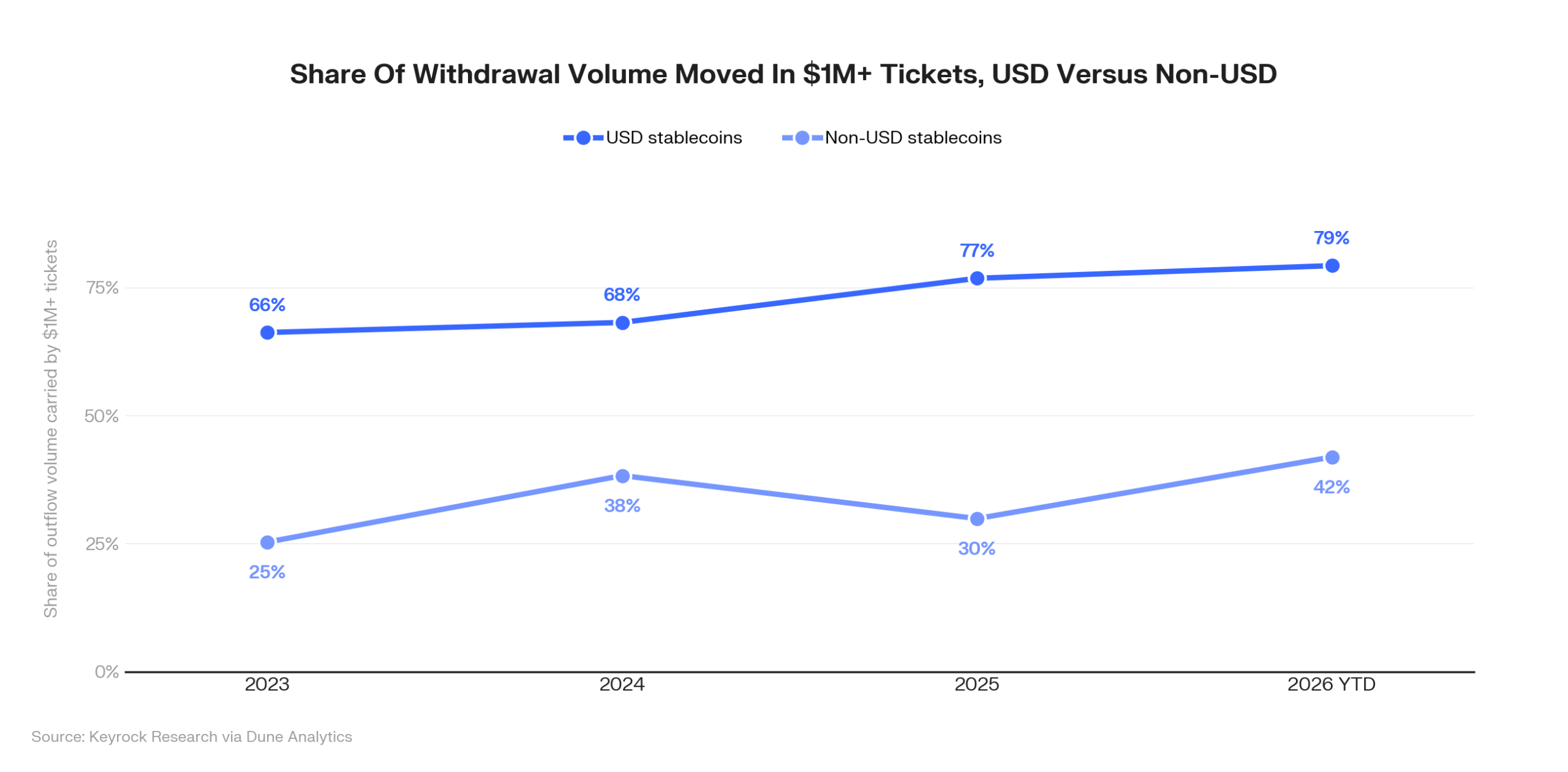

The aggregate is overwhelmingly dollar, $13.7 trillion since 2022, but the non-USD share has risen tenfold over the past 18 months and hit a record $206 million in the first quarter of 2026, with the Singapore dollar, Mexican peso, and Swiss franc each setting their own quarterly records. The flow has also gone wholesale. Tickets of $1 million or more now carry 79% of dollar outflow and 42% of non-USD, up from 66% and 25% in 2023.

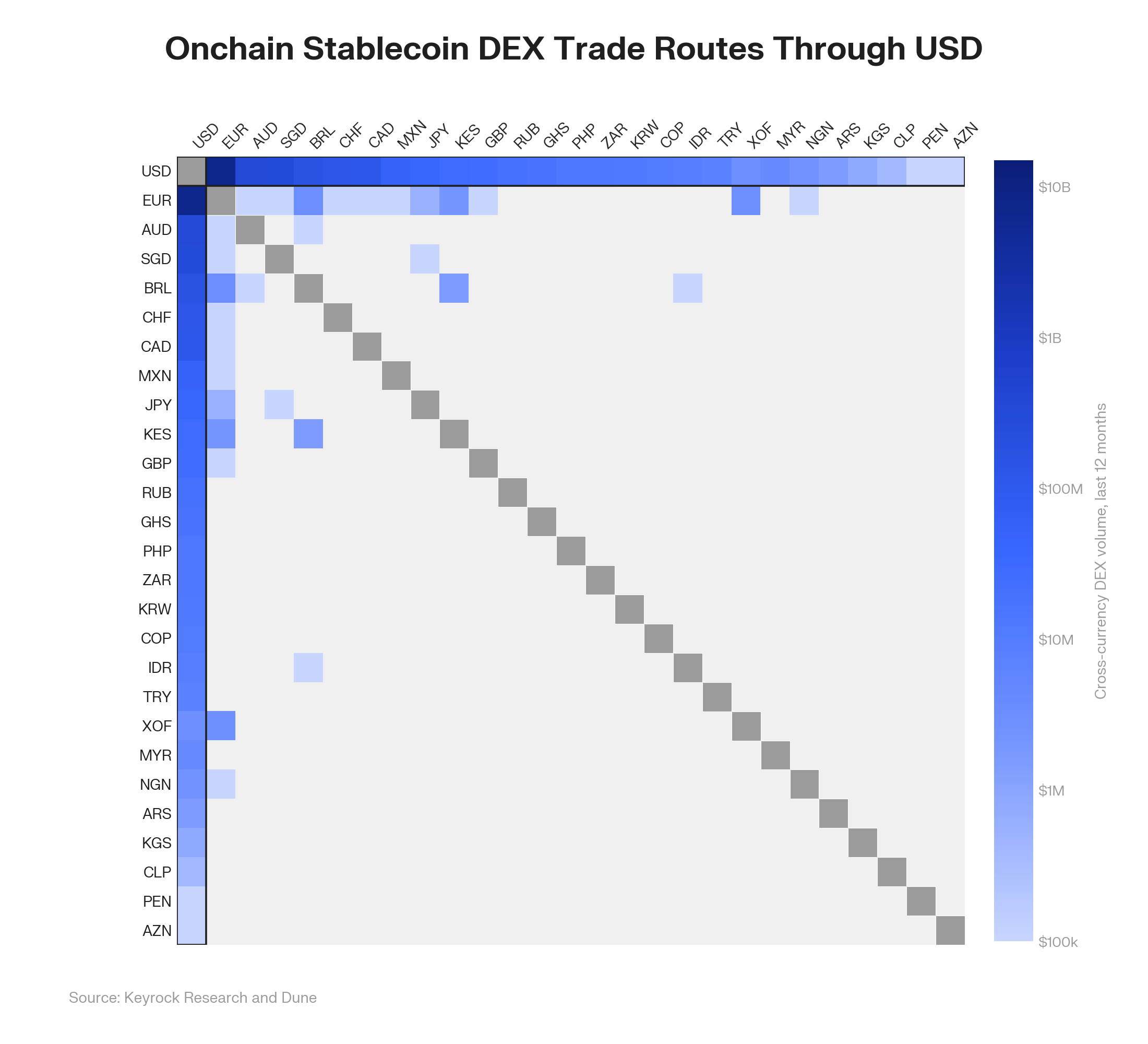

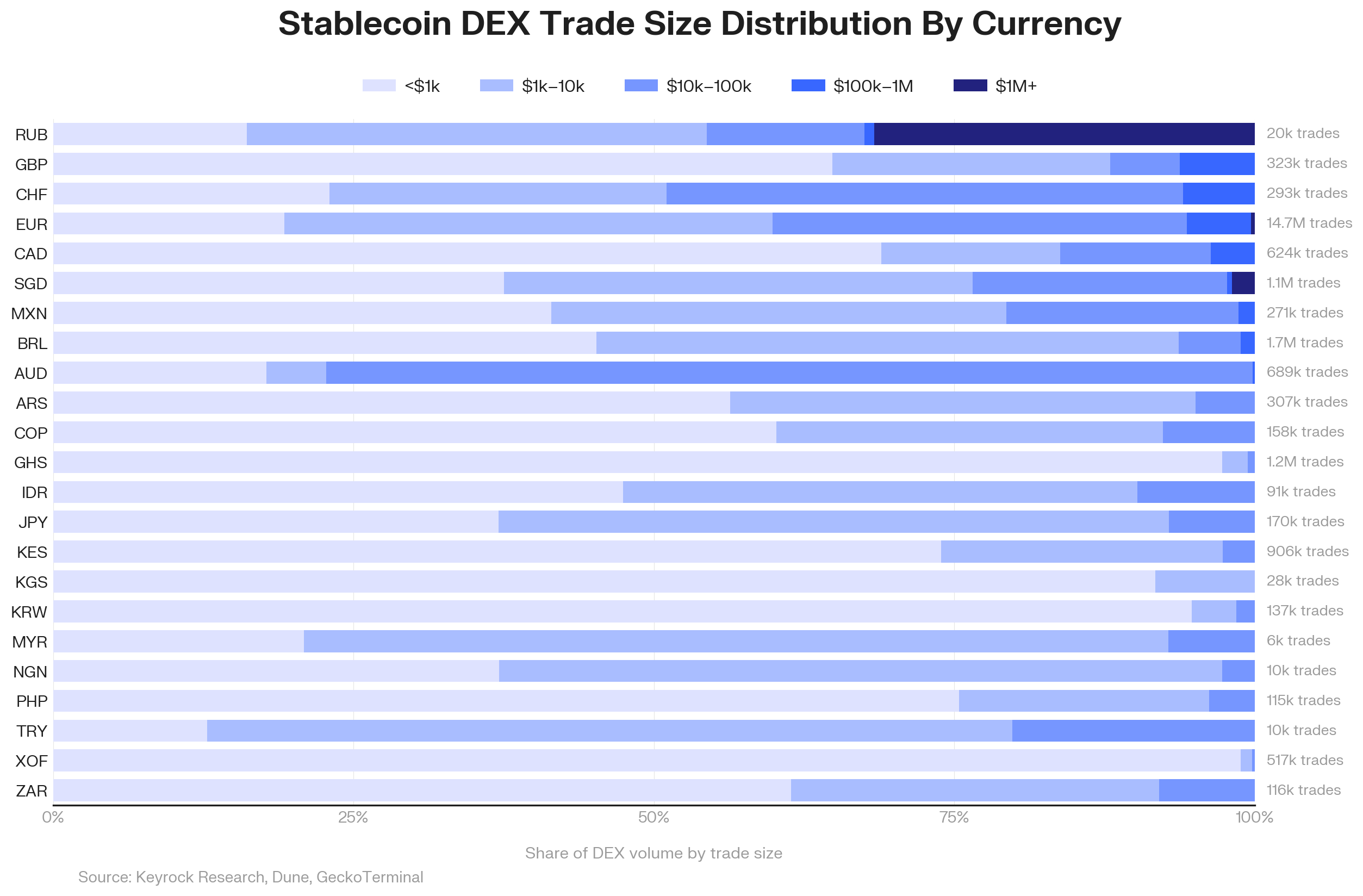

Onchain FX

Onchain DEX trading is the bottom of the funnel, where a local stablecoin’s exchange demand either converts into native trading or does not. Of the 19 currencies trading on centralised exchanges, only 6 carry meaningful onchain DEX volume. Volume reached $1.09 billion in March 2026, near its all-time high, and the euro alone holds 88% of it.

67% of the volume clears on Base, with Aerodrome handling 60% of venue activity and Uniswap another 31%. Onchain FX is materially a Base-and-Aerodrome rail.

Trade sizes sort that onchain activity into distinct profiles. The Russian ruble trades almost entirely in million-dollar tickets, a whale and sanctions-adjacent rail. The euro, Swiss franc, and Australian dollar cluster in the $10,000 to $100,000 band of treasury flow. Most emerging-market currencies sit in $1,000 to $10,000 tickets, and the African currencies run mostly sub-$1,000 swaps.

Conclusion

The ramp is broad and growing, but each stage below it is smaller than the last, and only the euro is active the whole way down. The first quarter of 2026 was the first time the lower stages registered meaningfully, with withdrawals into self-custody at an all-time high. What holds the rest back is liquidity. Only three non-dollar currencies hold $10 million of depth at their deepest venue, and the entire onchain pool base is $46 million, little of it reachable in size.

A currency advances when it has both a regulatory framework issuers can build on and a domestic reason to hold the token rather than convert it into dollars. The euro is the only one that has climbed all four stages, following MiCA’s recognition of the token as a payment instrument, with Brazil and Singapore nearest its position and sterling close behind once its framework lands. Onchain foreign exchange will broaden one currency at a time rather than everywhere at once, and the dollar will remain the currency that trade routes through even as a growing share settles in local denominations.

For media or press inquiries, or questions on data and methodology, contact [email protected]